Gold tested its long-term TAIL Line of resistance at $1324/oz. at the end of last week. Spot contracts backed-off yesterday fueled by Goldman’s call for a move off the highs by the end of the year. Their prediction induced some big selling in front-month COMEX futures ahead of their earnings report today and Yellen’s testimony:

Spot Volume:

- +28% vs. 5-Day Avg.

- +57% vs. 1-Month Avg.

Like us, they cited growth, and consequently interest rates as a driver. We will look for some read-through on the Fed’s expectations with Yellen’s commentary today at her semi-annual testimony to the Senate Banking Committee. We continue to be of the view that she will be forced to echo a more dovish tone as we progress towards the September meeting:

Hedgeye Position:

- #Inflation Accelerating continuing to be consumer headwind; growth miss warranting easier policy on the margin:

- Commodities catch a bid perpetuating the consumer headwinds already manifest (long-gold, short USD bias)

- Yield spread compression reflects forward-looking growth expectations

- Top-line pressure on high-multiple, early cycle consumer stocks (consumer based-sectors)

- Sector variances observed in growth-slowing sectors outperforming to the upside (Energy, Utilities, REITs, TIPS, Long-End of the Treasury curve)

Because of this bearish set-up on rates (for now), we remain long of Gold into the second half of the year (TREND Support = $1272):

- Front-Month COMEX Futures +30 bps today off the down move

- Yield Spread: -30 bps day-over-day

We re-entered on the long-side in real-time alerts yesterday on the oversold signal.

To further clarify our bullish position, the thesis stems from our view that growth would likely turn from accelerating to decelerating moving into Q1 2014. A link to the full write-up from Darius Dale along with a summary review of his main points is included below. We will stick with the same position here with the willingness to change our view with the relevant catalyst:

From November 26th, 2013:

- “#GrowthSlowing: We think monetary and fiscal policy uncertainty (mostly monetary policy uncertainty) will weigh on consumer and business confidence. Furthermore, GDP comps get difficult as CPI/GDP deflator comps get easier, at the margins.

- #InflationAccelerating: We think domestic disinflation is now a rear-view phenomenon as easy comps and a weak dollar provide upward pressure on CPI and PPI readings.

- #IndefinitelyDovish Monetary Policy: We are increasingly of the view that the Fed is aware of the systemic risk present in the bond market and is potentially setting up to never commence tapering. They will likely accomplish this by setting far-too-aggressive targets for GDP growth and shifting their focus to combating a perceived risk of deflation, at the margins.

Historically, moves by the US into Quad #3 have been bullish for the price of gold, as both the US dollar and real interest rates tend to decline in this economic “state”; the opposite holds true on a move into Quad #1 (i.e. #GrowthAccelerating as #InflationAccelerates), which is where both the reported data and consensus expectations have tracked throughout much of 2013. Given where we’ve been on growth and inflation for much of the year, it would be modest to say that we are not surprised to see gold down almost -26% YTD (we’ve been the bears on gold for much of the past 12-18M).”

Gold: Is it Time To Get Back In on the Long Side?

With the gold outperformance year-to-date, has the bull market run its course over the last six months?

We still like it on the long-side for the same reasons and will continue to buy at the low end of our immediate-term TRADE risk-range on the signal that selling has been exhausted to the downside.

Full-year growth expectations from the Fed have already been downwardly revised since we made the call moving into this year (GLD +11% YTD) and are still likely too optimistic:

The markets expectation of fed tapering leaned on an improving growth outlook moving into the year. This expectation for a steepening in the long-end of the yield curve has reversed as growth has slowed:

- 10-year Treasury Net Futures and Options Contracts at CBOT from the CFTC:

- December 31, 2013: -176K (Tapering expectations putting upward pressure on rates)

- May 20, 2014: +49K (Capitulation on Q1 GDP print, #inflation accelerating)

- July 8, 2014: -68K (rates can’t go any lower)

- Yield Spread YTD: (10yr – 2yr): -22% YTD to +206 bps wide

- Actual and/or rhetorical easing of policy relative to previous expectations

- The USD is expected to weaken under the feds predictable, linear model for countering high-frequency economic data points. Below is a squeeze of real-purchasing power despite a flat dollar YTD:

- USD Index: +23 bps

- CRB commodity Index: +5.6%

- Investors choose gold over a depreciating currency:

