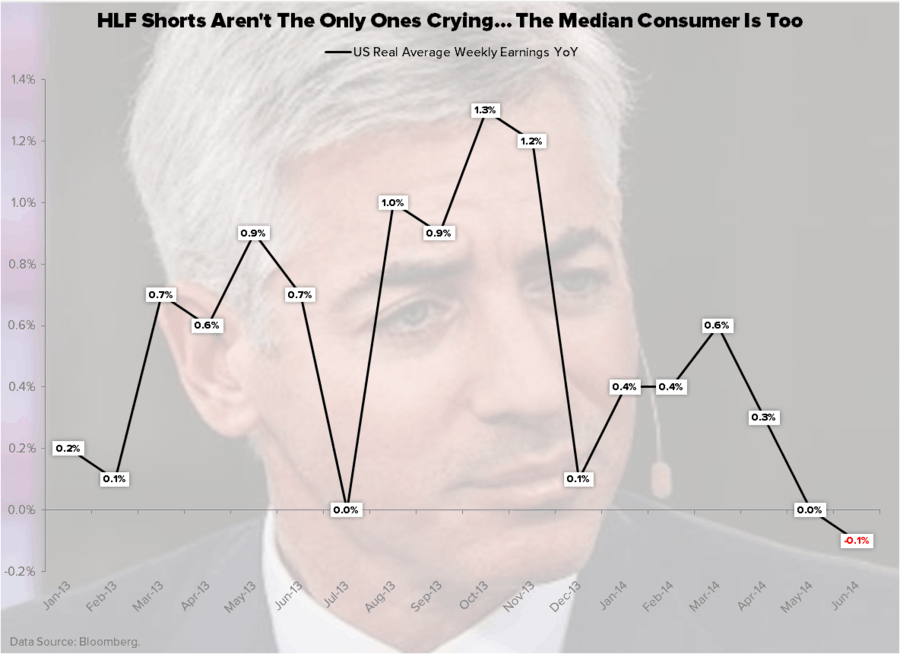

As you can see in our Chart of The Day, even the US government’s contortionist reading on US Consumer Price Inflation (CPI) delivers you a fresh new YTD low in NEGATIVE real wages (not good).

As you can see in our Chart of The Day, even the US government’s contortionist reading on US Consumer Price Inflation (CPI) delivers you a fresh new YTD low in NEGATIVE real wages (not good).

By joining our email marketing list you agree to receive marketing emails from Hedgeye. You may unsubscribe at any time by clicking the unsubscribe link in one of the emails.