This note was originally published at 8am on July 18, 2014 for Hedgeye subscribers.

“A remarkable aspect of your mental life is that you are rarely stumped.”

-Dan Kahneman

Lightning struck over 3,000 times in less than 2 hours in the UK last night. Thank God I got out of London in the morning! As I landed in New York, US stock market fear was crashing to the upside (VIX +41% < 2 weeks). Perma stock market bulls on my contra-stream (Twitter) were stumped.

The aforementioned quote comes from one of the forefathers of #behavioral finance (Kahneman wrote Thinking Fast, And Slow) and it’s cited in a book I was reading on the plane by Chip & Dan Heath called Decisive. It’s all about #process and how you make risk managed decisions.

Did you buy Gold Bond before your recent overseas flight? Did you sell the momentum stocks on the June bounce like you should have at the beginning of the year? Everything we do in both business and in life is a decision. It’s a lot easier to read about fighting your emotions and confirmation biases than it is to implement it in your risk management process. But neither life, nor this profession, is easy.

Back to the Global Macro Grind…

Decisive is a relatively new book, but the risk management concepts in it don’t deviate much from how we roll here at Hedgeye. In Chapter 3, the Heath’s introduce the strategy of “multi-tracking.”

“When you consider multiple options simultaneously, you learn the shape of the problem.” (pg 67)

In other words, widen your scope. As I was reading this I realized this is the number one thing that has improved my #process since starting the firm. The more macro I’ve gone, and the more research analysts we hire, the more options I have. There are always bull and bear markets somewhere.

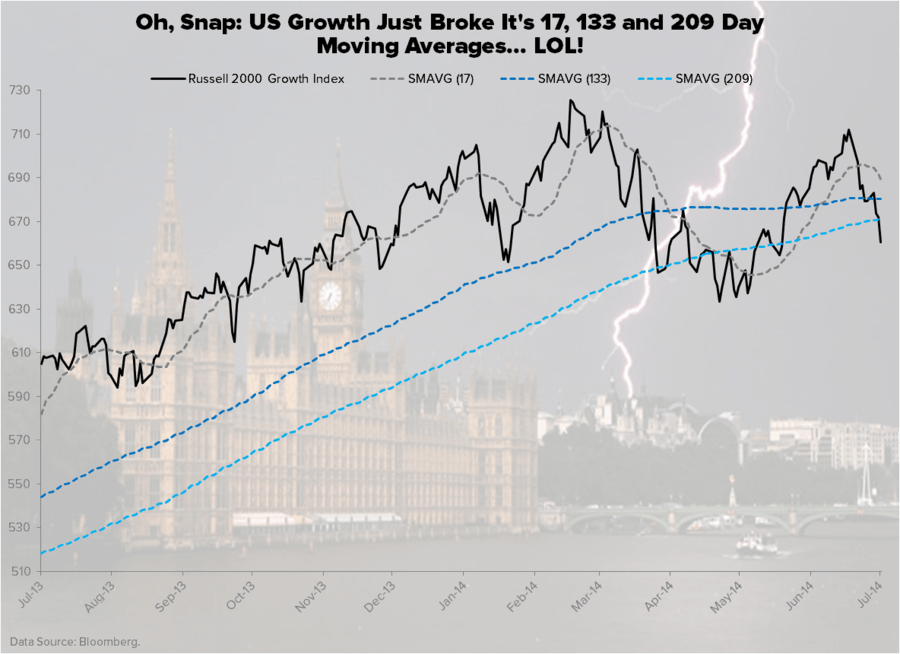

From a risk management perspective, I call our #process multi-factor, multi-duration. This stops me from naval gazing at US equities on a simple moving average, 1-factor (price), chart. It also helps me get bullish when I’m right bearish on US growth – bullish on Gold and Bonds, that is…

In addition to the rip in the VIX yesterday (see our recent Q3 Macro Deck on Volatility’s Asymmetry):

- Gold and Silver ripped +1.5-1.7%, compounding their absolute and relative 2014 gains

- Long-term Treasuries (TLT) had a +1.1% day, hitting fresh YTD highs as bond yields re-tested YTD lows

- Inflation Protection (TIP) had another up-day, moving to +5.1% YTD

Beats being long the Russell growth index.

But the relative (and absolute losses) in the Russell 2000 for 2014 YTD shouldn’t surprise anyone who is reading my rants. While it took 62 trading days to give the SP500 a -1% down day (longest streak since 1995), the Russell has already lost -6.2% since July 7th and is -2% YTD.

Consensus Macro can blame the weather, trains, planes, and automobiles at this point … but the reality is that it’s almost August now and excuse making is not where the performance is.

If the only reason why the US stock market was down yesterday was a Malaysian plane crashing in the Ukraine, why did both Chinese and Indian stocks close UP on the session overnight?

Other than the Down Bond Yields, Down Russell, Up Gold move, what else happened yesterday?

- Housing Stocks (ITB) -2.5% after a horrendous week of housing data (mortgage purchase applications continue to crash)

- Bank Stocks (KRE) -2.3% as the lead indicator for net interest margin (Yield Spread) collapsed to YTD lows

- Biotech Stocks (IBB) -2.2% after the entire edifice of the social-no-earnings thing made lower-bubble-highs vs FEB 2014 peaks

Put another way, what worked and didn’t work yesterday was pretty much the same thing that’s leading and lagging on the 2014 scorecard. If you are bearish on rates, the US consumer, US housing, and high-multiple-bubble stocks with no earnings, you’ve been rarely stumped.

Our immediate-term Global Macro Risk ranges are now:

UST 10yr Yield 2.46-2.55%

SPX 1949-1970

RUT 1123-1155

BSE Sensex 25201-26159

VIX 12.53-14.99

WTI Oil 102.01-104.83

Gold 1299-1345

Best of luck out there today,

KM

Keith R. McCullough

Chief Executive Officer