Investment Ideas

The table below lists our Investment Ideas as well as our Watch List -- a list of potential ideas that we are in the process of evaluating. We intend to update this table regularly and will provide detail on any material changes.

Recent Notes

07/28/14 Monday Mashup: MCD, YUM and More

07/28/14 MCD: McLibel 2.0?

07/29/14 DRI: Light Gets In

07/31/14 YUM: Warning Shots Fired

Events This Week

Monday, August 4th

- KONA earnings call 4:30pm EST

- JMBA earnings call 5:00pm EST

- TXRH earnings call 5:00pm EST

Tuesday, August 5th

- TAST earnings call 8:30am EST

- BLMN earnings call 9:00am EST

- ARCO earnings call 10:00am EST

- DAVE earnings call 4:30pm EST

- FRGI earnings call 4:30pm EST

- PBPB earnings call 5:00pm EST

- CHUY earnings call 5:00pm EST

Wednesday, August 6th

- PZZA earnings call 10:00am EST

- THI earnings call 2:30pm EST

- GMCR earnings call 5:00pm EST

Thursday, August 7th

- WEN earnings call 9:00am EST

- EAT earnings call 10:00am EST

- JACK earnings call 11:30am EST

- IRG earnings call 5:00pm EST

Friday, August 8th

- MCD July sales and revenue release

Chart of the Day

Recent News Flow

Monday, July 28th

- JMBA announced an expansive franchise recruiting campaign in key markets where they plan to accelerate growth, including Atlanta, Miami, Dallas and specific East Coast markets.

- RRGB is celebrating its 500th new restaurant opening on Monday, August 4th when it opens in Milpitas, CA at the Great Mall of the Bay Area.

- DRI completed its sale of Red Lobster to Golden Gate Capital.

- PZZA announced it is celebrating the summer barbecue with its new Spicy Pulled Pork Pizza.

- DAVE elected David Mastrocola as Chairman of the Board of Directors. Mastrocola currently serves as Co-Founder and Advisory Chairman of Pleasant Lake Partners, LLC and previously served as a partner and Managing Director of Goldman Sachs.

Tuesday, July 29th

- CAKE celebrated National Cheesecake Day by offering any slice for half price.

Wednesday, July 30th

- No significant news.

Thursday, July 31st

- BWLD was upgraded to buy at Sterne Agee with a $176 PT.

- DRI announced a $500m accelerated buyback through Goldman Sachs and Wells Fargo. A portion of the proceeds from the Red Lobster sale will be used to fund this.

- BAGL announced a quarterly dividend of $0.13 per share.

- WEN announced a quarterly cash dividend of $0.05 per share.

Friday, August 1st

- PZZA increased its quarterly dividend to $0.14, up from $0.125.

- CAKE opened a Cheesecake Factory restaurant in Reno, NV.

- BOBE management and the board refuted Sandell's proposals in a recent company presentation, calling the activist's suggestions "shortsighted."

Sector Performance

The XLY (-1.8%) outperformed the SPX (-2.7%). On average, casual dining stocks (-2.9%) underperformed and quick service stocks (-1.7%) outperformed the XLY Index.

XLY Quantitative Setup

From a quantitative perspective, the sector turned bearish on an intermediate-term TREND duration.

