TODAY’S S&P 500 SET-UP – July 25, 2014

As we look at today's setup for the S&P 500, the range is 31 points or 1.21% downside to 1964 and 0.35% upside to 1995.

SECTOR PERFORMANCE

EQUITY SENTIMENT:

CREDIT/ECONOMIC MARKET LOOK:

- YIELD CURVE: 2.01 from 2.01

- VIX closed at 11.84 1 day percent change of 2.78%

MACRO DATA POINTS (Bloomberg Estimates):

- 8:30am: Durable Goods Orders, June, est. 0.5% (prior -1%, revised -0.9%)

- 1pm: Baker Hughes rig count

GOVERNMENT:

- Prelim. ITC ruling expected in case over U.S. allegations that Chinese, Taiwan producers dumped solar products below cost

- 9am: U.S. House Oversight/Govt. Reform Cmte hearing on campaign fundraising use in govt. offices

- 9am: FCC Consumer Advisory Cmte mtg Lifeline, broadband, stolen mobile devices

- 9:30am: House Science, Space/TechCmte marks up “Revitalize American Manufacturing and Innovation Act of 2013” (H.R. 2996)

- U.S. ELECTION WRAP: Obama Cuts DNC Debt; Mont. Race Rating

WHAT TO WATCH:

- Murdoch to sell Italy, German pay-TV stakes for $9b

- Lloyds approaches Libor settlement with U.S.-U.K. regulators

- Goldman, ADIA said to weigh joining Gavea in Fleury deal

- Fed should drop reverse repurchase facility: Bair in WSJ

- McDonald’s Japan ends sales of chicken products from China

- Russia firing artillery across border into Ukraine, U.S. says

- Israel, Hamas said to weigh U.S.-backed Gaza temporary truce

- Cynk restriction on broker shr transactions set to lift today

- Nortel U.S. unit agrees to pay bondholders $1b interest

- House to subpoena Ex-IM employee w/time running out for bank

- EMA’s CHMP decisions on Gilead, J&J expected

- KLab targets game partners in China after topping Japan charts

- Brazil’s TorreSur said to end sale as buyers balk at valuation

- Colorado city’s fracking ban thrown out; statewide vote looms

- U.K. overcomes record slump w/0.8% growth in 2Q

- Fed, U.S. GDP, Jobs Data, BP, UBS: Week Ahead July 26-Aug. 2

EARNINGS:

- Aaron’s (AAN) 7:15am, $0.35

- AbbVie (ABBV) 7:47am, $0.76 - Preview

- American Electric Power (AEP) 6:57am, $0.75

- Aon (AON) 6:30am, $1.20

- Avery Dennison (AVY) 8:30am, $0.79

- Barnes Group (B) 6:30am, $0.59

- Covidien (COV) 6am, $1.00 - Preview

- DTE Energy (DTE) 7:15am, $0.75

- First Niagara Finl (FNFG) 7:15am, $0.18

- Idexx Laboratories (IDXX) 7am, $1.06

- Lear (LEA) 7am, $1.97

- Legg Mason (LM) 7am, $0.55

- LifePoint Hospitals (LPNT) 7am, $0.55

- LyondellBasell (LYB) 6:50am, $1.92

- Moody’s (MCO) 7am, $1.02

- Moog (MOG/A) 7:55am, $1.03

- Prosperity Bancshares (PB) 6:03am, $1.02

- Silicon Laboratories (SLAB) 6am, $0.46

- Stanley Black & Decker (SWK) 6am, $1.36

- TCF Financial (TCB) 8am, $0.27

- Tyco Intl (TYC) 6am, $0.54

- Wabco Holdings (WBC) 6:30am, $1.46

- Xerox (XRX) 7am, $0.26

COMMODITY/GROWTH EXPECTATION (HEADLINES FROM BLOOMBERG)

