HEDGEYE RETAIL IDEAS LIST

EVENTS TO WATCH

Tuesday (8/5)

- COH - Earnings Call: 8:30am

- CVS - Earnings Call: 8:30am

- NILE - Earnings Call: 8:30am

Wednesday (8/6)

- RL - Earnings Call: 8:30am

Thursday (8/7)

- TUMI - Earnings Call: 8:30am

- HSNI - Earnings Call: 9:00am

COMPANY NEWS

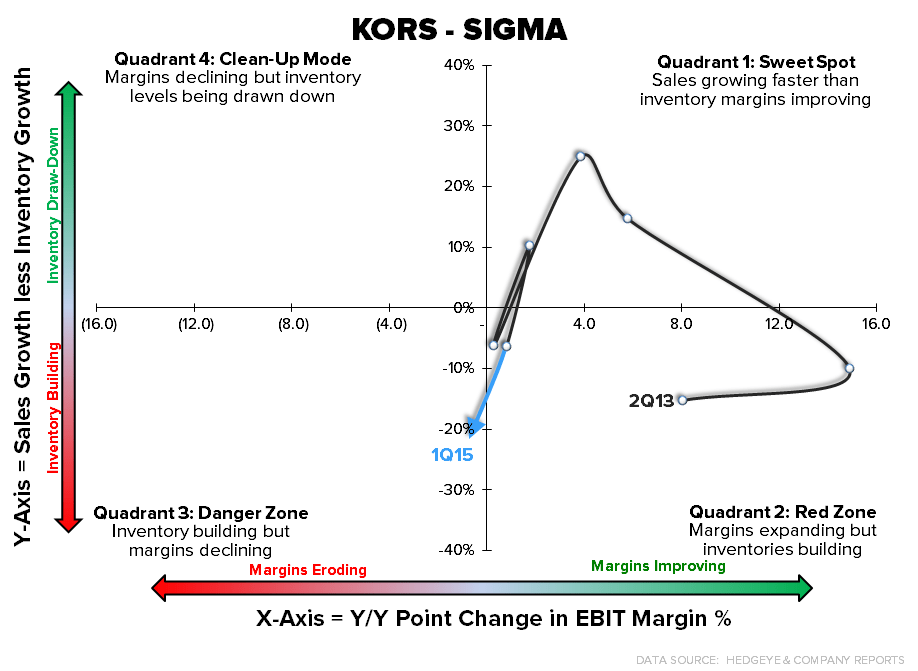

KORS - 1Q15 Earnings

Takeaway: At risk of sounding punitive, this 12% EPS beat was just the 2nd lowest EPS beat in company history. But when you play the 'smoke and guide conservatively' game like KORS does, this stuff matters. The top line still looks solid, and growth outside of the US remains bullet-proof. But the rate of gross margin improvement is decelerating, SG&A spending remains robust (+60%), and the cash conversion cycle looked horrible thanks to a 19 day increase in inventories. This might be a great brand, and a really good company. But something tells us that this print is a watershed event for the stock in that multiple expansion from here could be limited. That's not to say that the stock can't go higher -- but it will need to be driven by revenue and earnings growth. Oh and by the way…if you're a CEO of a company and some of your metrics start to show weakness, do yourself a favor and don't verbally spank your shareholders on the conference call. Not a good idea.

TGT - Target opens three new Canadian stores; plans three more

(http://www.chainstoreage.com/article/target-opens-three-new-canadian-stores-plans-three-more)

- "Target opens three new stores in Canada Aug. 1 and plans three more new Canadian stores later in the fall. The stores are located at Erin Mills Town Centre in Mississauga, Ontario; Park Place in Barrie, Ontario and Carrefour Candiac in Candiac, Quebec."

- "The opening of the three new stores brings the total number Target stores open in Canada to 130."

Takeaway: The reality is that within the next 12 months, Target Canada will look very different than it does today. It will either a) close shop entirely, or b) invest the capital needed to ultimately be a viable and profitable player in the market. This is all on Cornell.

JCP - In the CEO Hunt, Target’s Gain is J.C. Penney’s Loss

- "Target beat out J.C. Penney in landing Brian Cornell as its next chief executive, people familiar with the matter said."

- "The battered department store chain pursued Mr. Cornell about succeeding CEO Mike Ullman. Penney, which has been seeking Mr. Ullman’s successor for a year, contacted Mr. Cornell earlier this year."

- "Despite Penney’s approach, Mr. Cornell 'never expressed any interest' in taking command there, one of the people said Friday."

Takeaway: Truth be told, Cornell could have potentially had a much bigger payday at JCP than at TGT. But on a risk-adjusted basis, it's tough to question his decision.

OTHER NEWS

BOSS - Hugo Boss Shares Decline After Report Permia Seeks Exit

- "Hugo Boss AG shares dropped as much as 3.7 percent after people familiar with the matter said that Permira Advisers LLP is discussing a potential sale of its remaining stake in the German fashion house."

- "Permira, based in London, is in talks with advisers to find a buyer for its 56 percent holding in the German fashion label, valued at about 4.1 billion euros ($5.5 billion)..."

Bangladesh Workers Protest Over Wages

- "A 24-hour deadline to make back payments to 1,500 workers of apparel manufacturer Tuba Group in Dhaka, Bangladesh, created a deadlock on Sunday in talks to end a workers’ hunger strike."

H&M tops list of largest certified organic cotton users

(http://www.fibre2fashion.com/news/garment-company-news/newsdetails.aspx?news_id=166513)

- "H&M is again topping the list of the world’s biggest users of certified organic cotton, according to Textile Exchange’s latest Organic Cotton Market Report 2013. With a 29% increase in the last year, H&M manifests its leading position."

- "This is part of the company’s strategic target to use only more sustainable cotton by 2020."

ARO - P.S. From Aeropostale launches brand in Mexico, 100 stores on tap

(http://www.chainstoreage.com/article/ps-aeropostale-launches-brand-mexico-100-stores-tap)

- "Aeropostale, Inc. will roll out its P.S. from Aeropostale brand in Mexico through a licensing partnership with Distribuidora Liverpool, S.A. de C.V."