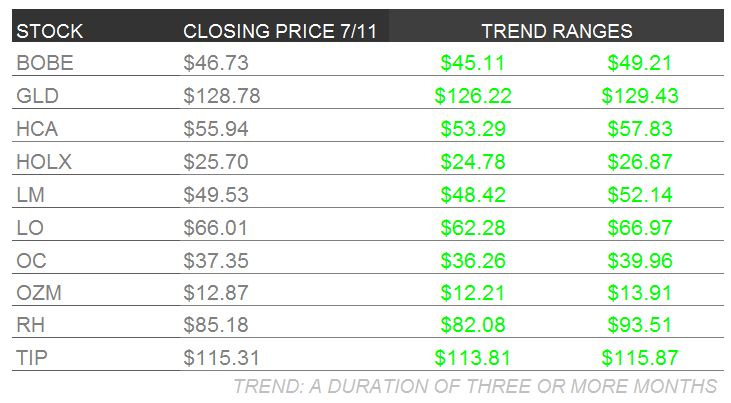

Below are Hedgeye analysts' latest updates on our TEN current high-conviction investing ideas and CEO Keith McCullough's updated levels for each.

*Please note that we added Bob Evans Restaurants (BOBE) to Investing Ideas this week. We will send out a full report this coming week.

We also feature two recent institutional research notes, as well as Keith McCullough's Friday morning macro call, all of which offer valuable insight into the markets and economy.

Trade :: Trend :: Tail Process - These are three durations over which we analyze investment ideas and themes. Hedgeye has created a process as a way of characterizing our investment ideas and their risk profiles, to fit the investing strategies and preferences of our subscribers.

- "Trade" is a duration of 3 weeks or less

- "Trend" is a duration of 3 months or more

- "Tail" is a duration of 3 years or less

HEDGEYE CARTOON OF THE WEEK

IDEAS UPDATES

BOBE – Restaurants sector head Howard Penney added Bob Evans Restaurants to Investing Ideas earlier this week. We will send out his report next week outlining his bullish case.

GLD – Gold broke out above its long-term TAIL Line of $1324/oz. this week and we remain long into the second half of the year (TREND Support = $1272). We added GLD to investing ideas in May and we still like it here for the same reasons outlined in our report.

Full-year growth expectations from the Fed have already been downwardly revised since we made the call moving into this year (GLD +11% YTD). The revised expectations for growth are reflected in the bond market. The market expected Fed tapering as growth improved. This expectation for a steepening in the long-end of the yield curve has reversed as growth has slowed:

- Yield Spread (10yr – 2yr): -22% YTD to +206 bps wide

- More money is expected to enter the system relative to previous expectations (tapering slower-than-expected so far)

- The USD is expected to weaken under the feds predictable, linear model for countering these data points

- Investors choose gold over a depreciating currency

Our GIP model, which predicts forward-looking growth and inflation, indicates growth expectations from both the Fed and consensus macro are still too optimistic. Growth will be slower than expected, and investors move to hedge a devaluing currency (rotation into Gold Over dollars).

On the growth miss, the Fed responds with more money in the system and dollar devaluation squeezes consumer margins. We continue to be short of the U.S. consumer and long of defensive sectors which outperform as growth decelerates and inflation accelerates. The divergence below which has already taken-shape will continue to generate alpha into the third quarter. This divergence is perpetuated from the policy response to overly optimistic expectations:

Underperformers: Consumer-Driven

- RUSSELL 2000: -0.30%

- Consumer Discretionary (XLY) : +0.5%

Out-Performers:

- GLD: +11%

- Treasuries (TLT): +11%

- Utilities (XLU): +14%

- REITs (REIT Index): +17%

- Energy (XLE): +11%

HCA – We received the results for the June/July installment of our monthly physician survey. As it relates to HCA, it appears patient volume appears solid through 2Q14. The results were not completely without issue, but there were two Key Drivers we are most focused on. The first is volume reported by physicians who have a high percentage of commercially insured patients, and practices with higher income patients, both of which remain positive on a rolling 3-month basis. The other is maternity trends. Our model using monthly data from the US Census and yields a birth forecast is pointing to acceleration which the June physician survey data is now confirming both for reported pregnancies and deliveries. At 25% of hospital inpatient volume, we should see sequential improvement in admissions from here.

