We added DFRG to the Hedgeye Best Ideas list as a short on 06/12/14 at $27.27/share. Since then, FY14 EPS estimates have been revised down $0.05 and the stock has acted accordingly (down ~21%), led by today's post earnings sell-off. DFRG remains on the Hedgeye Best Ideas list as a short with potential downside to $18/share. As it stands, we continue to believe 2014 and 2015 EPS estimates of $1.17 and $1.43 remain aggressive.

Comps: DFRG delivered +2.3% system-wide comp growth in the quarter, tracking in-line with estimates. Del Frisco's Double Eagle same-store sales increased +5.2%, beating estimates of +3.6%, driven by a +3.3% increase in average check and a +1.9% increase in traffic. Sullivan's same-store sales increased +0.9% in the quarter, beating estimates of +0.1%. This comp growth, however, was solely due to a +5.9% increase in average check. Traffic continued to deteriorate, down -5.0%. Management does not release same-store sales data for the Grille concept. System-wide revenues of $67.386 million (+12% YoY growth) missed consensus estimates of $69.100 million by -2.48%.

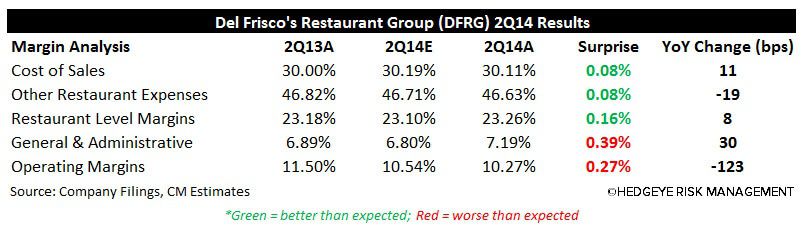

Margins: The quarter was generally in-line with expectations surrounding margin management in the quarter. Cost of sales increased 11 bps YoY to 30.11% of revenues, driven primarily by significant beef inflation though partially mitigated by 1.8% pricing, menu engineering and the natural hedge of the Grille rollout. Other restaurant expenses declined -19 bps YoY to 46.63% and led to a +8 bps YoY improvement in restaurant level margins to 23.26%. Operating margins, however, declined 123 bps YoY to 10.27%. We maintain our positioning that the company is growing at lower margins.

Earnings: Adjusted EPS of $0.20 (0% YoY growth) missed expectations of $0.21 by 4.19%. Earnings were hurt, to an extent, by common growing pains including less operating weeks than previously anticipated due to later than expected new unit openings. We reiterate our view that growing pains should be considered part of the bear case.

Brief Analysis: DFRG reported disappointing results this morning BMO, missing top line and bottom line estimates as well as guiding down FY14 EPS estimates from $0.94-0.98 to $0.90-0.94. This release, and the stock's subsequent reaction, comes as no surprise to us.

As expected, the Del Frisco's concept was strong (+5.2%), although management noted lower than expected sales at its Chicago restaurant. All told, the Del Frisco's concept has posted positive same-store sales for 18 consecutive quarters. Sullivan's, in our view, continues to be a disaster. Same-store sales increased +0.9% led by a +5.9% increase in average check and a -5.0% decrease in traffic. To be fair, management attributed 80% of the decline in guest counts to the removal of an entrée item from its menu, though we're hesitant to attribute the vast majority of the traffic decline to this. We continue to question the existence of Sullivan's as a viable concept. We also question the viability of Grille as a growth concept. Though we believe it has promise, the lack of clarity surrounding same-store sales, traffic and unit economics is concerning. Management didn't seem too confident regarding same-store sales or AUV trends. The new unit development pipeline was also pushed back toward the end of 2H14, which will result in a loss of operating weeks.

There is far too much uncertainty to be a supporter of this stock, which is partially why we assumed our bearish stance in the first place. In our view, Sullivan's is still a broken concept and the Grille is far from being considered a viable growth concept. DFRG posted $0.94 in adjusted EPS in 2012 and will only post $0.92 (or less) in adjusted EPS in 2014. These are not numbers that anyone should associate with a growth concept and they certainly don't justify the inflated multiples the Street awarded the stock when we initially added it as a Best Idea short.

As it stands, we continue to believe 2014 and 2015 EPS estimates of $1.17 and $1.43 remain aggressive.

What We Liked:

- System-wide same-store sales increased +2.3%

- Del Frisco's (+5.2% SSS) has grown same-store sales for 18 consecutive quarters

- Del Frisco's traffic increased +1.9%

- Sullivan's two-year same-store sales improved 340 bps sequentially to -0.9%

- Management has food costs under control (menu engineering; natural hedge of Grille)

What We Didn't Like:

- Top and bottom line miss

- Non-existent earnings growth

- Operating margins declined 123 bps YoY to 10.27%

- Management guided down FY14 EPS from $0.94-0.98 to $0.90-0.94

- Management tightened the low-end of its FY14 cost of sales guidance to 30.1-30.4%

- Management lowered its FY14 restaurant level EBITDA guidance from 22.9-23.4% to 22.6-23.1%

- Management raised its FY14 effective tax rate guidance to 31-32.5%

- Full-year beef inflation is expected to be in the 8-9% range

- Management expects fewer operating weeks in 2014 as several openings have been delayed

- Lower FY14 sales expectations for Del Frisco's in Chicago and Grille in Palm Beach

- Traffic declined -5.0% at Sullivan's

- Sullivan's continues to be a lousy concept, despite initiatives to save it

- Grille continues to be an unproven growth concept

- Continued lack of transparency surrounding the Grille concept

- 2013 class of Grille restaurants performing below the level of the 2011 and 2012 classes

- Management wouldn't share development plans for 2015

Research Recap:

DFRG: Thoughts into the Print (07/21/14)

Call with questions.

Howard Penney

Managing Director

Fred Masotta

Analyst