“Because we naturally seek self-confirming information, we need discipline to consider the opposite.”

-Chip Heath

That quote comes from a block and tackle #behavioral chapter in Decisive titled Consider The Opposite (pg 114). If I was ever seeking self-confirming evidence of US GDP #GrowthSlowing, this morning I’ve got plenty of headlines on that.

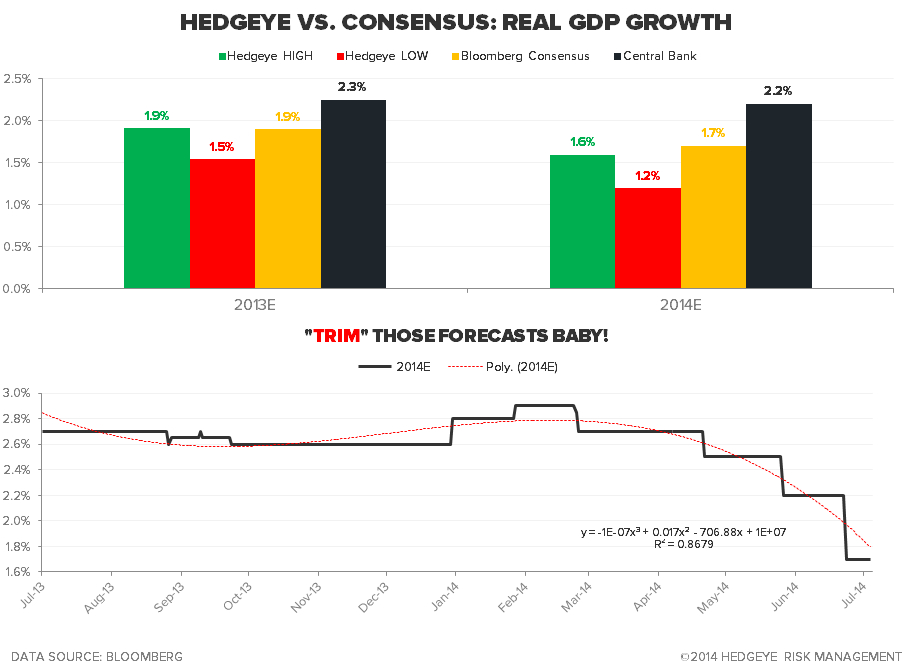

The cover of this week’s The Economist has a picture of an American jockey riding a turtle with a header that reads: “America’s Lost Oomph – Why It’s Long-Term Growth Rate Has Slowed.” And on Friday, the WSJ ran a story titled “Survey Shows Economists Trimming Growth Forecasts.”

#Trimming? With both bond yields and the Russell 2000 US growth index falling back toward their YTD lows, isn’t the market telling us to go all-in US growth investing? No thanks. The only discipline that matters in considering the opposite of our research view is delivered to us daily via real-time market signals.

Back to the Global Macro Grind…

The best part about The Economist and Wall Street Journal articles is that they attempt to explain US #GrowthSlowing with the wrong reasons. The Economist, in its classic Keynesian style, suggests that the Fed keeping rates at 0% remains critical to growth and that the government needs to both spend more and expand immigration. #MustPrintAndSpendMoarrr

My colleague Darius Dale comically summarized the WSJ article this way on Friday: “Net Exports are a solid negative ~2% of US GDP… not sure how “negative international events” can ever be the largest downside risk to US GDP growth. Consensus Macro can’t even get their story straight at this point.” #BlameTheWeather

In other words, those who were looking for +3-4% 1990s style US GDP growth 6 months ago should cite anything but what’s slowing 70% of the number (US Consumption = 70% of GDP). And, whatever they do, they shouldn’t blame The Policy To Inflate’s impact on real cost of living in America either.

In other self-confirming USA #Q3Slowing news, here’s what big macro markets signaled last week:

- Russell 2000 lost another -0.7% on the week, falling back to -1.0% for 2014 YTD

- US 10yr Treasury Yield dropped another -4bps on the week, and is down -55bps YTD

- Yield Spread (10yr minus 2yr) compressed another -7bps on the week to fresh YTD lows

Don’t kid yourself, the economists who are now cutting their GDP forecasts know exactly what falling bond yields and a compressing yield spread means. On the other side of that, this is what consumption growth bulls are saying:

- Food prices dropped -0.1% last week

- Natural Gas dropped -4.7% last week

- Gold dropped -2.1% last week

Too bad you can’t eat Gold. If you contextualize those three data points however:

- Food Prices (CRB Food Index) is still up +19.1% YTD

- Natural Gas has round tripped back to flat YTD

- Gold made another higher-low and is up again this morning to +9.3% YTD

So, from an asset allocation perspective, what would you rather be long YTD – Gold or the Russell? That one is too easy to answer. How about The Dow, Coffee, or Cattle?

- Dow Jones was +0.9% last week to +3.2% YTD

- Live Cattle prices were up +1.8% last week to +17.7% YTD

- Coffee prices were up another +6.8% last week to +47.2% YTD

I know. Instead of citing the all-time high in both US rents (34% of the country rents) and meat prices during BBQ season, let’s talk about the corn chart rolling over from its all-time bubble highs as a “deflationary force” when the Food Index is +19% YTD.

As for the SP500, which hasn’t been as much a focus for us in 2014 as the #GrowthSlowing style factors within the market, there are plenty of components that we like on the #InflationAccelerating (Energy, XLE +11.8% YTD) and slow-growth #YieldChasing (Utilities, XLU +12.6% YTD) front.

I even went smart beta last week and sent out the buyback signal on AAPL during its correction to what we call immediate-term TRADE oversold (within a bullish intermediate-term TREND). While I can’t feed my kids iPads, apples are eatable – and, compared to a $12 “gourmet burger”, relatively “cheap” too!

Our immediate-term Global Macro Risk Ranges are now:

UST 10yr Yield 2.46-2.54%

SPX 1

RUT 1133-1155

VIX 10.32-13.70

WTI Oil 100.50-103.41

Gold 1

Best of luck out there this week,

KM

Keith R. McCullough

Chief Executive Officer