Below are Hedgeye analysts' latest updates on our NINE current high-conviction investing ideas and CEO Keith McCullough's updated levels for each.

We also feature three recent institutional research notes which offer valuable insight into the markets and economy.

Trade :: Trend :: Tail Process - These are three durations over which we analyze investment ideas and themes. Hedgeye has created a process as a way of characterizing our investment ideas and their risk profiles, to fit the investing strategies and preferences of our subscribers.

- "Trade" is a duration of 3 weeks or less

- "Trend" is a duration of 3 months or more

- "Tail" is a duration of 3 years or less

HEDGEYE CARTOON OF THE WEEK

IDEAS UPDATES

BOBE – We continue to like Bob Evans as a long and part of this thesis revolves around a potential value creating transition to an asset light business.

Bob Evans’ significant real estate holdings give management the ability to convert to an asset light model in order to significantly enhance shareholder value. In the restaurant industry, there have been a number of public companies that have pioneered such a transition. We point to Jack in the Box (JACK) as the most recent success story, but numerous others have successfully sold restaurant assets as well.

Two direct competitors in the family dining segment, Denny’s (DENN) and IHOP (DIN), are nearly 100% franchised. Burger King (BKW) has also made an aggressive push to an asset light model in order to generate substantial value for shareholders.

In the restaurant space, franchisees have been known to run restaurants better than the franchisors running the brand. We don’t see why this would be different in the case of BOBE and believe there would be a significant appetite to sell off large blocks of stores.

In an asset light model, we believe BOBE would be able to collect as much as 10-12% of revenues in rent and royalty on a per-store basis. This compares favorably to the current 7% operating margin. In addition, we estimate the company could generate $300-600 million pre-tax in asset sales. The cash generated would allow the company to reduce its current outstanding share count by 20-30%.

Changes of this magnitude will undoubtedly take time, but the numbers suggest the stock would see meaningful upside.

GLD – With a slight bounce in the dollar week-over-week, the 10-year yield and and gold remained relatively flat in advance of the first Q2 GDP print and FOMC statement on Wednesday next week. The bond market needs more evidence of any sustainable dollar strength with the likely catalyst coming with September’s Jackson Hole meeting, We expect a sequential increase off of a very weak -2.9% Q1 print (Note: The Fed expects +2.1-2.3% for the full year, so we would need to see a significant acceleration).

Albeit relatively small this week, the sector variances that ensue when our economy is slowing with cost of living accelerating continue to grind wider:

Week-over-Week % Change:

- XLE: +0.9% Energy Sector that lives on production cost/energy price inflation margin

- TLT: +0.8% We remain long one of our key, non-consensus macro calls moving into this year (10-year yield down from 3.028% on December 31st to 2.47% ... -18.5%)

- December 31st was both the highest point for the 10-year and largest consensus short 10-year position (-175K contracts since). Not only was consensus short in front of a -18.5% move down; It was the largest short position since

- CRB Food: +0.9% Headline inflation crushes everyone; while, unfortunately not all Americans can hedge their cost of living squeeze with Gold or a Treasury bond

- S&P 500: Flat

- Russell 2000: -0.6% Small companies need a strong consumer to justify the growth assumptions baked into valuations

- Consumer Discretionary: -1.10% Stagnating real wage growth with cost of living increases means less real disposable income chasing consumer products

Despite the headline inflation this year, real wage growth declined -0.1% in June on a year-over year basis. If you are one of the minority with the ability to hedge your real earnings power, we continue to recommend an allocation to gold, treasuries, and sectors that do not depend on the disposable income of the consumer.

