We were recently given a look at June sales and traffic trends from Black Box Intelligence which were, in aggregate, disappointing for casual dining industry. Both same-store sales and traffic declined during the month. Before we delve further into the details of the release, we thought it'd be useful to highlight the changes in same-store sales estimates from the beginning of 2Q (April 2nd) to today (July 11th).

The street took up 2QC14 SSS estimates over the course of the quarter for the following companies: BWLD, CAKE, CHUY, DFRG, KONA, RRGB, RT, TXRH.

The street took down 2QC14 SSS estimates over the course of the quarter for the following companies: BBRG, BJRI, BLMN, BOBE, CBRL, DIN, DRI, EAT IRG, RUTH.

The street left 2QC14 SSS estimates unchanged over the course of the quarter for DENN.

We continue to like DFRG on the short side and believe same-store sales estimates, which have risen over the course of the quarter, are too aggressive. In particular, we have serious doubts that Grille and Sullivan's will post a +3.4% and a +0.1% comp, respectively.

Despite a rather disappointing quarter, revisions to same-store sales estimates were fairly mixed leading us to believe that expectations are too high for several companies. Casual dining stocks have underperformed both the SPX and XLY, in aggregate, over a 1YR, 6M, 3M, 1M and 1W duration.

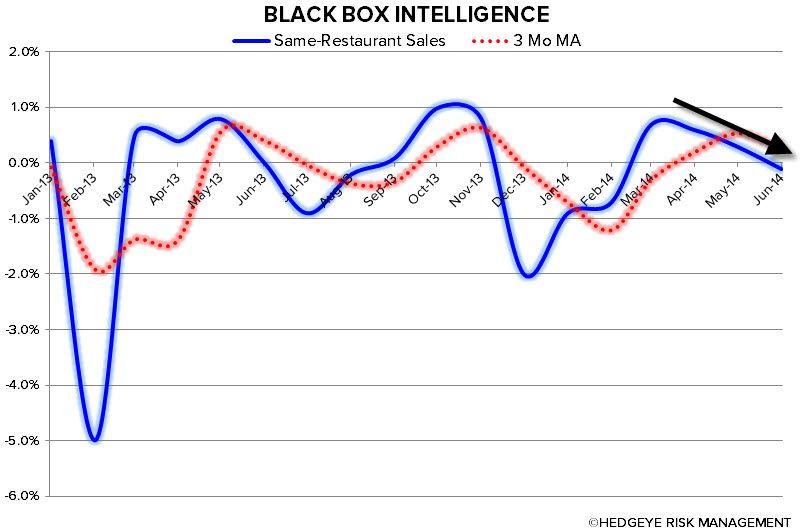

June was the worst month of the quarter, with same-store sales and traffic down -0.10% and -1.7%, respectively. The underlying trends were similarly concerning, with two-year same-store sales and traffic down -0.1% and -2.1%, respectively. Notably, each month in the quarter was worse than the prior. This is consistent with the discounting trends we've seen in the industry. As food cost pressures continued to build throughout the quarter, casual dining companies decreased their level of discounting in order to protect margins. In turn, traffic suffered which leads us to believe it's a "pick your poison" environment for casual dining operators right now.

Weather, which was the scapegoat in 1Q14, can no longer be used as an excuse. Rather, we point to a number of issues including stagnant wages, rising gasoline prices and what we've deemed "casual dining's secular decline." Overall, 2Q14 was a disappointing quarter as same-store sales increased +0.3%, while traffic declined -1.4%. These results are, however, an improvement over a tumultuous 1Q14.

Black Box also noted that the best performing region was Mountain Plains (SSS +2.1%; traffic -0.6%) and the worst performing region was NY/NJ (SSS -2.6%; traffic -3.5%).

Trends in the casual dining industry have been rather unsettling to us. While the bulls blamed weather in 1Q and predicted a strong 2Q, that clearly didn't materialize. In fact, we'd argue that looking at our proprietary Casual Dining Index, same-store sales estimates of +1.4% in 2Q14 are far too high. Unless estimates come down further, this should make for some interesting earnings releases!

Call with questions.

Howard Penney

Managing Director

Fred Masotta

Analyst