This note was originally published at 8am on June 26, 2014 for Hedgeye subscribers.

“Creativity is allowing yourself to make mistakes. Art is knowing which ones to keep.”

-Scott Adams

As you may already know, Scott Adams is the creator of the cartoon "Dilbert." The cartoon makes light of the corporate world and was originally created in the early 1990's as Adams was being "downsized" from a major corporation. Even though Adams isn’t a professional investor like most of you reading this, his quote above is remains rather apropos to the investing world.

Most great portfolio managers and analysts are also incredibly creative. They are creative in the types of analysis they employ and they are creative in their questions for management. But perhaps most importantly, they are creative in idea selection. The true skill, of course, then comes in knowing which creative ideas to keep. Some call this risk management.

We hired a cartoonist recently here at Hedgeye. Cartoons are a great way to communicate our often contrarian investing ideas and themes. Take for example the cartoon posted below that we included in our 100-page deep dive short call on United Airlines (UAL) earlier this week.

The cartoon emphasizes the craziness (at least from our perspective), of UAL’s accounting policies. Not unlike our short calls on certain stocks in the Master Limited Partnership (MLP) sector, we have a difficult time reconciling the valuation with UAL with its underlying cash flows. That said, we also know, to paraphrase Keynes, that the market can remain irrational longer than many investors can stay solvent.

As it relates to airlines, and specifically UAL, longer term we much prefer Warren Buffet’s maxim on the industry. That is, the best way to become a millionaire is to start a billionaire and buy an airline!

Back to the Global Macro Grind...

Our research team has been busy generating some very contrarian and well researched investment ideas lately. This morning I wanted to highlight a few. (As always, if you want more details on the idea and would like to review the more detailed work, please email sales@hedgeye.com for details on how to subscribe.)

First up on the runway is naturally United Airlines (UAL). The core of thesis per our industrials sector head Jay Van Sciver is as follows:

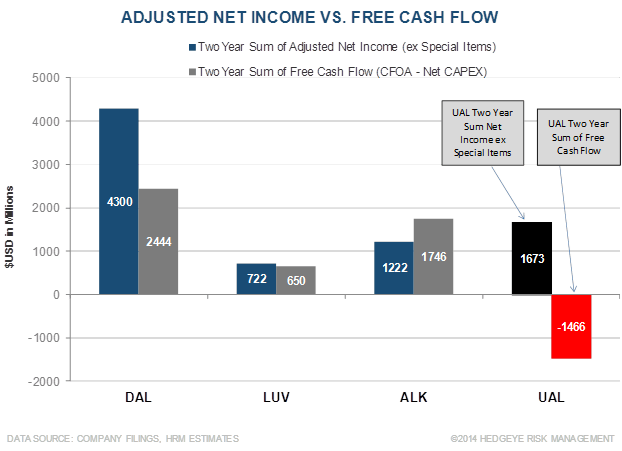

“By our estimates, the underlying UAL operations have generated a cumulative loss over the past two years. Further, UAL has burned over $1.4 billion in free cash flow, defined as Cash Flows from Operating Activities - Net Capital Expenditures, in the last two calendar years. As the high cost U.S. major since AMR's bankruptcy-related cost cuts, we expect UAL to struggle to improve its operations relative to competitors. In our view, it is relative costs that matter. We expect UAL to continue to underperform lower cost airlines.

This is just the tip of the proverbial iceberg.”

In our Chart of the Day below, we highlight this free cash flow deficit versus its peer group. As the chart shows, UAL appears to have severely disadvantaged economics as compared to its peers.

The second idea I wanted to highlight is Lululemon (LULU), a contrarian long idea. For many a thoughtful short seller, LULU has been one of the better short plays in retail of late. Rightfully so. Management appears to be making one misstep after another and doing virtually everything in its power to ruin what is actually a solid brand and product. The core of our long thesis according to our Retail sector head Brian McGough is as follows:

“There’s a massive bifurcation between the growth potential at this company, and the lack of a plan to execute on it. If management continues to execute in a sub-par way, we see downside to about $31 (stress testing our model at 10x EBITDA). Not pleasant (18% downside), but not the end of the world from its current price ($37.61). If the company/Board adds the operational depth that is necessary, then the discussion returns to this company doubling or tripling its top line, and realizing $3.00-$4.00 in earnings power. Pick whatever multiple you want, but the stock price on $3.50 in earnings will push it through its all-time high of $82.”

Finally, the last idea (and probably most controversial idea I wanted to highlight) is our short call on YELP. From a stock price perspective, on the short call we’ve been early, but we are getting increasing confidence in our thesis the more work we do. Our Internet sector head Hesham Shabaan actually had a call recently with the chief financial officer of YELP to discuss, which is at the core of our short thesis. This was his takeaway from that call:

“Where we didn’t get a tremendous amount of detail was when we delved into its customer repeat rate, which is how we are backing into its attrition rate. We did spend some time discussing this topic, and while he wouldn’t explicitly verify or refute our attrition thesis, he did say that YELP has never said that they are not losing customers after we delved into its reported numbers.

The question he wouldn’t answer, which is a spin off of its customer repeat rate metric: “How many of your current customers have been generating revenue for YELP for over a year?”

This is the most important question because it drives at the heart of the retention issue we have been highlighting. We estimate that in any given period that the overwhelming majority of YELP’s reported Local Business Accounts are accounts the company has signed within the LTM (meaning YELP is losing the majority of its accounts after the first year).”

Clearly, Hesham didn’t get a lot of clarity on attrition in his discussion.

As always, let us know if you have any questions on these or any other creative investment ideas you may be working on.

Our immediate-term Global Macro Risk Ranges are now:

UST 10yr Yield 2.46-2.64%

SPX 1932-1973

India’s Sensex 24873-25617

VIX 10.61-12.97

USD 80.02-80.47

Gold 1297-1343

Keep your head up and stick on the ice,

Daryl G. Jones

Director of Research