Orthopedics is holding up. As we have commented on previously, the Orthopedics surgical arena is the largest by revenue for the Hospital industry. Incidentally, Biomet reported their recent quarter earlier this week and while growth slowed sequentially, the results continue to show positive growth.

HOLX – CMS did not offer any comment on reimbursement for 3D breast tomosynthesis when they released their proposal for 2015 rates. The commentary included only a proposal to eliminate codes created for digital reimbursement several years ago transition the rates to codes currently used to reimburse for film based mammography. We were expecting more, but we’ll look for the final rule which will be published in October.

Our Pap survey continues to suggest a manageable decline in Pap volume of -10% over the coming 2 to 3 years. In a separate analysis of the data, we may be overestimating the total decline. It appears physicians who consider themselves compliant with the Cervical Cancer Screening Guidelines currently test a higher percentage of women on 1 year intervals than we would expect. The total decline from here, if their testing intervals are where the market stabilizes, the rate of decline from here for Pap testing approaches -5%, a much better outcome for Hologic.

LM – Legg Mason reported its June ending assets-under-management (AUM) on Friday morning with another inflow into its fixed income product suite which was offset by slight outflows in its equity funds. Being that LM has over 50% of its AUM in fixed income (versus 27% in equities and 19% in money markets), it is their bond results that matter most. With June tallies now in, which complete the company’s first quarter period (calendar second quarter), Legg’s results are quite impressive.

LM netted $2.5 billion in new fixed income flows in calendar 2Q14 alone which is more than the entire annual period of 2013, where LM netted just $1.1 billion in new bond business.

We continue to view the Legg as an underappreciated turnaround story that is still not recognized by the Street with low sell-side sentiment and also stubbornly high short interest. We think the next leg of the LM’s trajectory higher will be driven by deal making, as Legg as refinanced its long term capital and has been a successful acquirer and integrator of other asset management companies.

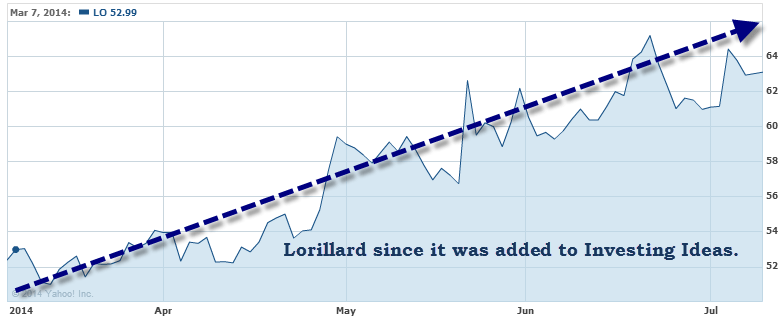

LO – Big news Friday … all parties that may be involved in a deal to acquire Lorillard (directly or not) acknowledged through press releases that in fact the parties are underway in discussions, yet noted that there is “no certainty that any deal will take place.” This not-so-new-news (rumors have persisted since March of this year of a deal between RAI and LO), bolted LO as high as 5%+ intraday (to $66).

We are riding out our long position in LO, which we added to Investing Ideas on 3/7/14, to a price target of $80. We expect to see RAI and LO work closely to get this deal done, and attach an 85% probability that a deal in fact gets done. Assuming Thursday’s (7/10) closing price of $63.09, we assume there’s an additional 26% upside to our target, and around 8% of downside to $58 should a deal not get done.

OC – Next Wednesday on July 16, we are hosting a special call with Bob McNally, a former General Manager of TAMKO Building Products. TAMKO is among the top four largest companies in the U.S. Asphalt Roof Shingle industry. Here are some of the key points we will cover:

- Were margins unsustainably high for the industry coming into 2Q?

- How do producers react to changing input prices & demand trends?

- What are the relative competitive advantages and cost structures of the key competitors?

- What is driving downward pressure on roofing prices? Is it inventory overhang?

Even with the drop in roofing sales we still believe it is better for OC to hold price than gain market share. Management even mentioned a stronger back-half of the year for its roofing business is still in the cards. With that said, insulation and composite margins are reverting back to their long-term averages. The uptick in the other segments’ sales can help recoup losses from the often volatile roofing segment and add overall improvement to OC’s operating profits.

