Our Hedgeye Housing Compendium table (below) aspires to present the state of the housing market in a visually-friendly format that takes about 30 seconds to consume.

*Note - to maintain cross-metric comparability, the purchase applications index shown in the table below represents the monthly average as opposed to the most recent weekly data point.

Today's Focus: MBA Mortgage Applications

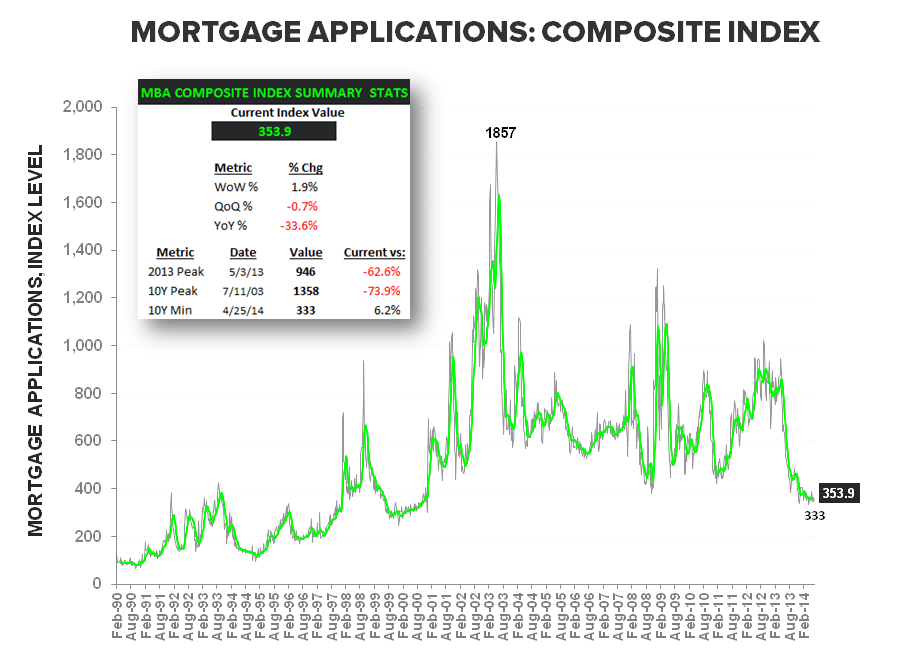

The Mortgage Bankers Association today released its weekly mortgage applications survey data for the week ended July 4.

