TODAY’S S&P 500 SET-UP – July 28, 2014

As we look at today's setup for the S&P 500, the range is 21 points or 0.62% downside to 1966 and 0.44% upside to 1987.

SECTOR PERFORMANCE

EQUITY SENTIMENT:

CREDIT/ECONOMIC MARKET LOOK:

- YIELD CURVE: 1.99 from 1.98

- VIX closed at 12.69 1 day percent change of 7.18%

MACRO DATA POINTS (Bloomberg Estimates):

- 9:45am: Markit U.S. Services, July prelim., est. 59.8 (prior 61.0)

- 9:45am: Markit U.S. Composite PMI, July prelim. (prior 61)

- 10am: Pending Home Sales m/m, Jun, est. 0.5% (prior 6.1%)

- 10:30am: Dallas Fed Mfg Activity, July, est. 12 (prior 11.4)

- 11am: Fed purchases $1b-$1.25b notes in 2036-2044 sector

- 11am: U.S. announce plans for auction of 4W bills

- 11:30am: U.S. to sell $27b 3M, $24b 6M bills

- 1pm: U.S. to sell $29b 2Y notes

GOVERNMENT:

- EPA to hold public hearings this week in Atlanta, Denver, Pittsburgh, Washington on proposed carbon dioxide emissions standards for existing, modified, reconstructed power plants

- EU representatives to discuss curbs on trade, investment with Crimea, penalites for business allies of Russian President Vladimir Putin

- 9:30am: Rep. Scott Garrett, R-N.J., holds roundtable on equity market structure with KCG CEO Daniel B. Coleman, SIFMA CEO Ken Bentsen, Nasdaq OMX CEO Robert Greifeld, BATS Global Markets CEO Joe Ratterman, TD Ameritrade CEO Fred Tomczyk among participants; Library of Congress

- 12:15pm: Treasury Secretary Jack Lew releases annual Social Security and Medicare trustees reports

WHAT TO WATCH:

- Danone said to be in talks to sell medical unit to Hospira

- JPMorgan to sell $1.3b of assets to Sankaty Advisors

- Yukos owners win $50b award against Russia

- Global pressure mounts on Israel to halt Gaza offensive

- Goldman said in talks to settle mortgage case for $800m-$1.25b

- Reckitt Benckiser confirms plans to spin off suboxone unit

- China H-shares rise 20% from March low, enter bull market

- Big Mac banished in Shanghai after meat scare prompts recall

- U.S. says satellite photos show Russia shelling into Ukraine

- Fox said open to giving board seats to Time Warner investors

- Microsoft taps Tencent, JD.com for first Xbox sales in China

- Deutsche Bank, HSBC sued for alleged silver fix manipulation

AM EARNS:

- Armstrong World (AWI) 7am, $0.65

- Capitol Federal Financial (CFFN) 8am, $0.14

- Compass Minerals Intl (CMP) 7am, $0.26

- Cummins (CMI) 7:30am, $2.39

- Old National Bancorp (ONB) 9am, $0.26

- Roper (ROP) 7am, $1.50

- RPM Intl (RPM) 7:30am, $0.78

- Tenneco (TEN) 7am, $1.26

- Tyson Foods (TSN) 7:30am, $0.78

PM EARNS:

- American Capital Agency (AGNC) 4:01pm, $0.68

- American Financial (AFG) 5pm, $0.94

- Amkor Technology (AMKR) 4:08pm, $0.15

- CNO Financial (CNO) 4:03pm, $0.31

- Cognex (CGNX) 4:06pm, $0.22

- Crane (CR) 4:15pm, $1.16

- Eastman Chemical (EMN) 5pm, $1.84

- General Growth Properties (GGP) 4:01pm, $0.10

- HealthSouth (HLS) 4:30pm, $0.47

- Herbalife (HLF) 4:30pm, $1.57

- Integrated Device Technology (IDTI) 4:01pm, $0.16

- Jacobs Engineering (JEC) 9:30pm, $0.86

- Masco (MAS) 5:15pm, $0.28

- Norwegian Cruise Line (NCLH) 4pm, $0.57

- Owens & Minor (OMI) 5:17pm, $0.46

- PartnerRe (PRE) 4:30pm, $2.62

- Plum Creek Timber (PCL) 4:04pm, $0.30

- Range Resources (RRC) 5:02pm, $0.40

- WR Berkley (WRB) 4:05pm, $0.76

- XL (XL) 5pm, $0.84

COMMODITY/GROWTH EXPECTATION (HEADLINES FROM BLOOMBERG)

