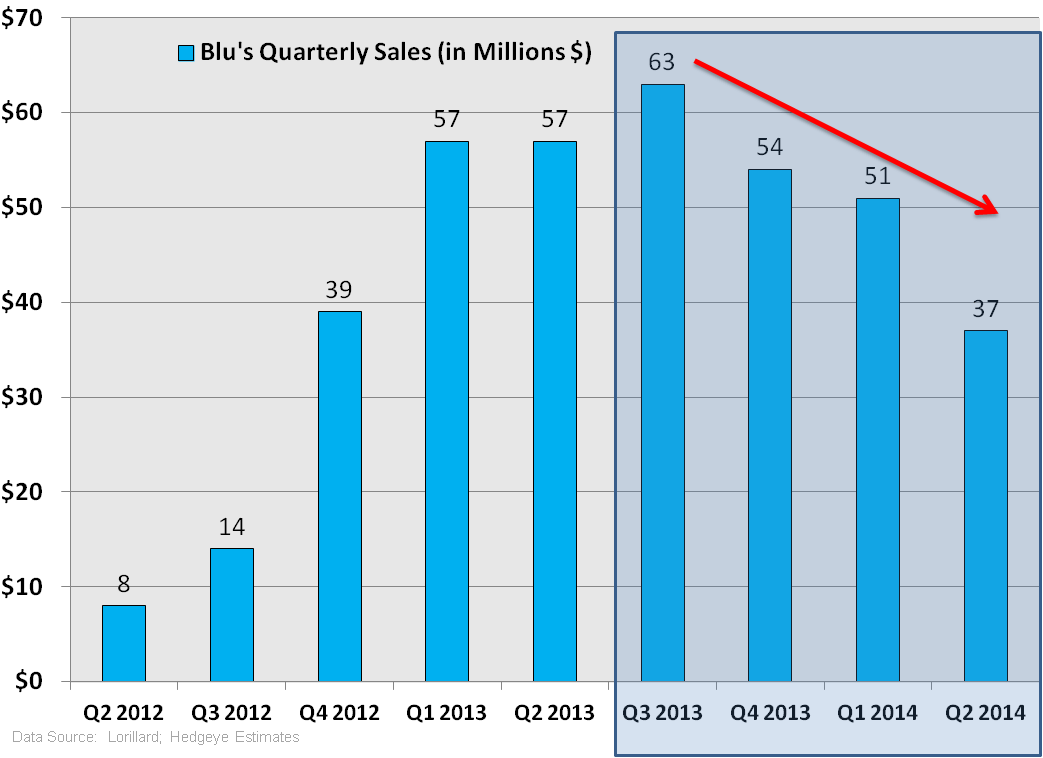

LO’s Q2 results missed on the top and bottom lines (Revenue $1.30B vs consensus $1.34B and adjusted EPS $0.84 vs consensus $0.88). Its e-cig business blu was the material drag on the quarter, with sales of $37M down -35.1% Y/Y and an operating loss of $23M (reported) or $17M (adjusted), showing underperformance accelerating over the last 3 straight quarters.

What We Liked. LO showed why it’s an industry leader in the tobacco industry with continued strong performance from the Newport brand and menthol. In the quarter the company was able to take 6.0% in cigarette pricing (a large number, yet similar to its peers of RAI and MO in the quarter), and outperformed the industry on a volume basis, declining -3.4% (versus an estimated -5.5% for the industry). On the positive side, total LO retail market share in the quarter increased 0.2 share points to 15%; Newport retail share rose 0.3 pp to 12.8%; and Newport’s share of the U.S. menthol market rose 0.2 pp to 37.1%.

What We Didn’t Like. Despite noticeable slowing trends in the traditional (“cig-alike”) e-cigarette category in measured channels over recent months, blu’s underperformance in the quarter is notably weak! Yes the company spent $8M in the quarter to launch blu (UK), rebranding SKYCIG that it bought in October 2013, but given the increased competition from national e-cigarette launches from MO (MarkTen) and RAI (VUSE) in recent months, 2H is looking increasingly challenged for blu domestically, especially given what will be an highly promotional environment to encourage adoption.

In the quarter blu lost 1.1 in share points, maintaining a domestic leading dollar market share in e-cigs of 40.9% (for the 13 weeks ending July 5, 2014 according Nielsen data), but we think that LO/RAI might just be pleased with its plan to sell blu to Imperial (for more on the RAI deal and divestiture to Imperial see Removing Long LO from Best Ideas List).

To say the least, blu has underperformed our expectations for a rebound in 1H 2014 after a weak Q4 2013. As we’ve written about, we attribute the weakness to strength in larger vaporizers (tank/pens/mods/open systems/etc) that are primarily being sold in non-measured channels like vape shops and online. Their appeal is driven on a superior vapor quality, battery life, and lower price versus cig-alike products, the format sold by Big Tobacco, including blu. We expect these consumer trends, along with increased competition within the category given the launches of VUSE and MarkTen to continue to pressure blu’s results.

We removed LO from the Hedgeye Best Ideas list on the long side on 7/15/14 following the announcement of RAI to acquire the company.

Of note is that LO opted not to hold a conference call on the quarter, likely related to the announcement of RAI’s intention to acquire the company.

Howard Penney

Managing Director

Matt Hedrick

Associate

Fred Masotta

Analyst