Consensus estimates, management guidance and commentary, and questions for management in preparation for the earnings release/call tomorrow.

Q2 2014 CONSENSUS ESTIMATES

- Total revenues: $1.987 billion

- EPS $0.52

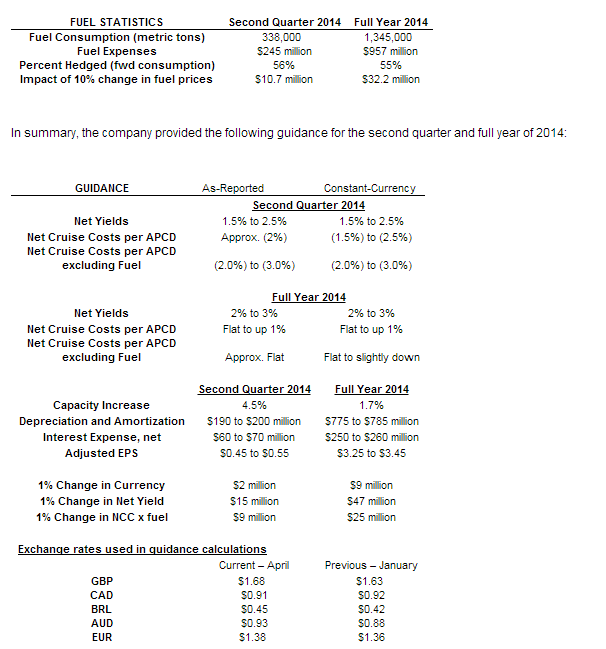

MANAGEMENT GUIDANCE

QUESTIONS FOR MANAGEMENT

-

What is the industry capacity increase in Europe for 2015? And RCL's European capacity in 2015?

-

Is the European strength mostly coming from US sourced and Asian sourced customers -- or some other part of the World?

-

Is Spain/UK still leading the way in European performance?

-

What about the impact from Israel/Gaza and Ukraine conflicts? Changes in Scandinavia/Russia deployments for 2015? Has the booking curve been more closer in for these itineraries?

-

How are Celebrity's new onboard promotions doing?

-

Is the Caribbean's heavy promotional state more of a demand or supply issue?

-

Which categories are driving onboard revenue growth e.g. casino, bar?

- Discuss early interest and booking activity for the new Australia based itineraries?

FORWARD LOOKING COMMENTARY

Asia

- Continue to see strong yield growth on sailings in Asia even with the significant capacity increase in the region.

Onboard yields

- Onboard yields... continued to see the benefits of fleet upgrades and onboard revenue management initiatives.

Booking volumes

- Booking volumes have been accelerating. The past eight weeks have been much stronger, with bookings up more than 20% year-over-year. While the strong demand trends have been partially driven by promotions available for Caribbean sailing, RCL is also seeing elevated levels of quality demand for itineraries not being discounted. So as a result, book load factors and APDs for the year are higher than same time last year.

- Demand from North America has been particularly strong at increasing prices and RCL already have more than 80% of their forecasted United States and Canadian revenue on the books. This is considerably more than same time last year.

Caribbean

- While RCL is seeing strong bookings for the Caribbean with recent booking volumes trending well above last year's levels, the environment remains very promotional. The pressure on pricing has mostly been limited to seven night and shorter Caribbean itineraries as they are seeing continued yield growth on long Caribbean sailing.

- Expect to see higher Caribbean load factors than last year during the summer. So, as Caribbean capacity for the industry is up more in Q2 than in all other quarters, it is subsequently where RCL expects to see their largest yield decline for the Caribbean.

- Still expect Caribbean itineraries to be down slightly YoY. RCL guidance expects continuation of our promotionally oriented Caribbean market environment for the remainder of 2014.

Europe

- European sailings have exceeded expectations and are booked at significantly higher load factors and prices than the same time last year. Demand and pricing have been broadly strong for these itineraries with all key source markets trending ahead.

- Finally starting to see a recovery in pricing from Southern Europe. RCL expects European itineraries, which account for 22% of their capacity in 2014 to generate double-digit improvement versus 2013 and higher yields than 2008.

- The percentage of guests booked on European sailings who have purchased their air through us has doubled year-over-year. An added benefit of our ChoiceAir program is that it increases the retention of the booking. Both our Mediterranean and Northern European products are at a higher book position than prior year and are driving elevated per diems with Mediterranean sailings doing particularly well.

- One of the markets that RCL has been particularly pleased with is the Spanish market that seems to have picked up quite nicely. And seeing strength out of the U.K. and Irish market as it relates to pricing.

Asia-Pacific

- Continue to exceed both pricing and volume expectations. China sailings which represent about 1/3 of this capacity are expected to generate double-digit yield improvement. This is in spite of a 30% year-over-year capacity increase in the market.

- 2014 summer China season is booked far ahead of the same time last year at higher rates.

Quantum of the Seas

- Currently in a very encouraging booked position in terms of both load factor and pricing

Alaska

- Alaska yields to increase in the low to middle single digit range and to be similar to yields in record 2011 season.