- WTI Crude Drops Before U.S. Economic Data; Brent Falls

- Gold Bulls Boost Bet on Rally as Prices Extend Drop: Commodities

- World Weather Seen Abnormal as El Nino Poised to Develop: Lerner

- Gold Declines in London as Stronger Dollar Curbs Investor Demand

- Lead Reaches 17-Month High on Supply Outlook as Aluminum Gains

- Wheat Production in Parts of Australia Seen Hurt by Dry Weather

- Big Mac Banished in Shanghai as Meat Scare Prompts Probe

- Morgan Stanley Sees Weaker Aluminum Premiums as Contango Shrinks

- China Takes on Hitachi as 17-Year-Old Rare Earth Patent Ends

- Rubber Reaches Three-Week High as Thai Price Drop Lures Buyers

- Steel Rebar Rises Most in One-Month as China Outlook Improves

- Bulls Fleeing Natural Gas as Goldman Sees Further Drop: Energy

- Corn, Wheat Supply Outlook Fully Priced In, ANZ Says in Report

- China’s State Stockpiler Said to Miss Cobalt Purchase Target

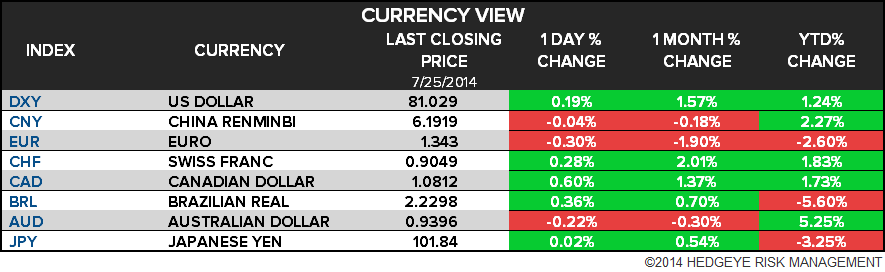

CURRENCIES

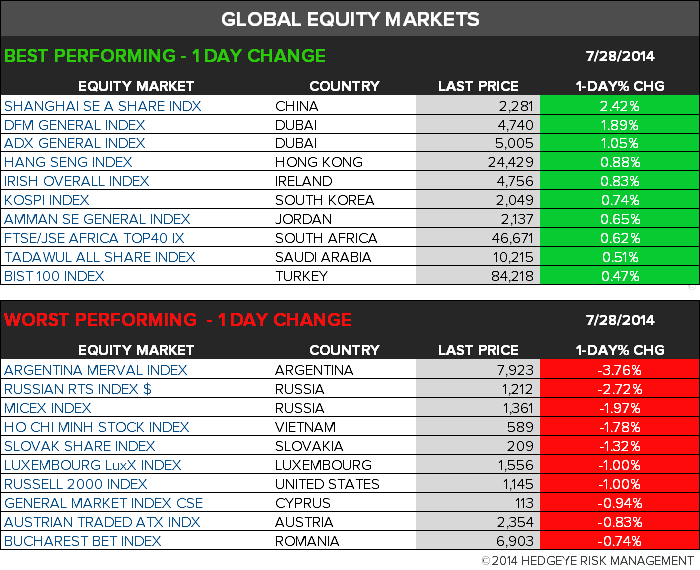

GLOBAL PERFORMANCE

EUROPEAN MARKETS

ASIAN MARKETS

MIDDLE EAST

The Hedgeye Macro Team