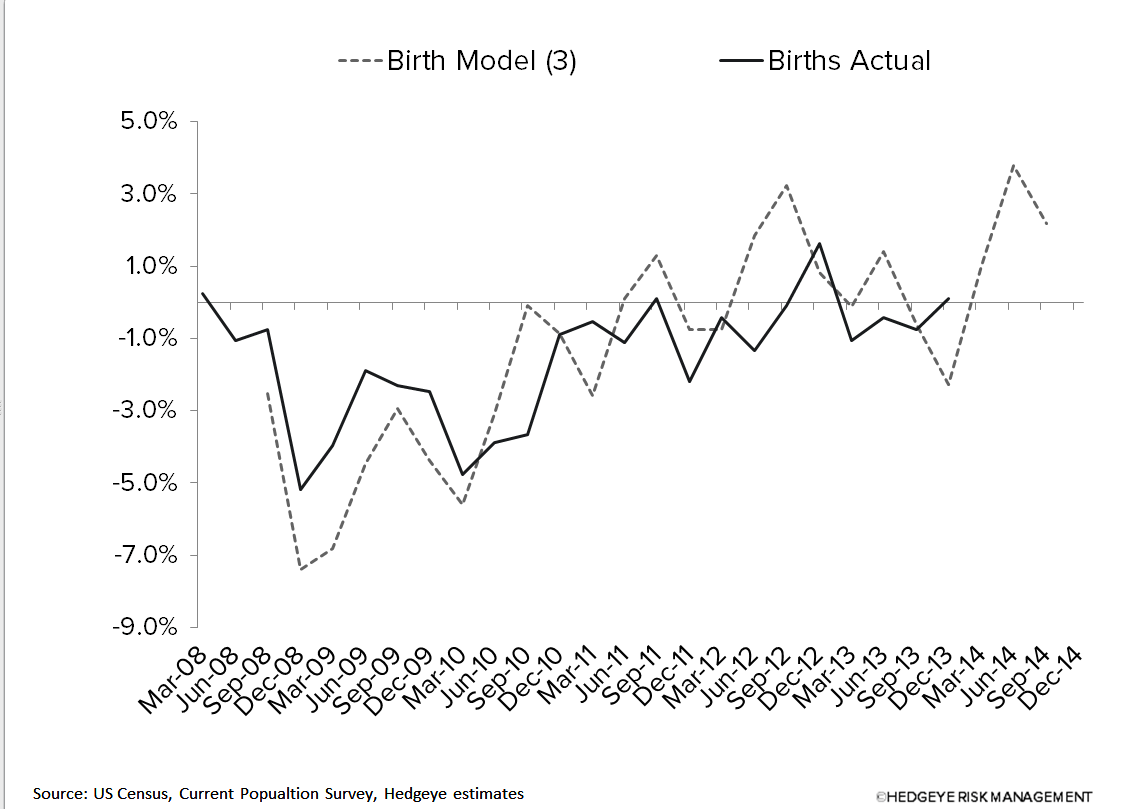

HCA – The question of what to do with HCA at this price is beginning to become harder to answer. Within our framework, there appears to be adequate upside from here as consensus moves their numbers higher for 2015 and HCA and its peers report solid quarterly results. Zimmer Holdings (ZMH) reported sequentially weaker results in their hip and knee businesses, which is becoming a concern as the aggregate category sales appear to be slowing. If this trend continues, we’ll get more cautious on HCA and hospitals.

On the other hand, we updated our maternity model today with the most recent data from June 2014. The forecast continues to show considerable acceleration into the second half of 2014. With unemployment claims continuing to trend below 300,000 per week, employment trends should continue to be supportive of HCA as well. When it starts to feel like we are playing for just a small amount of upside, we’ll rethink our long position. As of now, there are some cracks, but nothing (yet) that has changed our view.

HOLX – Hologic reports this Tuesday. We think they will report modest upside to their numbers, but we expect some concern about the strength of the Breast Health growth rate. Fiscal 3Q last year is a very difficult comparison based on their disclosures regarding contributions to Breast Health revenue growth. On a year over year basis, the growth rate may look challenged particularly as we have seen placements of 3D systems run slightly lower than the previous quarter. HOLX reacted positively to the upside last quarter in Breast Health revenue.

Given that there remains plenty of bears on the name that we continue to speak with, a disappointing Breast Health revenue print may drive the stock lower on Tuesday. While we still like the name, there is some risk heading into the quarter that we want you to be aware of, and depending on your horizon, trade around.

LM – Legg Mason announced the acquisition of Martin Currie (MC), an Edinburgh-based equity asset manager at the end of the week filling a large hole in their product offering. Martin Currie is a 100% institutional manager that delivers both traditional and alternative equity management and importantly has been in inflow over the past 2 years.

Legg will look to assist MC with their distribution as LM has substantially deeper penetration into U.S. brokerage networks as well as other international relationships.

We calculate the deal will be accretive by at least 2% within the first 12 months and up to 3-4% over a longer period of time. We like the fact that Legg is using its excess capital to enhance its business and not just engineer higher earnings per share solely by reducing its share count.

We think fair value on Legg stock resides closer to $60 per share.

