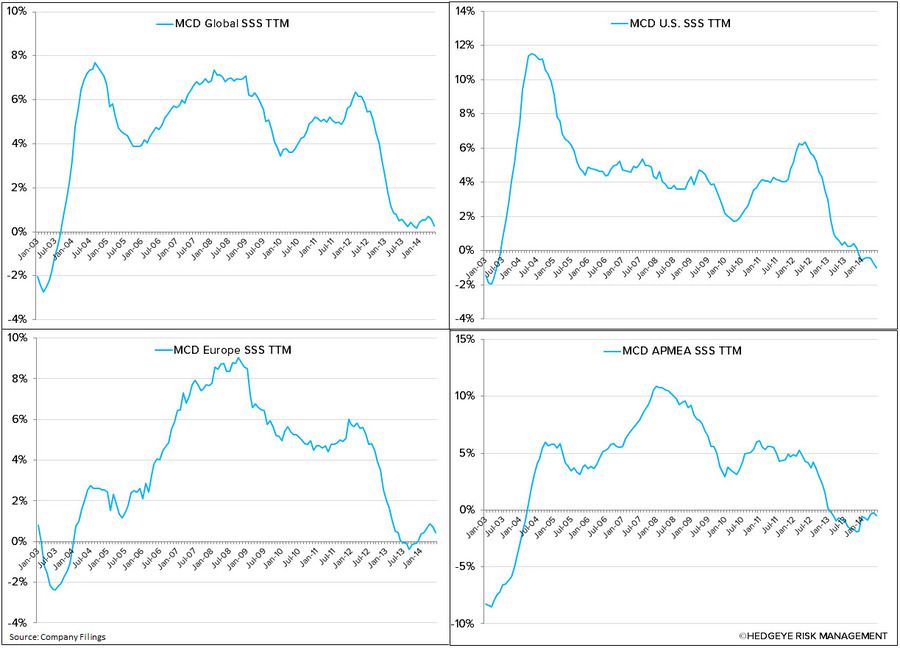

MCD reported a disappointing quarter, followed up by an even more disappointing conference call. While the phrase "sense of urgency" was used many times during the call, the current "reset plan" as outlined has very few teeth and is, in our view, unlikely to accomplish the intended results.

Given the current trends, and the lack of a credible business plan, MCD will have no choice but to undertake a major restructuring in 2015.

Until proven wrong, we continue to believe some of MCD's wounds are self-inflicted and stem from the company's attempt to be all things to all people while over-indexing the business toward beverages.

For the past two years, we've been harping on our "Espresso-Based Conspiracy Theory" as one of the reasons McDonald's is struggling to grow its top line.

In short, we believe the McCafe strategy creates additional complexity in the back of the house and diverts resources away from the core food business. We've always viewed McDonald's as a food first destination. Whenever management shifts their focus away from food and to beverages, the core business suffers. To that extent, we contend that the early success of the beverage strategy (cold beverages) successfully masked a decline in the core business (selling burgers and fries). Until the company addresses the McCafe complexity issues, it will be difficult to fix the core business.

Additionally, the company cannot seriously address the secular issues it faces until it reduces the complexity of its store operations. The company's 2014 attempt to address complexity issues by installing "high density" tables serves merely as a band-aid rather than a real solution.

Clearly, the Street is lacking confidence in the current management team and continues to dig deep into the issues the company faces. There is a lot of work that needs to be done before we'll see better trends at MCD.

Call with questions.

Howard Penney

Managing Director

Fred Masotta

Analyst