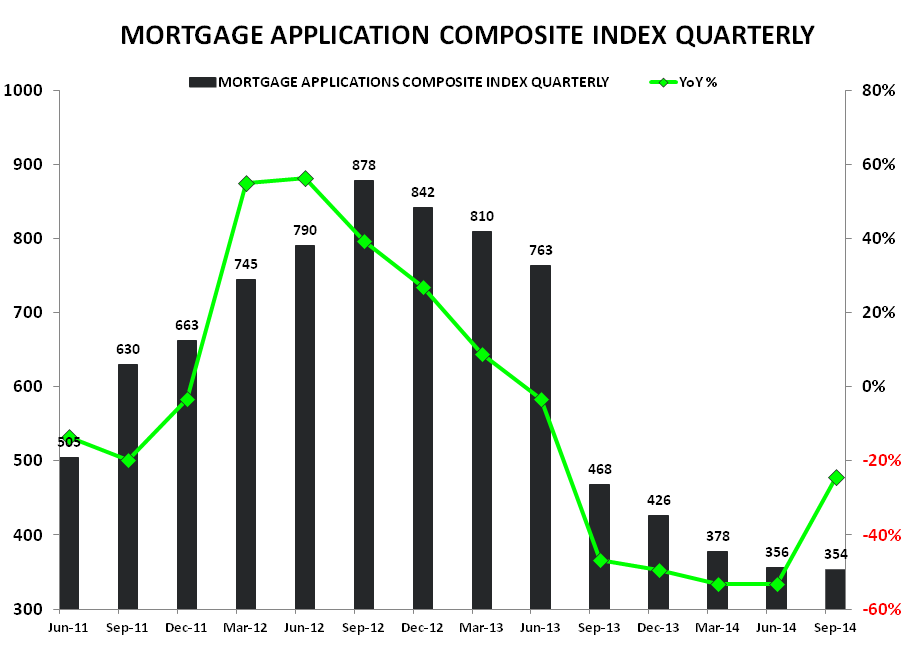

The data reflected a modest Increase to start 3Q with a +3.7% WoW increase in Purchase Apps and a +0.4% increase in Refi’s driving a +1.2% increase in the Composite Index

While we still aren't seeing any meaningful signs of a positive inflection in demand, moving forward, it's probable we see continued improvement from a rate of change perspective (YoY will improve even if purchase index level stays static) as comps ease through 2H.

Here's a summary look at the data:

* Composite Index: +1.2% sequentially and the first positive week in the last four.

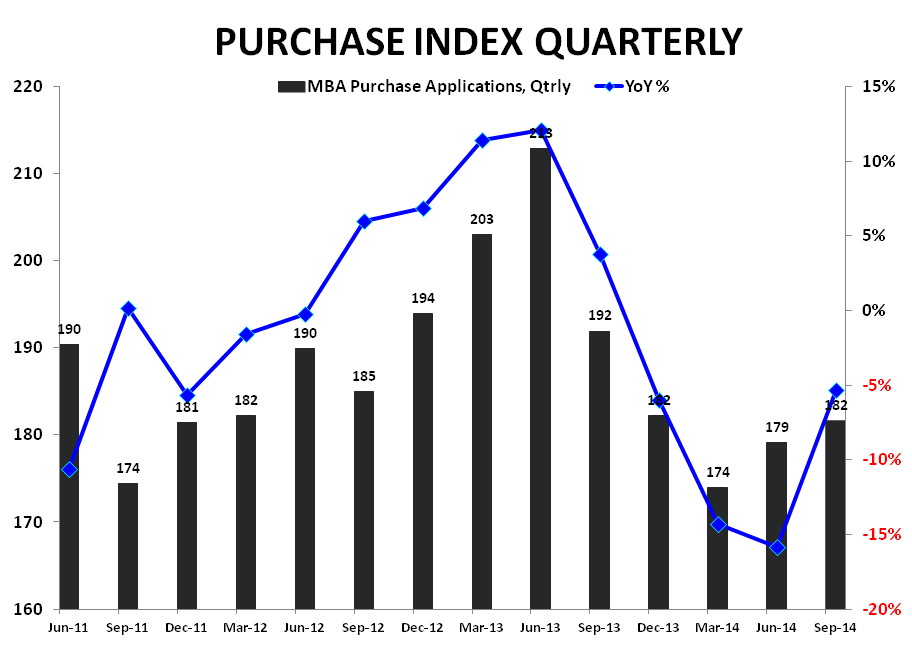

* Purchase Apps: First increase in 4 weeks with purchase demand +3.7% WoW, taking the Index back above the 180 level (181.7). YoY improves to -9.9% from -15.9% prior as we continue move past peak 2013 comps.

* Refi: Up +0.38% sequentially with the YoY improving to -45.9% from -48.5 prior with rates holding just above their best levels of the TTM.

* 30Y Rates: Tick up +4bps WoW to 4.32% but holding near the best levels of the last year. The latest week marks the 3rd consecutive week 30Y FRM rates are down on a YoY basis.

About MBA Mortgage Applications:

The Mortgage Bankers’ Association’s mortgage applications index covers more than 75% of mortgage applications originated through retail and consumer direct channels. It does not include loans delivered through wholesale broker and correspondent channels. The MBA mortgage purchase applications index is considered a leading indicator of single-family home sales and construction. Moreover, it is the only housing index that is released on a weekly basis.

Frequency:

The MBA Purchase Apps index is released every Wednesday morning at 7 am EST.

Joshua Steiner, CFA

Christian B. Drake