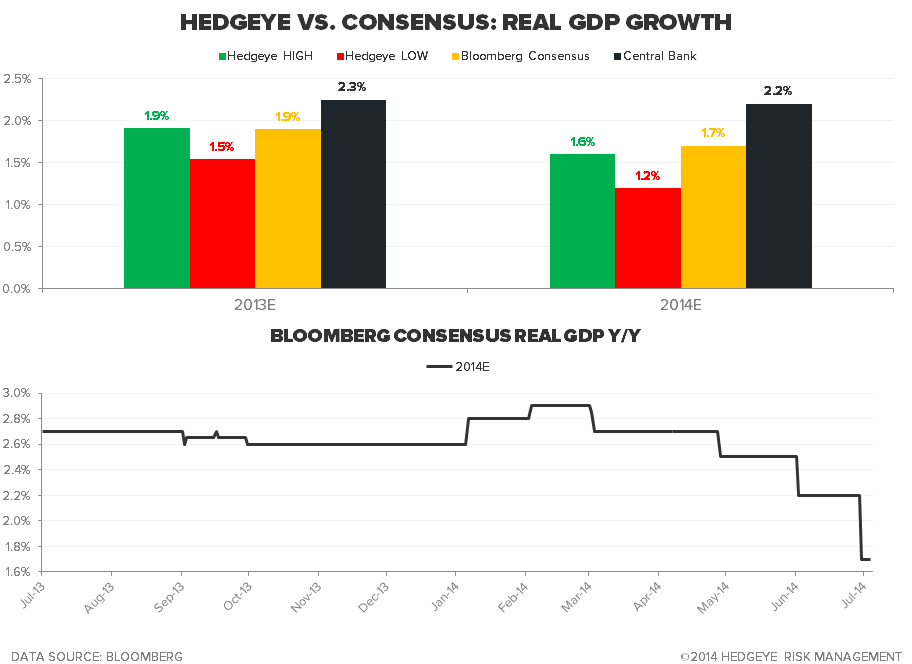

The GIP model (Growth, Inflation, Policy) which predicts forward-looking growth and inflation indicates growth expectations from both the fed and consensus macro are still too optimistic…

The policy response should our predictive model play-out is key to #Dollar Devaluation driving the upward pressure on Gold. Growth will miss relative to expectations (although the predictive gap has tightened), and, in now Pavlovian fashion, investors will move to hedge a devaluing currency (rotation into Gold Over dollars).

On the growth miss, the fed responds with more money in the system and #dollar devaluation squeezes consumer margins. Inflation expectations still set-up to miss vs. Hedgeye estimates:

Using 2013 as a case study, the relationship between the relative convexity of growth and inflation influencing a monetary policy response with U.S. dollar implications can be observed under both upside and downside surprises.

From the time we wrote the following positive note on the USD and consumer vs. bearish gold call on March 1st, 2013 to our bullish gold call on November 26th 2013 gold decreased -21%. We took this stance in observation of the exact same catalyst:

The growth and inflation outlook influencing the forward-looking expectation for the dollar

A few points to highlight from Christian Drake’s March 1st, 2013 note are included below along with a link the full article:

- “Positioning:

- Short Basic Materials: Materials is the worst looking sector across the S&P from a quantitative perspective and has direct negative leverage to commodity deflation

- Long Consumption: A Real-time tax cut via energy deflation is positive for real earnings growth and discretionary income. We like Consumption oriented/Consumer Facing equities in the U.S. and select Asian equity markets (China, Hong Kong)

- Short Gold: To the extent that U.S. dollar strength is reflective of growth and interest rate expectations (or just the expectation for a cessation in easing) we think gold holds further downside over the intermediate term.”

USD Redux: 3 Ways The Dollar Wins

The relationship between the price of gold vs. forward growth/policy expectations and the change in the Fed balance sheet discretely illustrates the point.

To re-iterate our position, we continue to be short of the U.S. consumer and long of defensive and late cycle sectors which outperform as growth decelerates and inflation accelerates. The divergence below appears to have more room to run in the third quarter.

2014 YTD:

- SPX: +7.0%

Underperformers: Consumption-Driven

- RUSSELL 2000: 0.3%

- Consumer Discretionary (XLY) : +1.1%

Out-Performers:

- GLD: +8.4%

- Treasuries (TLT): +10.8%

- Utilities (XLU): +11.8%

- REITs (REIT Index): +17.9%

- Energy (XLE): +12.0%

Ben Ryan

Analyst