Conclusion: This is one of the most hated stocks in retail. We understand the bear case, but think it’s foolish to be beared-up on a name when sentiment is at its worst, valuation is bordering on cheap, and growth is on the verge of reaccelerating.

This one is a head-scratcher. WWW beat the Street’s EPS expectation by 15% – putting up a better-than-expected top line, a positive reversal in Sperry (which is a lightning rod for this stock), and gave every indication that the productivity of international distribution agreements is improving (this was critical for us – see write up below). Yes, EPS was driven in large part by lower SG&A growth, but that was known heading into the quarter. The stock was up 8% pre-market, but then once the call got underway it cratered, and is down 2%. The primary culprit is that guidance was very ‘Wolverine-ish’, meaning that the company reaffirmed the year, but lowered the upcoming quarter – so it can beat it handily in another 13 weeks. In addition, we think that people will be concerned that the company will back away from its long term revenue target. We’re really not concerned about either of these things.

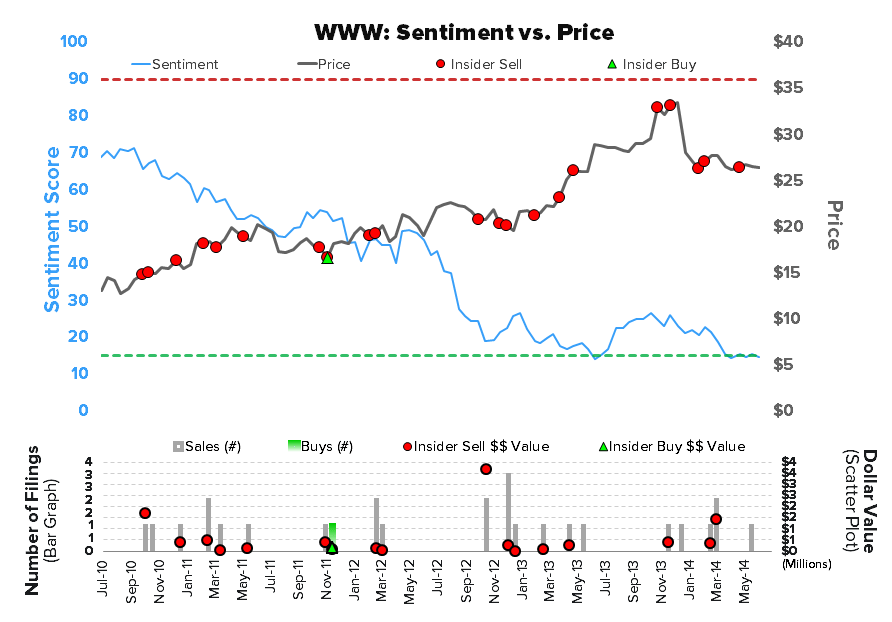

One thing that never ceases to amaze us is how much people love to hate this company. We’ve all seen companies that are perennially hated, but seriously, pull up a 20 year stock chart for WWW. It does not strike us a management team and business model that’s worth betting against for anything more than brief periods of time. Our Sentiment Monitor below, which combines Sell Side rankings with Buy Side short interest and assigns a quantitative score, shows just how hated WWW is today. When the Sentiment score gets below that dotted green line in the chart, it almost always signals a contrarian time to buy (the inverse holds true for stocks with sentiment above the red line).

Here’s something to think about from a timing perspective on WWW as it relates to its PLG acquisition.

1) Year 1: Even though the deal was consummated in 2012, it really only benefitted 2.5 months of the year. The real ‘Year 1’ was 2013. This was a breakout year for the stock as WWW blew away EPS estimates as it immediately realized revenue and cost synergies from the deal. The stock was up 66% for the year, more than double the market. It really served as the poster child as to why you want to own a stock in the first year after a transformational acquisition.

2) Year 2: Unfortunately, we’re in this year right now. We’re in the back half. But we’re still in it. In deal terms, we’ve anniversaried the Year 1 euphoria of synergies, and are still building the infrastructure to support organic top line growth and margin expansion. This begins in Year 3. Unfortunately, growth investors don’t want the stock at this point in its cycle, and it’s probably not cheap enough for value investors. GARP investors might look at it, but there’s not enough ‘G’ in the GARP equation here given a tough start to the year in US retail.

3) Year 3: 2015 – this is when we actually start to see a reacceleration in growth due to the investments that were made in years 1 and 2 of the acquisition. In WWW’s case, it will be an extension of the International growth that we’re starting to see in its numbers as Keds, Sperry, Saucony, & Stride Rite grow more aggressively overseas. That plus accelerated growth in e-commerce across all of its brands. In the end, we think that we’ll be looking at growth rates 2x what we see today.

The punchline is that today’s stock move definitely takes away what little wind WWW had in its sail, which we clearly don’t like. But when we step back, the reality (as we see it) is that the stock is bombed out, sentiment is simply abysmal, it is trading at 14x earnings and 10x EBITDA when earnings and cash flow have a long-term CAGR of 20% and 25%, respectively. That might be justified if it the business was decelerating. But we think we’ll see an inflection in 2H, and then a material acceleration in 2015. That should start to be discounted in the back half of this year -- to some degree. It might be sleepy and boring, but we like this name in the mid-$20s.