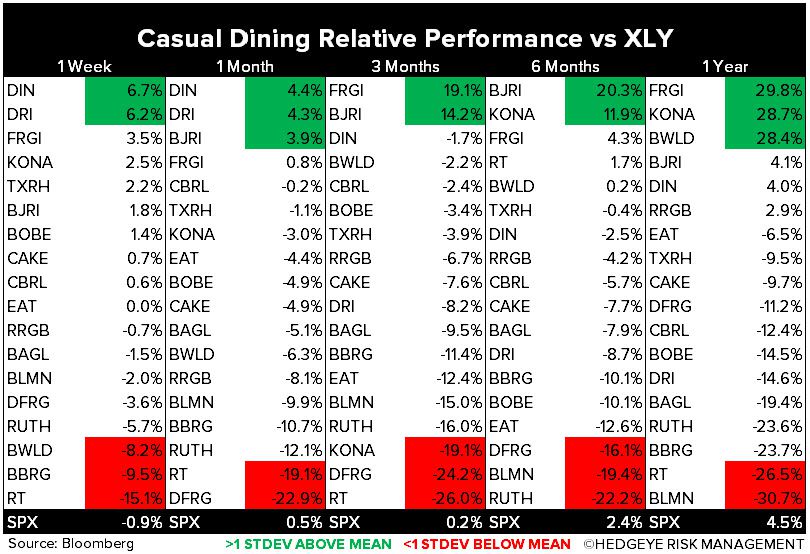

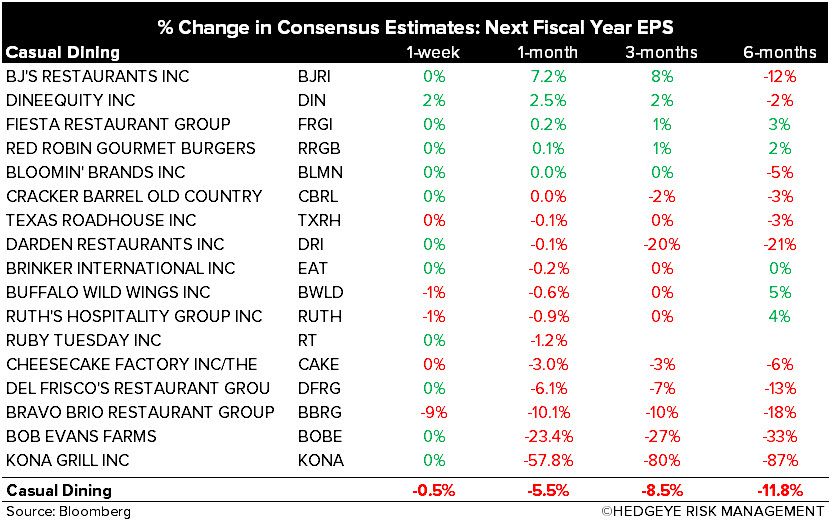

Casual Dining Restaurants

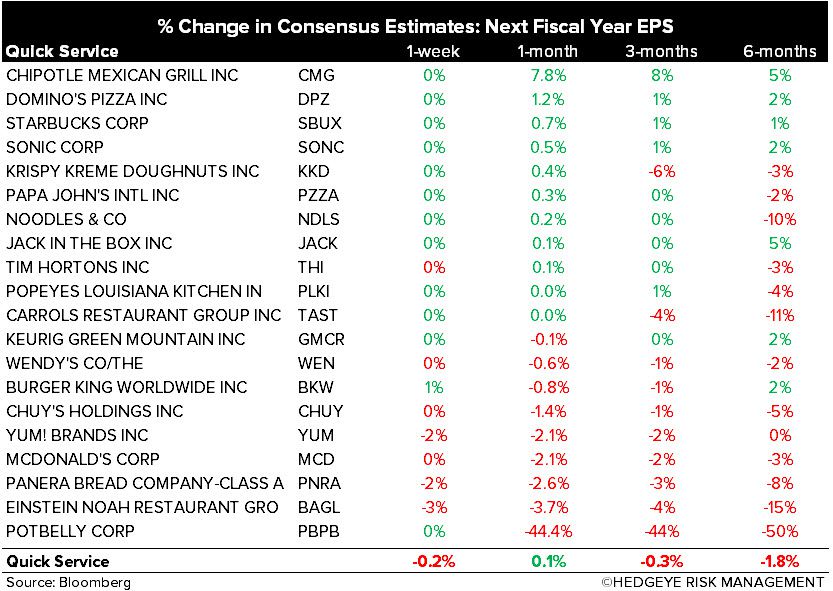

Quick Service Restaurants

Howard Penney

Managing Director

Fred Masotta

Analyst