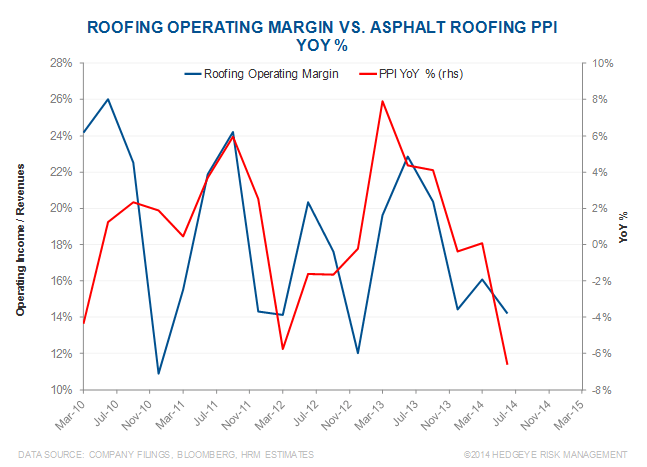

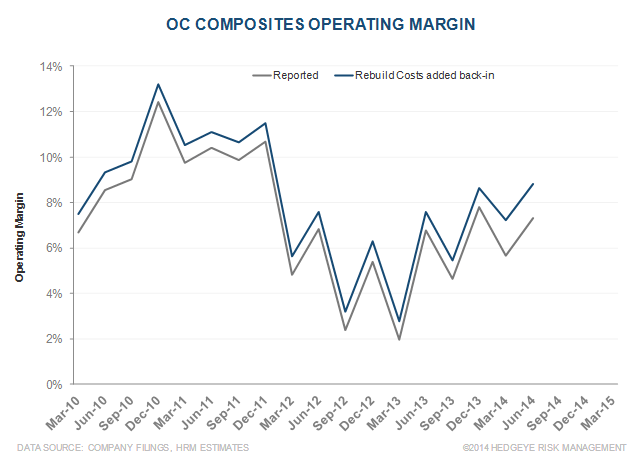

OC – At first, the Owens Corning earnings release did not read well. However, there are encouraging signs masked by weaker Roofing results. Margins in Insulation and Composites (ex-rebuilds) expanded at a healthy rate. Corporate expenses were lower. Much of the report was reasonably positive.

As indicated in OC’s pre-announcement, the Roof segment was weaker than expected. This is a topic of great interest, since it is challenging to pinpoint what is driving the margin pressure. Our understanding is that the change is not structural. Rather, we believe an input price drop early in the year stimulated production during a period of weather-curtailed demand. The resultant excess inventory pressured pricing in a second quarter demand environment that was well below longer-term ‘normalized’ levels. We expect an eventual return to replacement levels of roof shingle demand to resolve these shorter-term challenges. However, this is an understanding we continue to challenge, and we are scheduling another call on roof shingle competition, this time with a focus on distribution.

We are sticking with OC because the Insulation and Composites businesses are tracking well and have significant value creation potential. While we expected margin pressure in Roofing, recent margin pressure has exceeded our expectations. The Roofing pressure does not appear to be structural, but we will continue to try to verify that it is not. However, we expect Insulation and Composites segment margins to expand, with this quarter’s results again lending credibility to that view. Revenues in the Insulation and Composites segments are roughly as large as that of Roofing. We expect the Insulation margin to nearly match that of the Roofing business and Composites margin to reach double digit levels by 2016. In that scenario, OC would generate $5 to $6 per share in EPS, including tax expense, assuming our construction rebound scenario plays out roughly as expected (leaving aside the rough $5/share NOL). That well exceeds current consensus estimates. Our reasonable range of assumptions yield valuation range extending from the mid-40s to the high 60s.

OZM – Market rumors swirled at the beginning of the week that the Department of Justice (DOJ) was softening its stance against Och Ziff on its potential violation of the Foreign Corrupt Practices Act (FCPA). We have always estimated that this issue was well discounted in the stock with an $800 million decline in OZM’s market cap having come about on this FCPA issue based on a $200 million loan, which is part of the reason the stock is on our Best Ideas list as a long.

Despite, the strong move up this week, longer term there is still upside in the stock.

OZM is now trading at 3.5x its incentive fees, right at the midpoint of its 0-7x historical incentive fee multiple. If we assume that the pension tailwind can force this incentive multiple back to new highs, there would be another 15% upside to over $16 per share (stock is at $14) plus investors would clip a 10% dividend yield, so a few ways to get paid here.

RH – Here’s an interesting Macro nugget about Restoration Hardware. It makes sense that it puts its stores in the wealthier areas of the US. If we map out a 60 minute driving radius around each of its existing stores, we see that the average household income is $81,000, versus $65,000 for the average US city. That 25% bump is nice.

But what’s even more interesting is that when we look at how much money households spend each year on home furnishings, it’s $857 on average throughout the US. But in RH territories, the average household spends $1,779/yr – more than double the US average.

We’ve done extensive analysis showing how increasing the size of the existing store fleet will result in meaningful market share growth for RH, at an increasingly higher ROI.

RH remains our top retail idea, even after its recent run.

TIP – Keeping up with the U.S. inflationary data released last week, things are continuing to pick up on the domestic inflation front as another high frequency data point was released.

CPI advanced another +0.3% MoM while holding flat YoY at 2.1%. Moving through the second half of 2014, we should see this accelerate as annual comparisons continue to get easier. This data adds to our conviction in staying long of the iShares Tips Bond ETF (TIP) as a way of profiting from accelerating rates of reported inflation over the intermediate term.

Next week, the ISM Input Prices and GDP Deflator numbers are scheduled to be reported. It is likely these relevant data points add to the U.S. cyclical inflation story should continue to support our long idea in TIPS.

* * * * * * *

Click on each title below to unlock the content.

Well that was short-lived. Last month's NHS report suggested a return to positive momentum. Nothing could have been further from the truth.

McDonald's: In Need of a Major Restructuring

Until proven wrong, we continue to believe some of MCD's wounds are self-inflicted and stem from the company's attempt to be all things to all people while over-indexing the business toward beverages.

Fund Flows: Stocks Over the Waterfall, Bonds Bolstered

U.S. stock funds put up their 12th consecutive week of outflow with bond fund inflows holding steady.