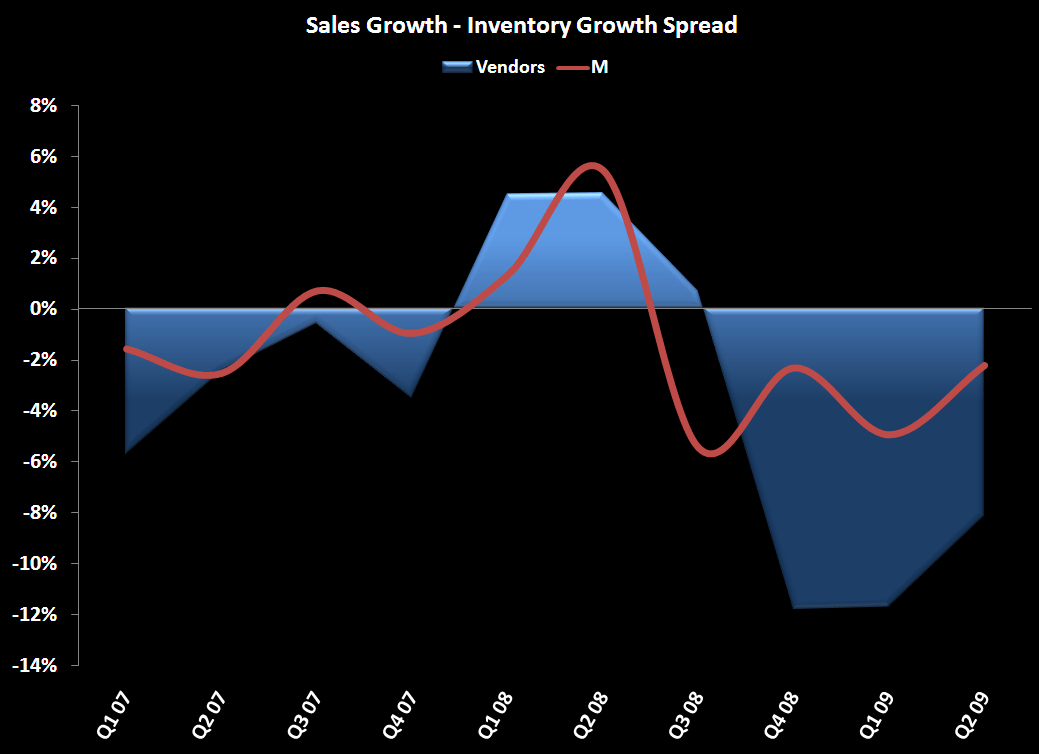

Inventory destocking and clean-up across the supply chain appears to be at an inflection point now that the majority of the branded apparel and footwear vendors have reported 2Q results. The chart below shows branded apparel and footwear sales to inventory spreads over the past several quarters vs. the trend at Macy’s (one of the largest sellers of all these goods). Yes we know that most vendors have become less and less reliant on the department store channel, but with the dominance of Macy’s market-share in branded retailing, it’s still worth a look. We’ll have a better picture of this over the next week or two when every other retailer reports 2Q inventories, but for now it is clear that the delta on sales/inventory is getting better on the margin.

The bottom line here appears to be that this is good for most links in the supply chain. But we can’t improve this delta (hence boosting Gross Margin) by simply shrinking inventories forever. At some point, companies are going to have to actually buy inventory if they care to grow their respective businesses. This actually smells a little like Wall Street to me, where many people are not ALLOWED to be bullish because they (or their PMs) are too afraid of being run over making a positive bet on a consumer discretionary company. At some point, retailers are going to have to start to open the gates. My sense is that this will be around Holiday. That’s also the time when we eye a period (Spring) where the delta on compares won’t be as easy, and companies will need to either benefit from, or suffer with, the capital deployment decisions made today.

Bottom line is that I still think that the Quality Trade returns in early 2010, and companies that are proactively preparing to grow their businesses for the New Reality will prove that today’s numbers are far too low (RL, BBBY, UA, and even Nike later in the year). PSS is in there – though I accept that it does not deserve the ‘quality’ label. Junk is as junk does. That’s WRC, GIL, and JNY. And yes, include ROST and TJX in there. I know everyone loves them and they’re not ‘junky,' but we’ll start to see quality of earnings and incremental ROIC head in that direction next year.