TODAY’S S&P 500 SET-UP – July 11, 2014

As we look at today's setup for the S&P 500, the range is 32 points or 0.59% downside to 1953 and 1.03% upside to 1985.

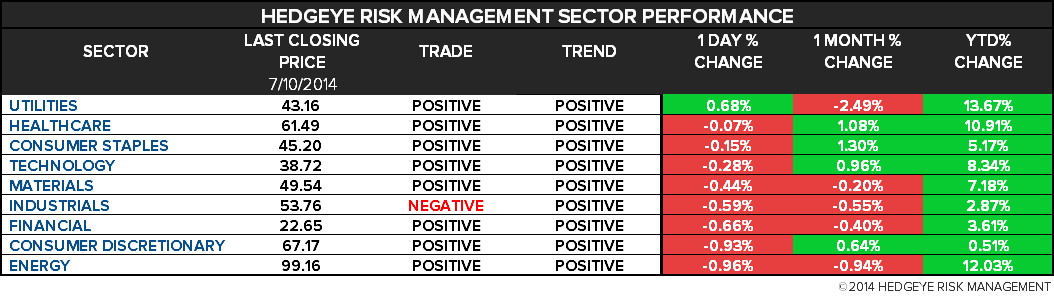

SECTOR PERFORMANCE

EQUITY SENTIMENT:

CREDIT/ECONOMIC MARKET LOOK:

- YIELD CURVE: 2.08 from 2.08

- VIX closed at 12.59 1 day percent change of 8.07%

MACRO DATA POINTS (Bloomberg Estimates):

- 1pm: Baker Hughes rig count

- 2:00pm: Monthly Budget Stmt, June, est. $79.0b

GOVERNMENT:

- House will vote on H.R. 4718, legislation to make bonus depreciation permanent; White House said it would veto the bill

- Commerce Dept releases final decision on anti-dumping, countervailing duties on oil country tubular goods from 9 countries including Korea

- U.S. ELECTION WRAP: Poll Accuracy; Attack Ads; Fundraising

WHAT TO WATCH:

- Reynolds said near deal to buy Lorillard with BAT blessing

- Whirlpool to buy $1b Indesit stake in European expansion

- AbbVie said to nudge top Shire investors to urge deal talks

- Farnborough air show to focus on existing models

- Espirito Santo discloses EU1.2b exposure to GES

- Alibaba nears SEC assent as biggest IPO causes few U.S. ripples

- Gap falls after posting unexpected drop in June comp sales

- Caesars said to tap Kirkland & Ellis to lead restructuring talks

- Nowotny says no ECB action needed now as stimulus takes hold

- Oil demand seen by IEA rising fastest since ’10 on China growth

- July WASDE for corn, soybean, cotton, wheat released at noon

- SoundCloud music service said to near deals with record labels

- Apple bid for Samsung U.S. sales ban pitched as more modest

- China, U.S. highlight steps on yuan, investment pact post talks

- VW outsells GM in China to remain on track for repeat sales win

- Google to send executives to Europe to discuss privacy: NYT

- German, French business lobbies criticize U.S. bank fines: FAZ

- Yellen Testimony, China GDP, GM, JPMorgan: Wk Ahead July 12-19

EARNINGS:

- Fastenal (FAST) 6:50am, $0.44 - Preview

- Wells Fargo (WFC) 8am, $1.01 - Preview

COMMODITY/GROWTH EXPECTATION (HEADLINES FROM BLOOMBERG)

- CME/Thomson Reuters to Run Replacement for Silver Fix in August

- Grain Prices Seen Falling in OECD-FAO Outlook as Supply Rises

- Palm Oil Imports by India Sliding as Buyers Like Sunflowers

- Milk Output Gain Poised to Spur 5-Year Global Glut: Commodities

- WTI Set for Third Weekly Drop as Supply Risks Ease; Brent Falls

- Sugar Output in India to Rise First Time in Three Years on Yield

- MORE: Shanghai Exchange Copper Inventory Rises to 5-Week High

- Record U.S. Soybean Crop Spurs Storage Crunch as Prices Drop

- Tin Losing to Nickel as Indonesia Calls Shots: Chart of the Day

- Prepare for Oil to Keep Falling on Libya to U.S. Supply: Energy

- Gold Heads for Longest Weekly Rally Since March on Haven Demand

- Rapeseed Prices Seen Extending Decline on Ample European Supply

- Gold Traders Resume Bullish Outlook as Haven Demand Increases

- Pollution Permits to Gain 28% as EU Cuts Glut: Carbon & Climate

CURRENCIES

GLOBAL PERFORMANCE

EUROPEAN MARKETS

ASIAN MARKETS

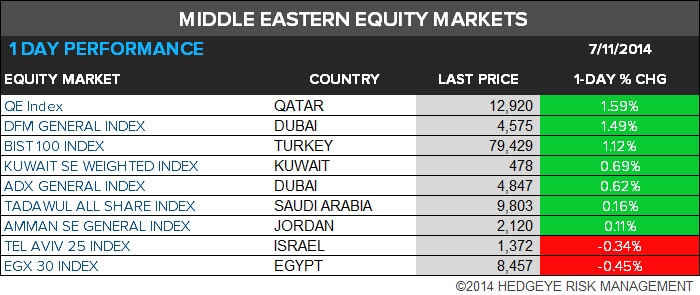

MIDDLE EAST

The Hedgeye Macro Team