Below is the detailed breakdown of this morning's initial claims data from the Hedgeye Financials team led by Joshua Steiner. If you would like to setup a call with Josh or Jonathan or trial their research, please contact

You Know, the Jungian Thing

The first chart below summarizes where we are in the labor market from a historical context. Allow me to suggest something akin to the duality of man. On the one hand, we're seemingly in a great place. Claims are near their historic lows at 309k (rolling SA). Look back at the last three periods in time when claims were comparably low. You'd be looking at the periods of December, 2005, April, 1999 and August, 1987. All those periods were auspicious as they were accompanied by a rapidly rising stock market and an ongoing economic expansion. On the other hand, they were also all in relatively close proximity to major market corrections: 2 months away in the case of August, 1987, ~2 years away in December, 2005 and ~1 year away in April, 1999. Such is the dilemma of where we stand today. We're standing on the tracks and we know the train is coming, but we don't know if it's 2 months or 2 years away. #Conundrum.

[HEDGEYE MACRO]: An alternate approach to the “where are we in the cycle” question is examining how long, after having reached their frictional lower bound, have claims tracked at a level generally considered (by the market) to be “good”.

On average, over the last three cycles, claims have held below the 330K level for ~33 months. The present streak currently stands at 5 months.

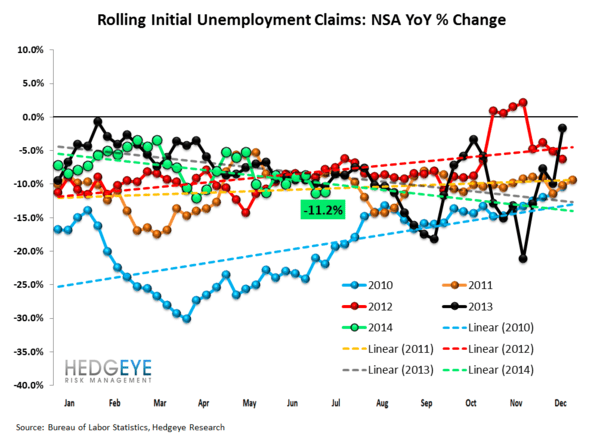

The chart below speaks to just how strong the data is at the moment. By the way, it's important to remember that seasonal auto manufacturing furloughs occur at this point every year, but last year, due to strong demand, they went largely unutilized. Furloughed autoworkers are eligible to file for claims. As such, seeing the NSA Y/Y prints come in as strongly as they are suggests things really are quite good (at the moment).

The Data

Prior to revision, initial jobless claims fell 2k to 302k from 304k WoW, as the prior week's number was revised up by 1k to 305k.

The headline (unrevised) number shows claims were lower by 3k WoW. Meanwhile, the 4-week rolling average of seasonally-adjusted claims fell -3k WoW to 309k.

The 4-week rolling average of NSA claims, which we consider a more accurate representation of the underlying labor market trend, was -11.2% lower YoY, which is a sequential deterioration versus the previous week's YoY change of -11.4%

Joshua Steiner, CFA

Jonathan Casteleyn, CFA, CMT