7/14/14

WWW: THOUGHTS INTO THE PRINT

This WWW quarter to be reported tomorrow is an important event for our confidence in our Long thesis. To be clear, we’re not too worried about the EPS number. We think that looks fine. We’re at $0.28, about a penny above the Street, which would represent a 22% growth rate in EPS compared to a 6% decline in 1Q. The consensus view is that the revenue is weak, and that the company will make up for it with lower pension expense. That’s mostly correct, but well-telegraphed. We shouldn’t see any downward revision to guidance for the year. If anything we think WWW will beat and keep FY guidance steady, implying that 2H will be lower (that’s what it always does). Keep in mind that the company was at the FFANNY trade show in early June where it held 1-on-1s, and then presented at a broker’s Consumer Conference. Both of those happened just 1-2 weeks before the quarter closed June 14th. In other words, WWW knew its numbers, and likely would have preannounced at that time if it thought the quarter or year was at risk.

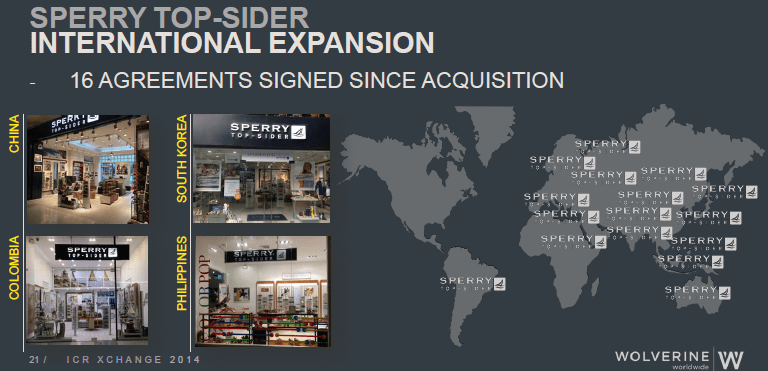

The key thing we’re looking for, however, is a) the number of international distribution arrangements signed for Sperry, Keds, Saucony and Stride Rite, and b) the revenue generated by the deals that have already been signed. Why is this so important? The crux of the investment opportunity here is WWW scaling up the International distribution for the four PLG brands. It already has the most efficient international distribution network of any footwear company in the world, with better than 60% of its shoes sold outside the US across a network of 210 distributors over 11,000 points of distribution. All of them are on SAP, and all are exclusive to WWW. Conversely, the PLG brands generated only 5% of its sales outside of the US due to the inefficiencies of being under the umbrella of its former owner, Collective Brands (Payless). When we look at the timeline associated with this deal, organic international growth should be ramping up right now. Here’s the timeline…

PLG Acquisition Timeline

- 2012 was the year of the PLG deal (4Q12). It was big, and painful initially – no EBIT, just interest from $1.2bn in debt.

- 2013 was the year of integration. In 1H people moved around, brands were repositioned, and management realigned. Then in 2H the chessboard was largely set, but they had to seal the deal with an SAP implementation, which went without a hitch.

- Then comes 2014 – which should be all about revenue growth. The global salesforce, which is the most efficient footwear distribution operation on the planet, has four new major tools (brands) in its toolbox. WWW has been lining up international distribution arrangements over the past 18 months and is now sitting on about 55. Aside from each of those arrangements getting more productive, there’s still another 150 that could be added by our estimates.

Here’s what the company has said in its last seven public appearances about its cadence in signing new deals.

- Q2'13 CC (Jul ‘13): almost 20 distribution agreements in key growth markets and anticipate another 15 to 20 programs will come online in the back half of 2013

- Q3'13 CC (Oct ‘13): We continued to make progress on this front during the quarter by signing and executing distribution agreements covering 14 key growth markets, bringing the total number of new agreements since closing to nearly 35 covering 67 countries.

- Investor Day (Oct '13) : Since acquisition, we've signed 35 new agreements covering 67 countries, and we're very excited about certainly the most recently inked agreements with the Elan Corporation for the Sperry Top-Sider and Keds brand for the China market.

- ICR (Jan '14):

- Q4 '13 CC (Feb '14) : significant investments to build out the full Sperry Top-Sider lifestyle assortment. We have seven license agreements in place today for everything from swimsuits to sun glasses and our most exciting initiative, the introduction of a full range of Sperry apparel via license agreement with Li & Fung is scheduled to launch this coming fall... We've signed 15 to 20 new contracts for Sperry. We still only have Sperry in about 67 countries around the world, for example.

- Q1'14 CC (Apr '14): During the quarter, we signed agreements covering over 25 key growth markets, bringing the total number of new agreements since closing to nearly 55, covering nearly 85 countries.

- Baird Conference (May '12): And as we noted in our earnings call last week, since the acquisition closed, we've signed 55 new distribution agreements for the newly acquired brands covering 85 markets. And so those distribution agreements are in place.

So there are 55 agreements in place as of May, and probably close to 70 today. We’re ahead of the consensus this quarter due to revenue growth associated with these arrangements. If we’re wrong, then we’ve got to step back and question our logic, math and thesis. But based on what we know today, we’re comfortable owning this one.