Investment Ideas

The table below lists our Investment Ideas as well as our Watch List -- a list of potential ideas that we are in the process of evaluating. We intend to update this table regularly and will provide detail on any material changes.

Recent Notes

07/14/14 MONDAY MASHUP: YUM ON DECK

07/15/14 YUM: THOUGHTS INTO THE PRINT

07/17/14 YUM: EARNINGS RECAP

07/18/14 CMG: THOUGHTS INTO THE PRINT

07/18/14 DRI: PERPETUALLY MISGUIDED (FOR 46 MORE DAYS)

Events This Week

Monday, July 21st

- CMG earnings call 4:30pm EST

Tuesday, July 22nd

- DFRG earnings call 8:30am EST

- DPZ earnings call 10:00am EST

- MCD earnings call 11:00am EST

Wednesday, July 23rd

- CAKE earnings call 5:00pm EST

Thursday, July 24th

- DNKN earnings call 8:00am EST

- BJRI earnings call 5:00pm EST

- SBUX earnings call 5:00pm EST

Friday, July 25th

- No events

Chart of the Day

Recent News Flow

Monday, July 14th

- EAT Brinker was upgraded to overweight at JP Morgan with a $52 PT.

- RRGB announced it is two weeks away from opening its newest restaurant on Long Island.

Tuesday, July 15th

- MCD Janney released a report noting the growing long-term threat McDonald's is facing from privately owned Chick-fil-A.

- RRGB completed an acquisition of 32 franchised restaurants in the U.S. and Canada for approximately $40 million in cash.

- DRI Starboard delivered a letter to the Board of Darden, calling for new leadership and a series of operational improvements.

Wednesday, July 16th

- BOBE delivered a letter to stockholders stating their case for the Board's director nominees at the annual meeting on August 20th, 2014.

Thursday, July 17th

- CAKE The Cheesecake Factory announced that its licensee, S.A.B. de C.V., opened its first restaurant in Mexico (Guadalajara, Jalisco).

- TAST Carrols Restaurant announced its agreement to acquire 21 Burger King restaurants from Kessler Group, Inc.

- MCD announced a quarterly cash dividend of $0.81 payable on September 16, 2014 to shareholders of record on September 2, 2014.

Friday, July 18th

- No news

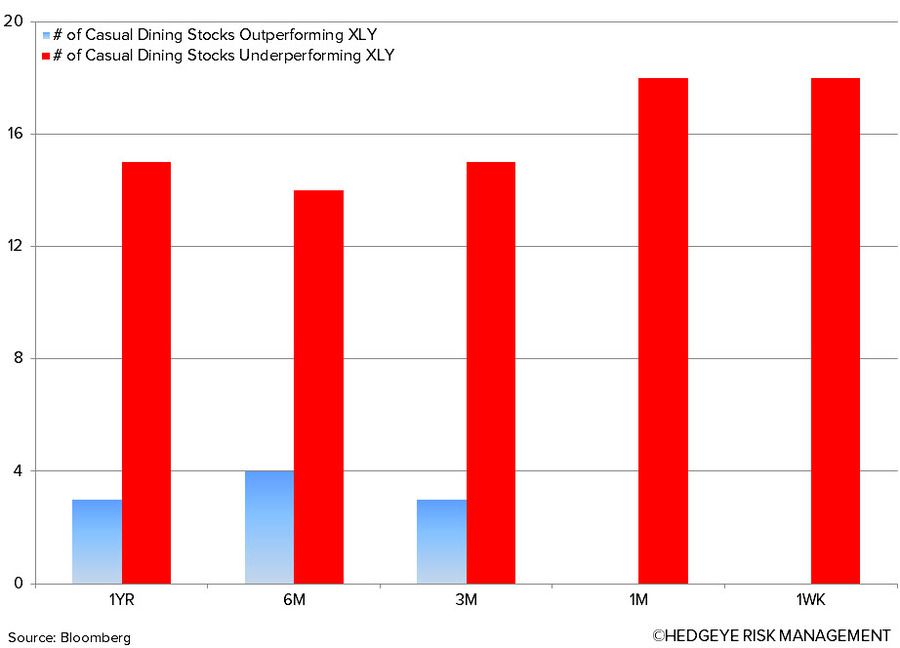

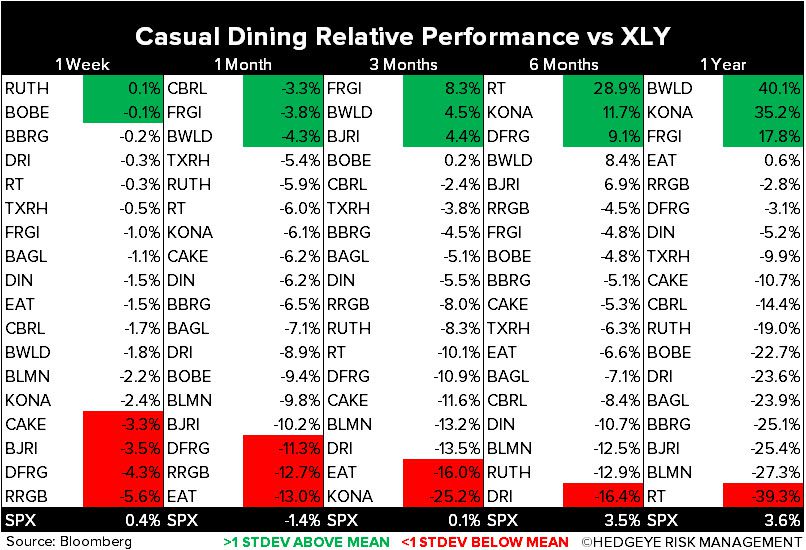

Sector Performance

The XLY (+0.2) underperformed the SPX (+0.5%). Both casual dining (-1.6%) and quick service (-0.7%) stocks, in aggregate, undperformed the XLY Index.

Consumption

The Hedgeye U.S. Consumption Model is signaling bullish, with 7 out of 12 metrics flashing green.

XLY Quantitative Setup

From a quantitative perspective, the sector remains bullish on an intermediate-term TREND duration.

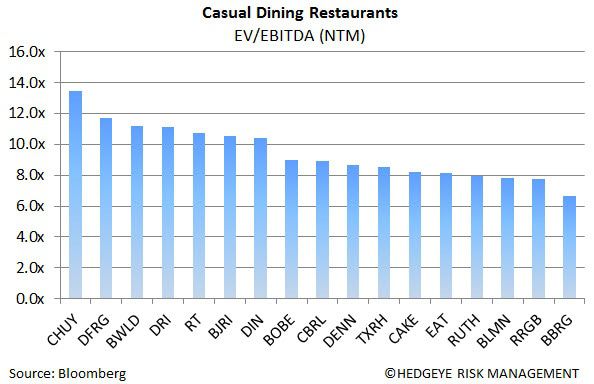

Casual Dining Restaurants

Quick Service Restaurants

Howard Penney

Managing Director

Fred Masotta

Analyst