This note was originally published at 8am on June 30, 2014 for Hedgeye subscribers.

“Without cycles, time would literally defy any kind of description.”

-The Fourth Turning

From a performance reporting perspective, it’s both month and quarter end today. As William Straus and Neil Howe recently reminded me in The Fourth Turning, “The words year and hour come from the same root as the Greek horos (solar period)… and the word month is a derivative of moon.”

Time and price put more pressure on us than most things in this profession. We just need to take a few deep breaths every once in a while to contextualize both. “We need to recall that time, in its physical essence, is nothing but the measurement of cyclicality itself.” (The Fourth Turning, pg 13)

After one of the lowest volume months in US equity market history, where are market prices within the context of the future? What is the US economic cycle (and bond market) telling you vs. the US stock market’s last price? Does history matter?

Back to the Global Macro Grind…

Straus/Howe do a good job arguing that most academics who are trying to become famous in the social sciences with “it’s different this time” are disrespecting time and space. “This scholarly rejection of time’s inner logic has led to the devaluation of history throughout our society” (pg 12).

While it might work in disruptive technologies, devaluing history, time, and cycles rarely works in Macro… “so”, let’s embrace the uncertainty born out of these measurable risk factors and get on with Q3.

One of the Top 3 Global Macro Themes we’ll roll with for Q314 (we’ll be hosting our Institutional Investor conference call next week) is simply going to be #Q3Slowing. US growth slowing, that is.

Nope, God didn’t call us this weekend. Here’s where we’re finding conviction in this out-of-consensus view:

- The Currency Market

- The US Bond Market

- The US Equity Market

Why?

- FX – US Dollar Index (down for 2 straight weeks) remains below both our TREND ($80.84) and TAIL ($81.19) risk lines of resistance

- TREASURIES – 10yr Yield -7bps last week (-49bps YTD) remains below both our TREND (2.81%) and TAIL (2.65%) risk lines of resistance

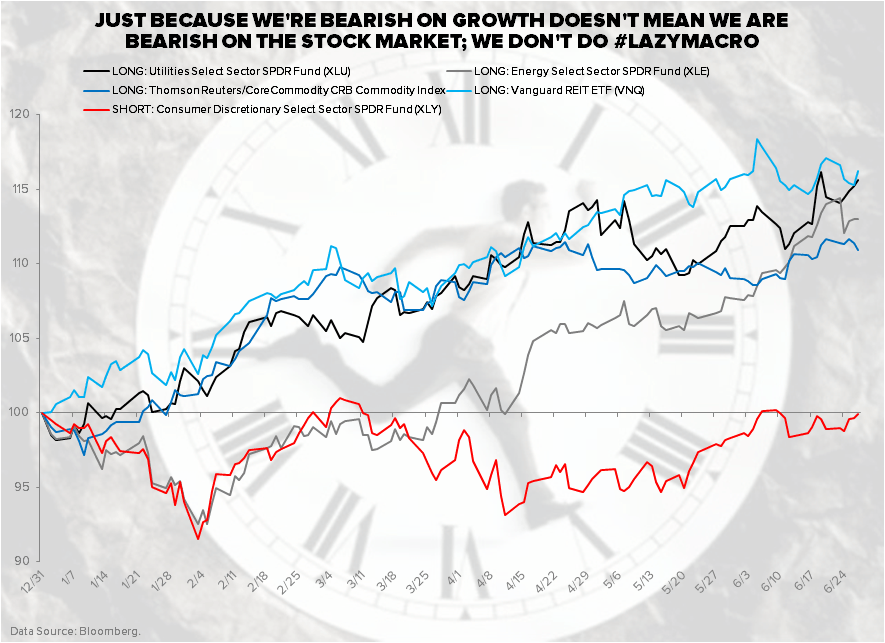

- US EQUITIES – slow-growth Utilities (XLU) were up another +1% last week to +15.6% YTD (Consumer Discretionary is still down YTD)

And those are just the quantitative signals (time/price) augmenting our baseline research views that:

- The Fed is perpetuating inflation via its #DownDollar Policy To Inflate

- As the Dollar declines, #InflationAccelerates and real-consumption growth slows

- As real-growth slows, inflation + slow-growth #YieldChasing strategies (long Bonds, Utilities, etc.) #win

Who cares if an ideological and un-elected central planning committee doesn’t get paid to acknowledge time and space? All you have to do is listen to Mr. Macro Market’s inner logic and you’ll beat your peers in generating risk adjusted returns.

Food prices (CRB Foodstuffs Index) were up another +0.5% to +23.5% YTD last week. Cattle led the charge on that front, closing up another +3.6% on the week to +25.9% YTD. Being long of that and short Del Frisco’s (DFRG) cost of goods sold (and traffic slowing) works for us.

Or how about being long the lover of all things slow-growth-#YieldsFalling, Gold? Gold was up another +0.3% last week to +9.6% YTD (vs. the Dow +1.7% YTD). But, after 4 consecutive up weeks, you want to be buying ze #GrowthSlowing Gold on red, not green!

In a Fed Easing, Down Dollar, and #InflationAccelerating environment, there are so many places to put your money that I’ll run out of time and space in this morning’s rant. To recap, here are some of the bigger asset allocations we continue to like:

- Fixed Income (still loving TIPs and Treasuries)

- Foreign Currencies (still loving the Canadian, Mark Carney, at the Bank of England #StrongPound)

- Commodities (Gold, Oil, Food, etc.)

- International Equities (India, Brazil – i.e. most of the markets we didn’t like last year)

- US Equities (Utilities, Energy Stocks, Healthcare Stocks, Semis, etc.)

In other words, without embracing the uncertainty of where we are going in the macro cycle, my writing to you every market morning would literally be useless. #History teaches us that knowing where you are going in markets requires contextualizing where you’ve been.

Our immediate-term Global Macro Risk Ranges are now:

UST 10yr Yield 2.51-2.60%

SPX 1944-1969

BSE Sensex 24976-25652

USD 80.01-80.37

Pound 1.69-1.71

WTI Oil 105.16-106.99

Gold 1305-1345

Copper 3.12-3.20

Best of luck out there today,

KM

Keith R. McCullough

Chief Executive Officer