This unlocked note was originally published July 10, 2014 at 09:13 in Financials. To learn more about subscribing to Hedgeye click here.

Investment Company Institute Mutual Fund Data and ETF Money Flow:

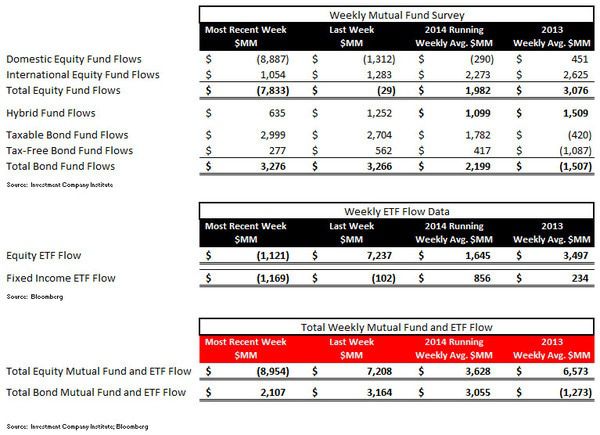

In the most recent 5 day period, aggregate bond funds including both taxable and tax free products netted another $3.2 billion in new investor subscriptions. Conversely, the combined equity mutual fund complex had substantial outflows with $8.8 billion alone coming out of domestic equity mutual funds, their 10th consecutive week of redemptions and the worst outflow in 79 weeks since the first week of 2013. The broad take-away is that the U.S. retail investor has been retrenching for most of the first half of the year (with only one week of outflows in the past 21 weeks in taxable bonds and 25 consecutive weeks of tax-free or muni bond inflows). This compares to over 2 consecutive months of outflows in U.S. stock funds. We are positioned accordingly with this emerging asset allocation having removed T Rowe Price from our Best Ideas list on May 14th and are positioned more conservatively with our ongoing Long recommendation of leading fixed income manager Legg Mason.

Total equity mutual funds put up a significant outflow in the most recent 5 day period ending July 2nd with $7.8 billion coming out of the all stock category as reported by the Investment Company Institute. The composition of the $7.8 billion redemption continued to be weighted towards domestic equity funds with a massive $8.8 billion coming out of domestic stock funds which was offset by a $1.0 billion inflow into international products. This significant drawdown in domestic equity funds was the biggest outflow in 79 weeks since the first week of 2013 and has become an intermediate term trend with now the tenth consecutive week of outflow in the category. The running year-to-date weekly average for equity fund flow is now a $1.9 billion inflow, which is now below the $3.0 billion weekly average inflow from 2013.

Fixed income mutual fund flows had a solid week of production with the aggregate $3.2 billion that came into the asset class besting the 2014 running year-to-date average inflow of $2.2 billion. The inflow into taxable products of $2.9 billion made it 20 of 21 weeks with positive flow for the category and the inflow into municipal or tax-free products of $277 million was the 25th consecutive week of positive subscriptions. The 2014 weekly average for fixed income mutual funds now stands at a $2.2 billion weekly inflow, an improvement from 2013's weekly average outflow of $1.5 billion, but still a far cry from the $5.8 billion weekly average inflow from 2012 (our view of the blow off top in bond fund inflow).

ETF results were broadly negative with outflows in both equity and fixed income products. Equity ETFs experienced $1.1 billion in redemptions, breaking two consecutive weeks of strong subscriptions, while fixed income ETFs suffered another outflow of $1.1 billion. The 2014 weekly averages are now a $1.6 billion weekly inflow for equity ETFs and a $856 million weekly inflow for fixed income ETFs.

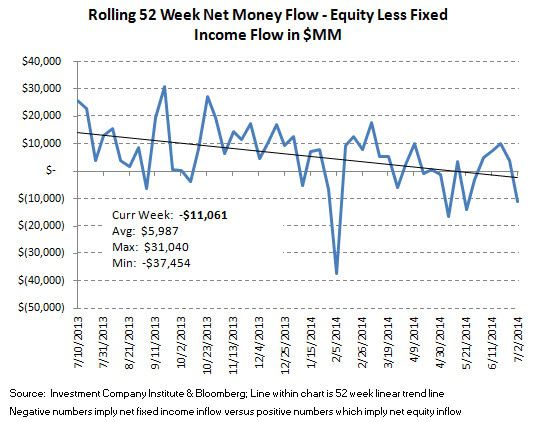

The net of total equity mutual fund and ETF trends against total bond mutual fund and ETF flows totaled a negative $11.0 billion spread for the week ($8.9 billion of total equity outflow versus the $2.1 billion inflow within fixed income; positive numbers imply greater money flow to stocks; negative numbers imply greater money flow to bonds). The 52 week moving average has been $5.9 billion (more positive money flow to equities), with a 52 week high of $31.0 billion (more positive money flow to equities) and a 52 week low of -$37.5 billion (negative numbers imply more positive money flow to bonds for the week).

Mutual fund flow data is collected weekly from the Investment Company Institute (ICI) and represents a survey of 95% of the investment management industry's mutual fund assets. Mutual fund data largely reflects the actions of retail investors. Exchange traded fund (ETF) information is extracted from Bloomberg and is matched to the same weekly reporting schedule as the ICI mutual fund data. According to industry leader Blackrock (BLK), U.S. ETF participation is 60% institutional investors and 40% retail investors.

Most Recent 12 Week Flow in Millions by Mutual Fund Product:

Most Recent 12 Week Flow Within Equity and Fixed Income Exchange Traded Funds:

Net Results:

The net of total equity mutual fund and ETF trends against total bond mutual fund and ETF flows totaled a negative $11.0 billion spread for the week ($8.9 billion of total equity outflow versus the $2.1 billion inflow within fixed income; positive numbers imply greater money flow to stocks; negative numbers imply greater money flow to bonds). The 52 week moving average has been $5.9 billion (more positive money flow to equities), with a 52 week high of $31.0 billion (more positive money flow to equities) and a 52 week low of -$37.5 billion (negative numbers imply more positive money flow to bonds for the week).

Jonathan Casteleyn, CFA, CMT

203-562-6500

Joshua Steiner, CFA

203-562-6500