While RevPAR may have been slightly disappointing to some investors, mix and law of averages suggest potentially better RevPAR for Hyatt and Hilton.

THE CALL TO ACTION

MAR posted a strong quarter all around although expectations were high and recent Smith Travel Research numbers suggested a higher RevPAR estimate and result. HLT and H look good into their prints this week as we believe the read through is actually positive. HLT’s mix should provide better RevPAR than MAR and HOT (who was also lower than STR) while Hyatt should benefit from the outperformance of its portfolio and lower investor expectations. Moreover, the law of averages suggest with two of the four major branded hotel companies already posting lower than STR RevPAR, the probability of better RevPAR from the other two rises.

SET UP

In our July 10, 2014 note “LODGING: STRONG EARNINGS SEASON” we noted “very strong Q2 RevPAR translates into upside revenue and EBITDA revisions for the lodging operators and REITs” and highlighted, “we believe HLT and H have the most upside versus current consensus estimates and even we might be conservative.”

Following MAR earnings release, we feel strongly that HLT and H will beat earnings expectations. MAR gave some explanation as to why their North America RevPAR trailed the Smith Travel numbers and it certainly resonates that it’s not a perfect comparison. However, we still believe that H and HLT should outperform MAR and HOT on North America RevPAR.

SMITH TRAVEL READ THROUGH

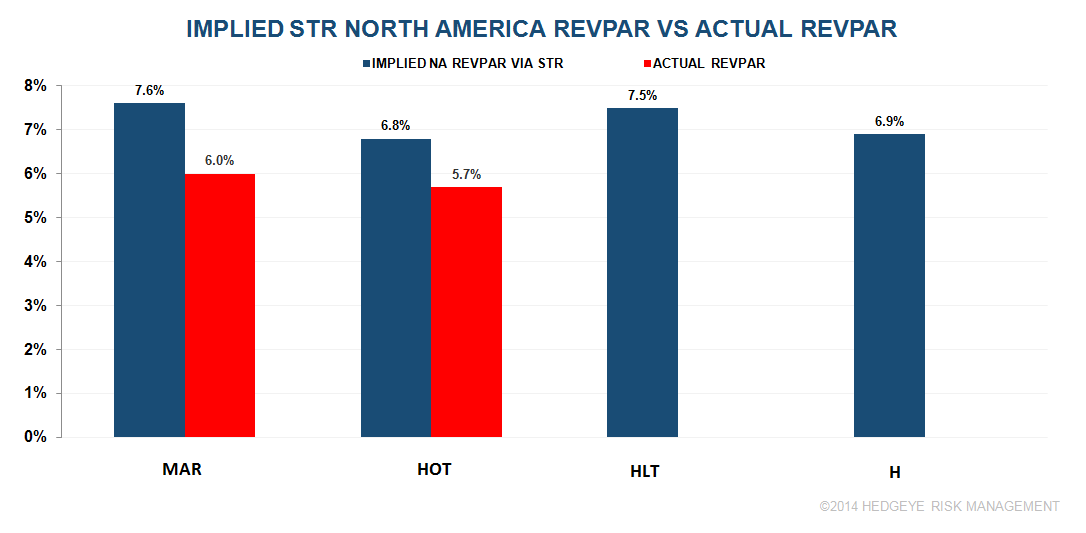

STR RevPAR for Q2 2014 was as follows for North America.

The STR data when paired with the lodging operators' North America rooms data results in implied RevPAR for the lodging operators. There are obviously other variables so the comparison is only a guide. Geography, comp mix, and Canadian exposure will all impact the comparison.

Based on this math, the implied Q2 2014 RevPAR for MAR was 7.6%. By comparison, MAR reported 2Q 2014 actual North American RevPAR of 6.0%. Implied Q2 2014 RevPAR for HOT was 6.8%; however, HOT reported 2Q 2014 actual North American RevPAR of 5.7% (6.3% in constant dollars).

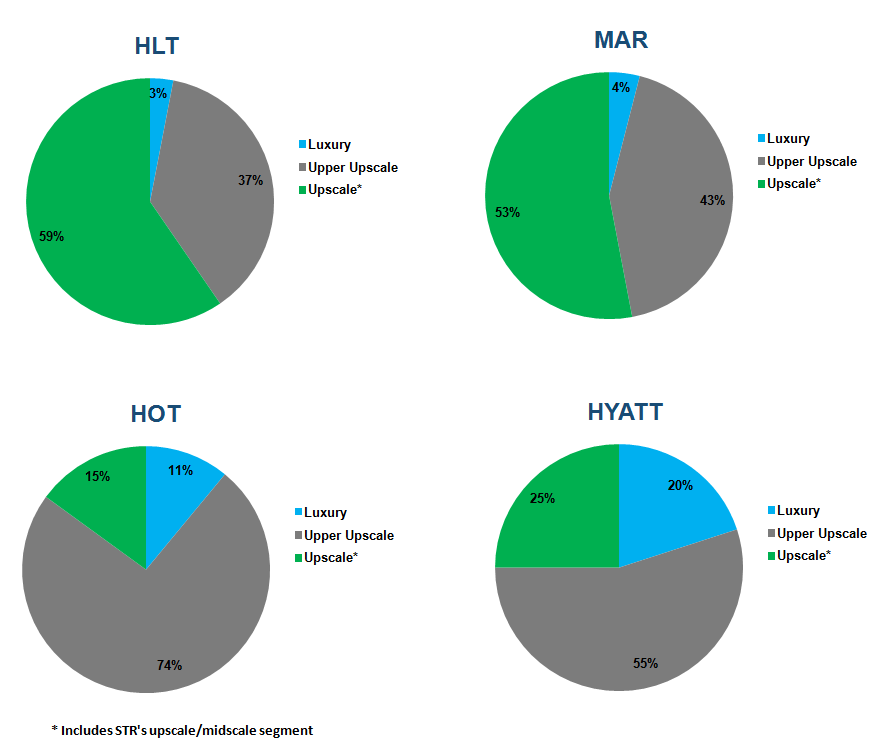

Unlike Marriott and Starwood, Hilton has a significantly greater portfolio exposure to the upscale segment, which experienced the strongest increase in RevPAR during Q2 2014. Based on this analysis, Hilton’s implied RevPAR is 7.5% and Hyatt’s implied RevPAR is 6.9% for Q2 2014.

CONCLUSION

Given the recent commentary from Hilton management regarding lift in group bookings, a stronger outlook for the Big 8 assets, as well as management’s incentive to under promise over deliver, coupled with Blackstone’s shared interest in a beat and raise story, we reaffirm our positive conviction on Hilton into the earnings print – we predict Hilton will go 3 for 3, with a 3rd straight beat and raise in only its third earnings report as a public company.

In addition to Hilton, we also like Hyatt into the earnings print. Similar to Hilton, Hyatt has sizable room exposure to the upscale segment with 25% of total rooms. We have confidence in Hyatt’s ability to continue to drive superior RevPAR performance at Andaz and Park Hyatt (categorized as luxury) as was the case during Q1 2014 when RevPAR at Andaz was +13.6% and Park Hyatt was +9.5%. Finally, we believe Hyatt like Hilton will also benefit from continued strong fee growth due to RevPAR growth and new hotel openings.