TODAY’S S&P 500 SET-UP – July 18, 2014

As we look at today's setup for the S&P 500, the range is 21 points or 0.47% downside to 1949 and 0.61% upside to 1970.

SECTOR PERFORMANCE

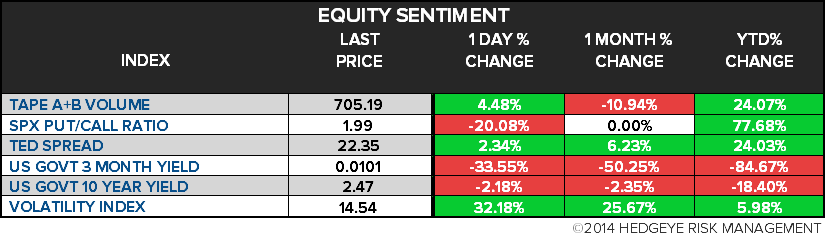

EQUITY SENTIMENT:

CREDIT/ECONOMIC MARKET LOOK:

- YIELD CURVE: 2.01 from 2.00

- VIX closed at 14.54 1 day percent change of 32.18%

MACRO DATA POINTS (Bloomberg Estimates):

- 9:55am: UofMich Consumer Sentiment Index, July prelim., est. 83 (prior 82.5)

- 10am: Leading Economic Indicators, June, est. 0.5% (prior 0.5%)

- 1pm: Baker Hughes rig count

GOVERNMENT:

- House, Senate out

- 12pm: Congressional Internet Caucus Advisory Cmte holds panel discussion on NSA surveillance programs

- UN Security Council holds emergency meeting on MH17 crash, may take place at 3pm

- U.S. Election Wrap: Colo. Dead Heat; Immigration Concerns

WHAT TO WATCH:

- Ukraine, Russia point fingers over downed Malaysia plane

- United Nations Security Council to discuss MH17 crash

- Israeli forces carry out Gaza entry via land, sea

- AbbVie to buy Shire Pharmaceutical for $55b in cash, stock

- Line said to seek U.S. IPO with confidential SEC filing

- McDonald’s workers claim co. fired them for union activity

- American Apparel investor said to be close to buying loan

- DoJ alleges FedEx role in delivering misbranded drugs

- SEC looking at 10 firms in probe of high-speed trading

- Microsoft job cuts provoke Finnish demands of worker support

- Energy Future lenders gang up to force talks on rival plan

- Amazon considering subscription service for e-books: NYPost

- Union plans more strikes at 9 German Amazon sites: Bild

- Petsmart talking with investment banks amid activism: WSJ

- Twitter to roll out 4 new metrics with earnings: WSJ

- CBS interested in CNN purchase if channel becomes available

- DirecTV offering NFL package via web at 10 universities

- IMF, Home Sales, Apple, Facebook, Ifo: Week Ahead July 19-26

EARNINGS:

- Bank of New York Mellon (BK) 6:30am, $0.57

- First Horizon National (FHN) 7am, $0.16

- General Electric (GE) 6:30am, $0.39 - Preview

- Honeywell Intl (HON) 7am, $1.36 - Preview

- Huntington Bancshares (HBAN) 5:55am, $0.18

- Interpublic Group (IPG) 7am, $0.25

- Johnson Controls (JCI) 7am, $0.83

- Kansas City Southern (KSU) 8am, $1.17

- Laboratory of America (LH) 7:03am, $1.77 - Preview

- VF Corp. (VFC) 7am, $0.35 - Preview

COMMODITY/GROWTH EXPECTATION (HEADLINES FROM BLOOMBERG)

- WTI, Brent Set for First Weekly Gain in a Month on Ukraine, Gaza

- Gold Declines as Investors Weigh Dollar Against Global Tensions

- Cocoa Grinding in Asia Climbs as Demand for Chocolate Increases

- Glencore’s Woman Director Marks Progress for Mining: Commodities

- ANZ Tightened China Commodity Financing Processes ‘A Little’

- WTI Crude Seen Rising in Survey on Falling U.S. Supplies

- MORE: Shanghai Exchange Copper Stockpiles Rise 29% to 108,851 Mt

- Ban on U.S. Oil Exports Seen Dying One Ruling at a Time: Energy

- Corn Volatility Rises as Options Traders Bet on Price Rally

- Wheat Set for Weekly Climb as Investors Assess Black Sea Outlook

- Buzzard Field Power Restored After July 13 Outage, Nexen Says

- Colorado Governor Says He Opposes Measures Restricting Drilling

- Kurdish Oil Grab Fuels Independence Dream as Iraq Unravels

- Copper Traders Bearish for a Second Week as Supplies Seen Ample

CURRENCIES

GLOBAL PERFORMANCE

EUROPEAN MARKETS

ASIAN MARKETS

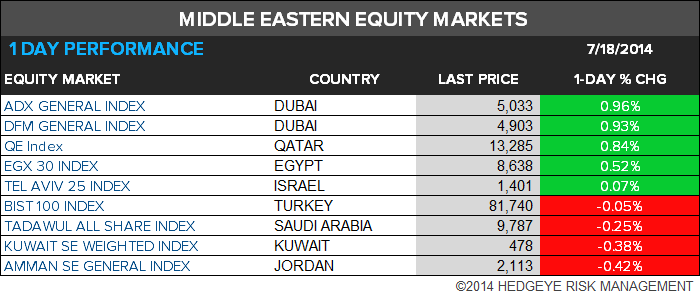

MIDDLE EAST

The Hedgeye Macro Team