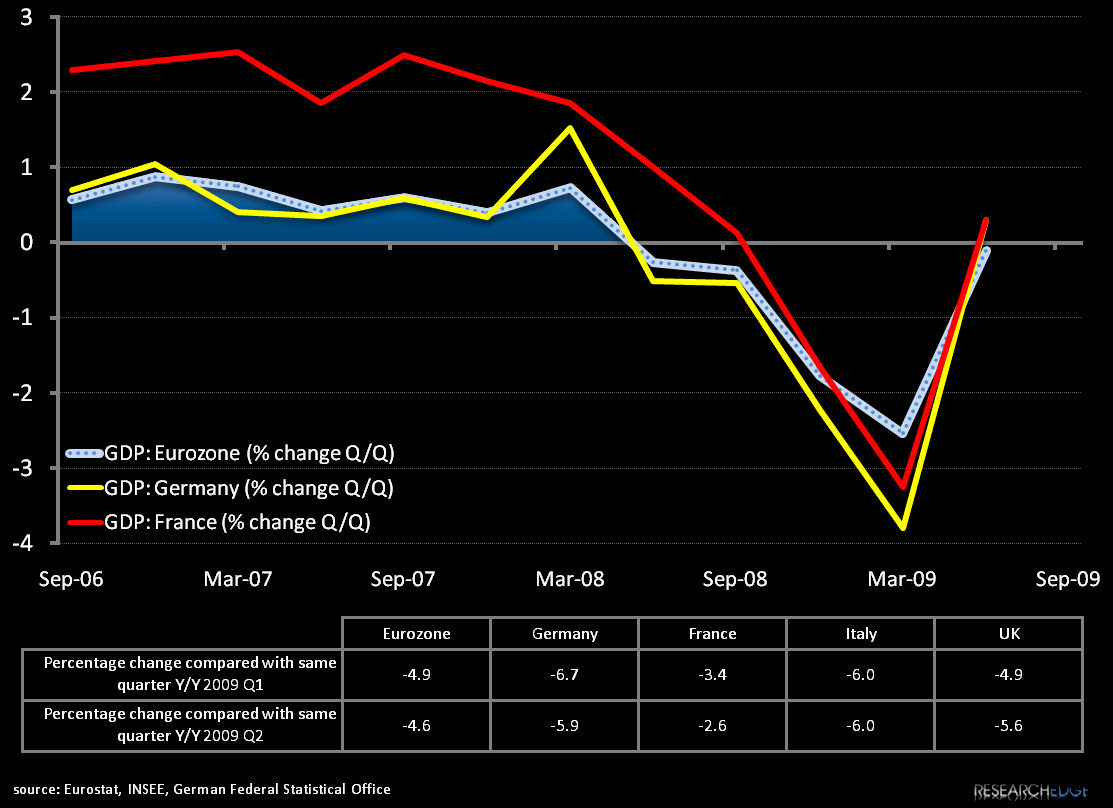

European markets traded higher today on Europe’s Q2 GDP numbers. Today’s report from Eurostat helps confirm the improving fundamental landscape for the region that we have been reporting on, as Eurozone growth declined 0.1% on the quarter, but rebounded substantially from Q1’s 2.5% contraction.

For more on our Western European view, see our post “Taking Cues from Europe’s Larger Economies” on 8/11, however as a call-out, today’s numbers on an individual country basis further substantiate the divergence among Western Europe’s larger economies: Germany and France rose 0.3% in Q2 quarter-on-quarter, while Italy and the UK, though improving sequentially, still registered in negative growth territory at -0.5% and -0.8% respectively (See chart below). On an annual basis all countries lie firmly in negative territory, yet when comparing Q2 annual results with Q1 year-on-year, Germany and France saw improvement, while Italy was unchanged and the UK declined.

As we measure the relative winners and losers in Europe, GDP remains a lagging indicator, yet markets trade day-to-day on lagging indicators as our CEO Keith McCullough has alluded to many times. The DAX closed up over a percent today and the Euro and Pound moved higher versus the USD. As a side note relating to our German thesis, today’s positive GDP number should provide further support for Chancellor Angela Merkel’s CDU party, who is polling over a 30% spread over her challenger Frank-Walter Steinmeier of the Social Democrats, as national elections approach on September 27th.

Matthew Hedrick

Analyst