Owens Corning reports earnings on Wednesday, July 23rd.

OZM – Och Ziff Capital Management had a soft week of stock performance as most of the Financial sector declined on emerging fears of renewed banking system weakness coming out of Portugal. OZM as a leading hedge fund has quite a bit of beta sensitivity (the stock is quite sensitive to broader market reactions) and thus the 4% decline during the past 5 days is not unexpected or overly worrisome to us.

The fundamental picture for OZM continues to brighten with its monthly multi-strategy performance for June, which was released last week, having being quite positive again. OZM stock sold off sharply in March and April as the firm’s core multi-strat portfolio spit off negative performance, however this trend has reversed with positive performance in May and June.

OZM continues to have the industry’s fastest organic growth rate in new client assets at 24% year-to-date supported by a U.S. pension fund market which is heavily allocating to Alternatives. With a 5% dividend yield on core management fees alone and an additional 4% yield possible on year end incentive fees, there are many ways to get paid on an investment in OZM.

RH – We will be releasing our second Black Book on Restoration Hardware next week, outlining in specifics the key issues that we think are critical to our investment thesis and the stock price at this point in the company’s growth trajectory. The reality is that some of the key factors to this story deserve greater scrutiny today than they did just $30 ago.

We’ll hit on several topics, but the key focus will be real estate. The crux of our commentary will focus on the likelihood of success in RH’s buildout of its large format Full Line Design Galleries. We’ll outline the biggest opportunities, potential risks, and whether or not the company is set up to execute on this opportunity.

Ultimately, we’re going to flesh out the real estate profile and potential store growth in the same way and using the same tools many retailers use to analyze their own store growth opportunity.

KEY TOPICS WILL INCLUDE:

- What does RH’s addressable market look like, and how will that evolve over the next five years?

- How many markets in the US can support a Full Line Design Gallery at the sales productivity standards that RH is setting for its’ new stores?

- A look at trends we’re seeing in anchor tenant space, and why we’re seeing more premium space available than most people might think.

- Category expansion, and which categories present the biggest opportunities (and potential risks) at retail.

- How much of a risk is a housing downturn to the RH story?

Look for updates on our work in the coming weeks.

TIP – It was a semi-quiet week on the domestic inflation front. The US Dollar Index was flat-to-down WoW, while the CRB Commodity Index dropped nearly -3% amid a sharp decline in crude oil and natural gas.

There were no relevant high-frequency datea releases with respect to the cyclical inflation story. Next week, however, we’ll likely see a continued acceleration in both Import Price Inflation trends (Tues) and Producer Price Inflation (Wed) trends.

With respect to the structural inflationary pressures building up across the US economy, two data points should contribute to rising fears of accelerated wage growth among investors:

- According to the Dice‐DFH Vacancy Duration Measure, the average duration of a US job opening is 25.1 days, which is up 64% since JUL 2009 and exceeds all prior peaks.

- Within the NFIB Small Business Optimism Index, the “Job Openings Hard To Fill” sub-index ticked up +2pts MoM in JUN to a net 26% of respondents in favor of the question as worded. That’s a new cycle high and the highest reading since JUN ’07.

As such, we believe investors should remain long of the iShares TIPS Bond ETF (TIP) as a way to profit from what we continue to see as a forecasting no-brainer: accelerating rates of reported inflation over the intermediate term.

* * * * * * *

Click on each title below to unlock the content.

Qualcomm: Fair Value $95 for QCOM

Hedgeye Semiconductors analyst Craig Berger likes Qualcomm. He explains why he thinks shares have room to run in this recent research report.

Fund Flows: Negative Inflection In US Fund Flows, Bonds Keep Chugging

The latest survey of mutual fund trends relayed the biggest weekly outflow in U.S. stock funds in 79 weeks -- since the first week of 2013. Our Financials team takes a look inside the numbers.

LISTEN: Keith McCullough's Morning Macro Call 7.11.14

Hedgeye CEO Keith McCullough takes a deep dive into the markets in Friday morning's institutional morning call with a close look at volatility, the Russell 2000 and much more.