- French Wheat Exports in Question as Rain Spoils Crop Quality

- El Nino Seen Weak or Delayed for Several Months by Forecasters

- Gold Set for Second Weekly Loss as Economic Outlook Curbs Demand

- Kudzu That Ate South Heads North as Climate Changes: Commodities

- Arabica Coffee Rises as Rain Disrupts Brazil Crop; Sugar Falls

- Soybean to Corn Prices Fall on Prospects for Ample U.S. Supply

- WTI Set for Weekly Drop Amid Rising Fuel Supplies; Brent Steady

- MORE: SK’s Refining Margins to Rise on China Economic Recovery

- WTI Crude Seen Rising in Survey on Falling Supplies at U.S. Hub

- Tin Shipments From Indonesia Seen Shrinking Most in Six Months

- German Utilities Bail Out Electric Grid at Wind’s Mercy: Energy

- Copper Traders Bearish for Third Week as Prices Seen Too High

- Zinc Record China Discount Shows Rally May End: Chart of the Day

- Rubber in Tokyo Pares Weekly Gain as Falling Oil Cuts Appeal

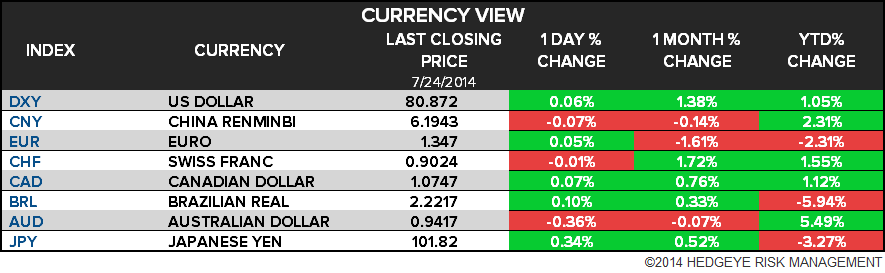

CURRENCIES

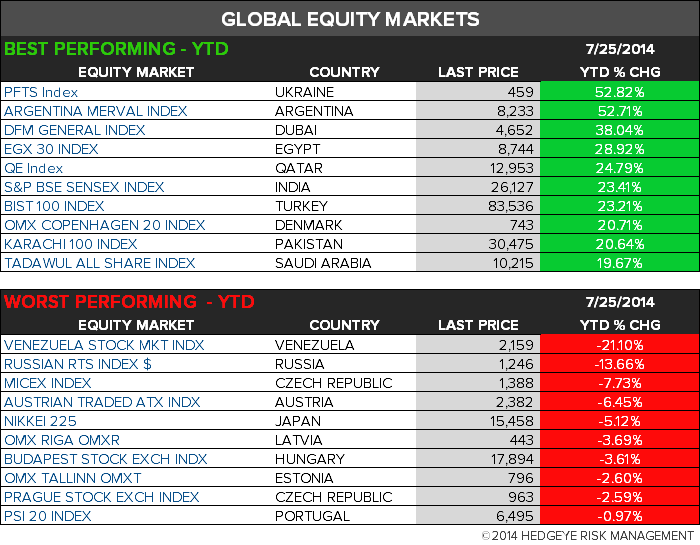

GLOBAL PERFORMANCE

EUROPEAN MARKETS

ASIAN MARKETS

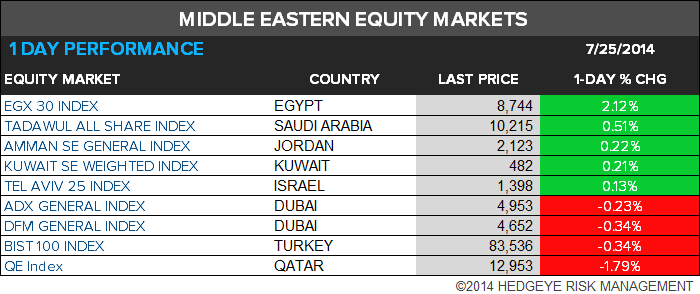

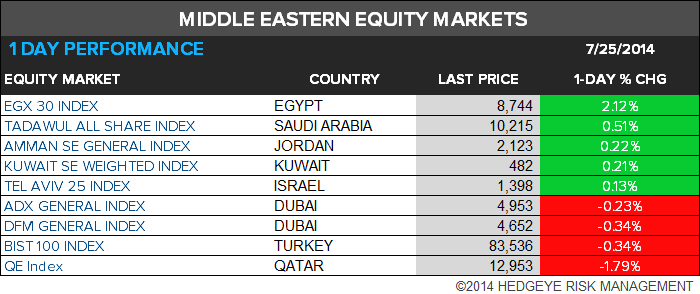

MIDDLE EAST

The Hedgeye Macro Team