This note was originally published at 8am on July 07, 2014 for Hedgeye subscribers.

“Each circle of time has a great moment of discontinuity.”

-The Fourth Turning

No, the stock market is not the economy. And the bond market is not the stock market. Everything is relative to its own rate of change. On that score, I think the US economic cycle is about to meet another great moment of discontinuity.

“In the ancient view, a new round of time does not emerge gradually from the last but only after the circle experiences a sharp break” (The Fourth Turning, pg 31). The Hedgeye Macro Model is hardly ancient, but Mr. Market’s respect for mean reversion within long-term cycles is.

After a -2.9% GDP print in Q1, the Old Wall’s latest victory lap on US growth came in the form of a classic lagging economic indicator last week – headline employment data. Since our models focus primarily on rate of change, it wasn’t surprising to see the slope of private wage growth remain negative. #InflationAccelerating and real-wages tracking negative for the first time in two years should ensure #Q3Slowing.

Back to the Global Macro Grind…

On Thursday afternoon, we shorted SPY for the 1st time (in Real-Time Alerts terms) since February 10th, 2014, on that. Well, maybe not only on that. You see, having a view on an economy within the Global Macro marketplace is pretty much useless unless you have some repeatable mechanism (read: #timing signal) that tells you when the probability of acting is falling into your favor.

With literally no volume trading in US Equities on Thursday (at the all-time highs), here’s the multi-factor, multi-duration, risk management signal I was looking at:

1. US DOLLAR – bouncing to lower-highs for the 1st time in 2 weeks, but still well below $81.17 TAIL risk line (USD Index)

2. US RATES – bouncing to lower-highs for the umpteenth time in 2014, but well below 2.81% TREND line resistance

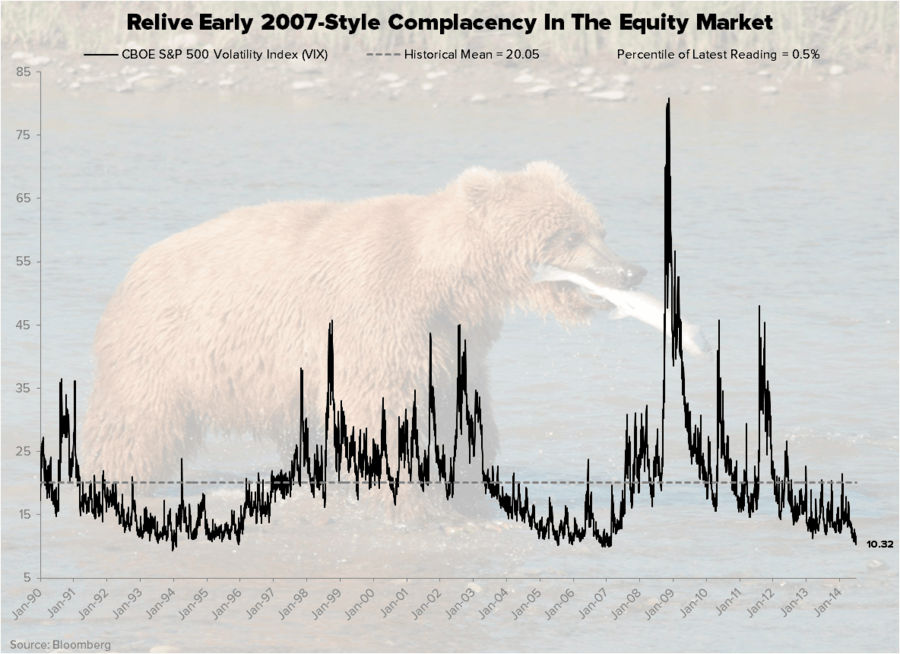

3. VOLATILITY – front month VIX testing its all-time lows, closing at 10.32 (it has never held below 10, sustainably)

Yes, never (in mean reversion terms) remains a very long time. So it’s a lot easier to make the SELL call on US domestic consumption growth today than it was when the Old Wall didn’t agree with us 6 months ago.

But consensus wouldn’t want to do that now, would it? How about you? If I’m right, you are going to crush your competition (newsflash: your competition in US Growth Equities is called levered long beta), just like you did from January 1st to the May 2014 lows.

If I’m wrong, well, consensus is going to be really right.

Strapping on the accountability pants is fun right here and now because the more bearish you are on US growth in Q3, the more you can get invested (on the long side) in what is going to be perpetuating outflows from US domestic equity funds:

1. Long Inflation (Commodities, Energy Stocks, Gold, etc.)

2. Long Bonds + Anything That Looks Like A Bond (love those #GrowthSlowing Yield Chasers!)

3. Long Foreign Currencies + Emerging Market Stocks (vs USD short)

This is when making a macro call matters – when you get those rare Moments Of Discontinuity in markets where you can put a lot of money to work. Sounds crazy, but this is much like the moment you had on JAN 1 to buy Gold and Utilities (+10% and +12% YTD, respectively).

To be crystal clear on this, we aren’t calling for the next Lehman – we are using our process to make an ole school consumption-cycle call. When the cycle is in phase transition, you get paid to shift your Style Factoring for the part of the cycle that you are entering.

In our process-speak we call this moving from the 2nd quadrant to the 3rd (within a 4 quad model using 2-factors, Growth & Inflation). Not unlike how Strauss and Howe explain “four-phase time” of the seasons, this risk management framework helps us simplify the complex.

“Time’s circle moves not only from cold, to hot, to cold but also from growth to maturity to decay to death.”

-William Strauss and Neil Howe (The Fourth Turning)

And while the “decay to death” part is not what I wake up thinking about in the morning, it does happen. Countries and companies slow too - and so does the confidence The People have in things like central-planning and the stock market’s last price being the economy.

Our immediate-term Global Macro Risk Ranges are now:

UST 10yr Yield 2.50-2.67%

SPX 1946-1989

VIX 10.11-11.54

USD 79.73-80.35

Pound 1.69-1.71

Brent Oil 110.03-112.99

Gold 1310-1330

Best of luck out there today,

KM

Keith R. McCullough

Chief Executive Officer