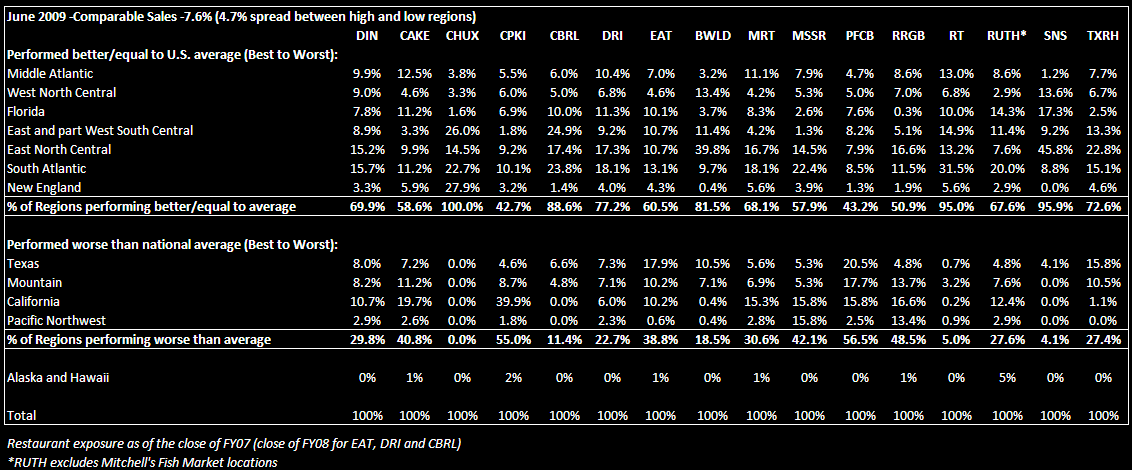

Malcolm Knapp provides regional performance data on a monthly lag basis relative to the overall sales and traffic results. This morning we got the July numbers for sales and traffic, which were just bad (-8.4% and -7.7% respectively). On a regional basis, in June, Texas shifted into the group of regions that performed worse than the national average, which was -7.6%. New England, on the other hand, performed better or equal to the national average. I only point this out because Texas has performed better than the average while New England has underperformed for most of 2008 and year-to-date as tracked by Malcolm Knapp. Both TAST and TXRH highlighted on their 2Q earnings calls this softening of trends in Texas in June.

Other regional shifts include both Florida and the South Atlantic which have been outperforming the national average in recent months after consistently underperforming in 2008 and early 2009. Granted, all of the regions posted negative numbers and the spread between the best and worst performing regions of 4.7% has actually narrowed from 7.1% in May and 5.4% in April.

The chart below shows casual dining restaurants’ exposure to the better and worse performing regions of the U.S. relative to the national average from a comparable sales growth perspective in June. CHUX, RT and SNS have over 90% restaurant base exposure to the regions that performed better than or equal to the average in June.