Summary

The market responded favorably to CAT’s 1Q 2014, with dealer inventory build supporting record margins in Construction Industries (CI) and an easy comp helping Energy & Transportation (E&T). From what we can see, many investors have likely mistaken 1Q 2014 results as an ‘all clear’ signal. As shown by CAT’s strong YTD performance, sentiment is far more positive going in to 2Q results. We instead expect CAT’s challenges to take somewhat longer to resolve, with 2Q 2014 and 2H 2014 estimates above what the company is likely to generate.

For 2Q 2014, however, the comps get tougher and the environment less pretty. Construction equipment sales appear weaker, particularly in Asia, as shown by Volvo and other early reporting construction equipment companies. We do not expect a repeat of CI’s record 1Q margin. Copper, iron ore, and coal prices have been weak, likely keeping Resource Industries (RI) under pressure. Weaker CI and RI sales may reduce engine volumes at Energy & Transportation, with dealer stats showing slowing in other key E&T markets. As for guidance, we are still amazed that anyone cares about a $0.25 2014 raise at a company that has seen 2014 estimates fall over the last ~18 months by >$7.00. Nonetheless, for 2Q 2014, we get a likely range between $1.44 and $1.50, below current consensus of $1.52, with sales in-line to slightly below current consensus.

Segment Expectations

Construction Industries

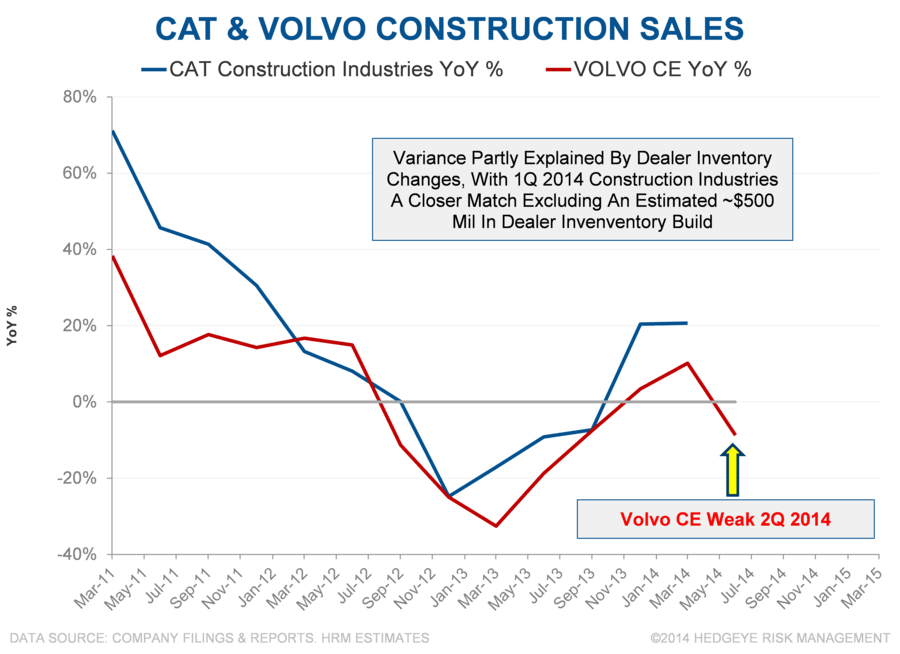

While a performance outlier in 1Q 2014, we expect CAT’s Construction Industries segment results to weaken sequentially. A significant build in dealer inventory last quarter helped drive a record margin and above industry revenue growth (see CAT: Dirty Paws or Easy Comp). Volvo CE and CAT CI sales are reasonably correlated, and more tightly correlated if we back out our estimates of CAT dealer inventory changes. As shown in the chart below, Volvo CE revenues were down ~9% in 2Q 2014.

Adjusted operating income at Volvo CE was nearly cut in half YoY. While it might be tempting to assume China will not matter for CAT, it was a factor in 4Q 2012/1Q 2013 amid a previous inventory glut. We will look for commentary on Asia construction equipment inventory and expected factory utilization.

Looking at Volvo CE results, there were largely negative signs outside of a robust North America.

Source: Volvo

CAT seemed to lower expectations for Construction Industries in the 1Q guidance, with the goal of maintaining double digit margins and 10% 2014 revenue growth. Dealer inventory build likely pulled forward sales, with guidance implying to a ~7% revenue growth rate for the remainder of the year. Margins at CI are usually fairly volatile. We have ~11% penciled in for 2Q 2014, with a lot of potential error imbedded in that estimate.

Resource Industries

CAT lowered RI 2014 top line guidance last quarter from -10% 2014 to -20%; we expect to see them do so again – perhaps this quarter. Dealer inventory changes were not identified as a factor last quarter and the environment appears to have weakened YTD. While the comps get easier on sales, weak pricing is likely to continue to pressure margins. As discussed in our recent call on Mining Equipment pricing, the time lag between order pricing and revenue recognition is significant. While we have a mid-single digit margin modeled for 2Q, we do see the potential for negative RI segment margins as the downcycle in mining capital spending drags on.

Energy & Transportation

As we have written previously, we believe CI and RI engine demand is an important source of volume across certain E&T’s engine platforms. CAT's dealer stats point to weak results for Power Generation and sequential slowing in Industrial and Transportation markets through May. Oil & Gas should prove a bit more robust, although product prices have generally weakened into 3Q, notably US natural gas. We have assumed topline growth similar to 1Q and slight margin pressure YoY amid what we expect to be weaker volume for certain engine platforms and ongoing spending to produce an emissions compliant locomotive.

Potential Upside?

Should dealers again add significant construction equipment or other inventory, we would expect a more in-line to better report from CAT. CAT may also have some flexibility to further reduce backlogged orders to keep capacity utilization high, potentially reporting better results. Of course, this tends to be the case each quarter. We suspect that large dealer inventory increases or backlog decreases might not prove as relevant to the market given the more positive current sentiment. To really move the needle from current levels, CAT may need to beat without results driven by a backlog drain or dealer inventory build.

What Could Get Us To Change Our View?

We can always be wrong and will change our views as needed. Specifically, we will be watching CAT’s cost programs closely. While we expect much more dramatic actions than the current restructuring to prove necessary, particularly in Resource Industries, CAT may be successful at executing significant change more gradually. We think it is unlikely, with hope for a rebound at Resource Industries likely to preclude the necessary rationalizations.

We will also track order rates. While we believe pricing is quite likely to continue lower in Resource Industries for at least the next year, margins may bottom somewhat earlier or somewhat later. We would expect orders for RI equipment to remain weak until a (likely muted) replacement cycle starts in the second half of this decade. Finally, we expect more significant negative feedback from weakness at RI and CI on E&T engine volumes. If that does not prove accurate or Oil & Gas capital spending accelerates, we would revise our longer-term E&T expectations.

Upshot

While 1Q 2014 benefited from inventory build at dealers and an easy comp, the set-up for CAT’s 2Q and 2H 2014 is more challenging. At the same time, 1Q results appear to have left many investors with the impression that CAT is on the mend. We think that is still a couple of years away. We expect the challenges facing CAT to take far more time to resolve, with YTD outperformance analogous to CAT’s outperformance in late-2012/early-2013 – a bounce higher in a longer-term downtrend. Assuming a cessation of inventory builds in CI, we see current consensus expectations for 2Q as too high, but calling quarters tends not to be our strategy. The current set-up is more fragile in our view: a miss in 2Q, or later in 2H, may shatter the narrative that CAT’s troubles are over.