HEDGEYE TV

Outspoken free market economist and TV personality Larry Kudlow explains why America is suffering from the "worst recovery since World War II" and offers solutions on how the U.S. can regain its economic footing once again.

Here’s the question-and-answer portion from Keith’s daily Morning Call with Hedgeye’s institutional subscribers.

CARTOON

INFLATION SHARK

Real Americans are about to get eaten.

CHART

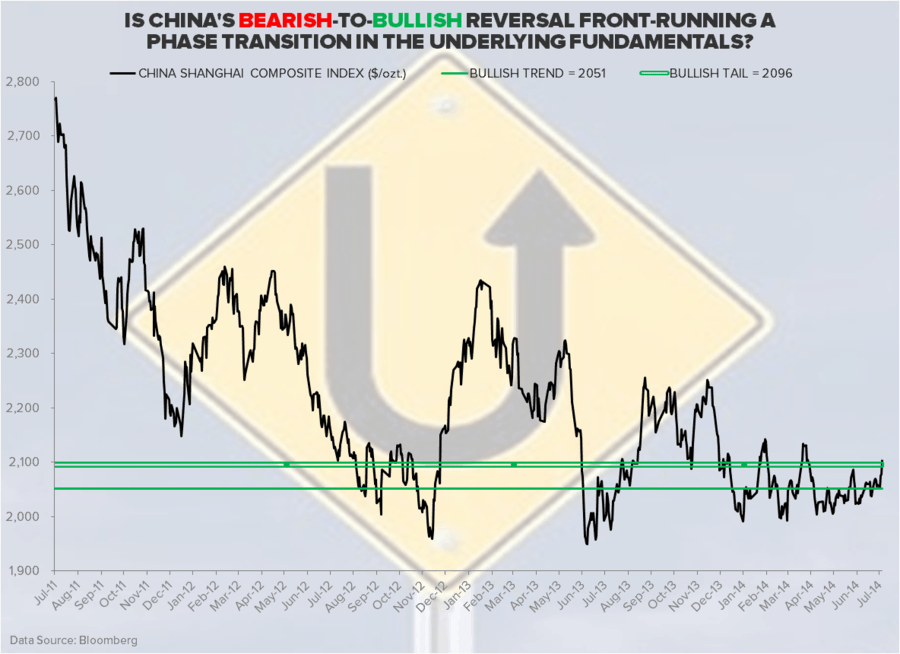

HARBINGER? CHINA'S BEARISH-TO-BULLISH REVERSAL

Chinese Stocks (Shanghai Composite) closed up another +1.3% last night after China’s best PMI in 18 months.

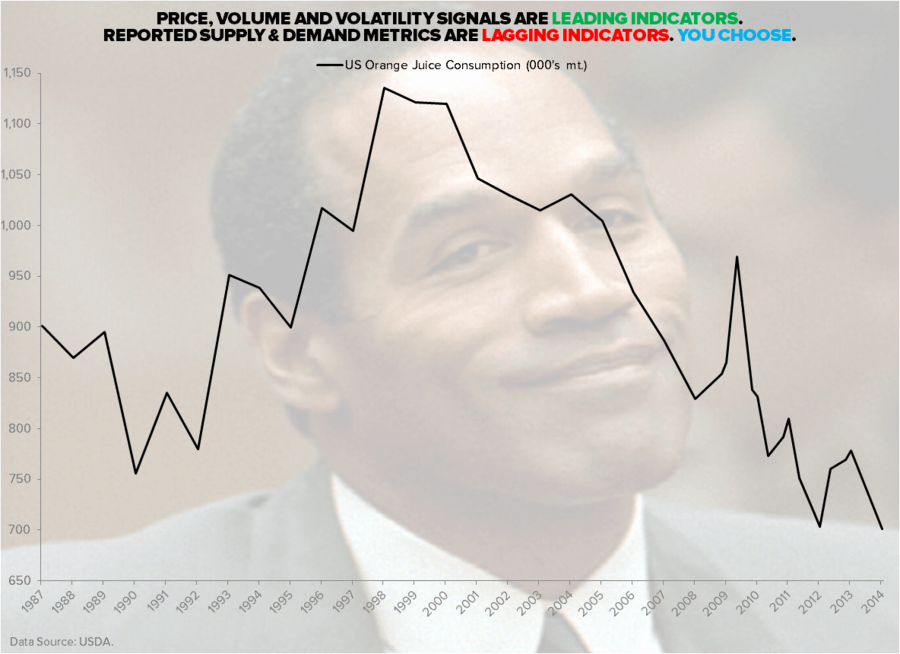

LEADING VS. LAGGING INDICATORS: YOU CHOOSE

Risk managing macro rarely has anything to do with “valuation” or even reported supply and demand metrics. Most of the big moves in macro happen on the margin when there is a phase transition in price momentum, volume, and volatility.

POLL

Measures of volatility suggest investors remain complacent about a variety of risks, including rising global turmoil which could disrupt the calm over the coming months.

The our poll on Wednesday we asked: Which global conflict is a bigger market threat Israel/Gaza or Russia/Ukraine?

At the time of this post, 69% voted that Russia/Ukraine posted the bigger market threat vs 31% that voted for Israel/Gaza.