BOBE remains on the Hedgeye Best Ideas list as a long.

Takeaway

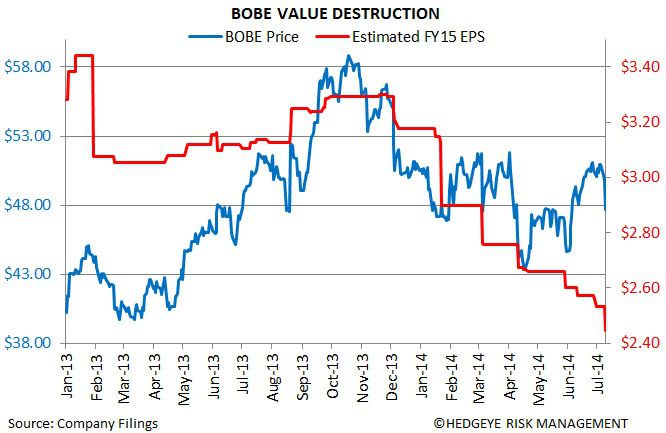

It was a disastrous quarter, and year, for Bob Evans Farms and its management team. The reality is we don’t like the company for what it is, but rather for what it could be. Activist investor Sandell Asset Management has been working tirelessly to unlock this hidden value. If BOBE reports another quarter similar to the one it just did, we won’t have to wait much longer. Management consistently referred to the company’s FY14 performance as an aberration and gave an optimistic outlook for FY15 – too optimistic, in our view. But we think the street will see right through this and estimates will come in below guidance. This company is a mess and first quarter trends are uninspiring. But sometimes ugly can be beautiful. We believe it’s only a matter of time before Sandell gets their way. You can review our full bullish thesis here.

Limping out of 4QF14

4QF14 revenues and EPS declined -17% and 32%, respectively, on a year-over-year basis. Management rattled off a long list of excuses for the poor performance during this morning’s call including severe winter weather, plant startup inefficiencies, high sausage material (sow and trim) costs, unforeseen supplier issues, an ongoing proxy contest and efforts to strengthen internal controls. FY14 and 4QF14 same-store sales decreased -2.1% and -4.1%, respectively. Management attributed 3.4% of the 4Q same-store sales underperformance to severe winter weather. Adjusted, this implies that same-store sales were only down -0.7% in the quarter. We have a difficult time giving credence to this, considering that same-store sales were down -2.7% in April. Mind you, this is with pleasant weather and a refreshed asset base!

FY15 Guidance

Management brought down FY15 EPS guidance from $2.80-3.00 to $1.90-2.20 and guided to a full-year SSS gain of +1.5-2.5%. Most notably, this SSS guidance assumes a negative comp in 1Q, a flattish comp in 2Q and a high-single digit comp in both 3Q and 4Q. Following a disastrous FY14 and a slow start to FY15, we believe this guidance is outlandish. When pressed on this issue during the call, management cited a renovated store base, the Broasted Chicken rollout, an expectation for improved weather, increased marketing spend (including the “Get in on Something Good” advertising campaign) and stronger executional focus as the key same-store sales drivers. While these may be feasible SSS drivers on the margin, this company will not drive high-single digit increase in 2HF15. We simply don’t see how they will get there.

Management guided to eight new restaurant openings in FY15 and has finalized deals for four new Bob Evans Express units (two airport locations, two mall locations). They also expect to license up to ten Bob Evans Express locations during the fiscal year.

Words of Caution

Despite the aggressive guidance, management listed a number of current impediments to the company’s operations including macroeconomic headwinds, health care costs, a struggling core (lower and middle income consumers) market, commodity cost pressures and an increasingly competitive environment.

Commentary on Recent M&A Activity

Management was specifically asked about the high multiples currently being awarded in the packaged foods business. In fact, one investor pressed management on what they’d do if they received a HSH-like multiple for BEF Foods. Alas, management steered clear of that question. They did, however, reinforce their commitment to the foods business noting that an aberrative 2014 is behind them. On that front, they pointed to transformational investments (which have resulted in a lower cost structure), brand synergies, their insourcing strategy and their desire to continue to grow the business as reasons to hold on to BEF Foods. To be fair, they did note that if they received an offer for the foods business they’d look at it, but the overwhelming sense from day one is that management has no intention of selling this segment. Sandell appears adamant on making this happen and we think shareholders should be too.

Recent Notes

06/13/14 BOBE: Reiterating Best Idea Long

05/27/14 BOBE: M&A Activity Heating Up In The Food Business

05/15/14 BOBE: Asset-Light Is Right

05/02/14 New Best Idea: Long BOBE

Call with questions.

Howard Penney

Managing Director

Fred Masotta

Analyst