There shouldn’t be much to cheer about this earnings season but the stocks probably reflect lackluster results. We’re not sure decelerating Mass is priced in yet.

THE CALL TO ACTION

Sure, Street estimates have come down but so have the stocks. Thus, the Q2 earnings season doesn’t look like much of a catalyst, positive or negative, for the group. On an individual company basis, LVS looks like it could disappoint, particularly on a hold adjusted basis since Sands China generally played lucky during Q2. MPEL should come in light as well but we would caution would be shorts: a big share buyback announcement could (and should) be in the works. On the positive side, Galaxy looks most interesting to us. In the face of a difficult junket environment, Galaxy seems to have found the special VIP sauce and we project a slight Q2 beat.

But don’t forget about the upcoming mass deceleration…

THE SETUP

Q2 VIP disappointment is well known and mostly reflected in the sell side estimates. The comparison between Hedgeye and the Street is detailed in the chart below. Note also that we’ve included our hold adjusted EBITDA estimates for Q2 as well. Since we mostly know property level hold percentage before the companies report, we adjust our estimates for good/bad hold.

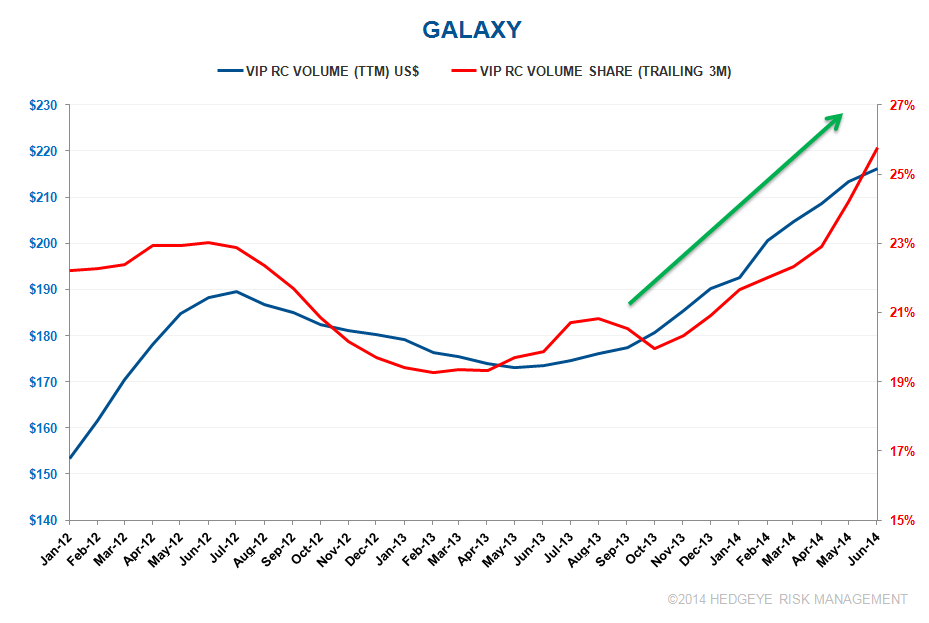

Galaxy: Earnings Beat and VIP Strength

Galaxy looks like the only stock that could pop with earnings (maybe also MPEL if it announces a big buyback). We’ve been very impressed with that company’s performance on the VIP side despite the well-publicized headwinds. As can be seen in the following chart, the company’s portfolio of properties (mostly Starworld and Galaxy Macau) have performed very well on this metric to go along with the market mass strength. While some of the share gain in Q2 could've come from the 2 Wynn VIP rooms facing construction disruption, the trend was already under way.

Mass Deceleration?

The bigger issue is the likely mass deceleration in 2H – not just Q3. We think the 30-40% mass revenue growth enjoyed by the casinos could dissipate to the high teens by the end of the year. As we pointed out in our 06/13/14 note “MACAU: HANDICAPPING MASS DECELERATION” – not only are comparisons difficult but July 2013 marks the month when casinos began jacking up table minimums on the mass floor. Lapping that and keeping 1H Mass growth rates will be a challenge.

CONCLUSION

The trade set up for Q2 earnings doesn’t look as it has in prior quarters. However, over the intermediate term, we remain negative on the stocks overall. We’re not sure sentiment has fully captured decelerating mass growth.