TODAY’S S&P 500 SET-UP – July 7, 2014

As we look at today's setup for the S&P 500, the range is 43 points or 1.99% downside to 1946 and 0.18% upside to 1989.

SECTOR PERFORMANCE

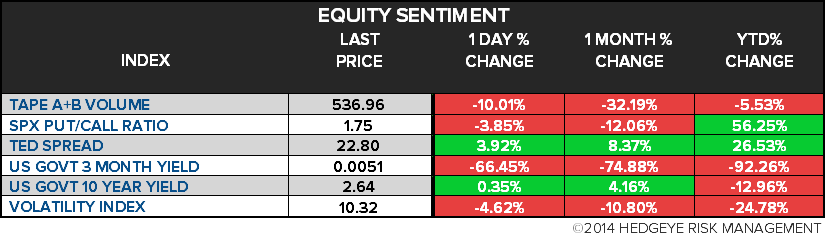

EQUITY SENTIMENT:

CREDIT/ECONOMIC MARKET LOOK:

- YIELD CURVE: 2.12 from 2.13

- VIX closed at 10.32 1 day percent change of -4.62%

MACRO DATA POINTS (Bloomberg Estimates):

- No major economic reports expected

- U.S. Rates Weekly Agenda

- FX Weekly Agenda

GOVERNMENT:

- President Obama hosts teachers at White House to discuss efforts to improve teacher quality

- Iran, World Powers hold nuclear talks in Vienna

- Argentina delegation in NYC to meet with court-appointed mediator

WHAT TO WATCH:

- Archer Daniels Midland to acquire Wild Flavors for $3b

- American Apparel investor said to weigh paying $10m loan

- Lagarde hints at global forecast cut even as U.S. rebounds

- Fed seen raising main rate earlier after June employment surge

- Goldman Sachs brings forward rate forecast as Treasuries drop

- American Express “take it or leave it” policy goes on trial

- SABMiller to sell $1.09b Tsogo Sun stake following review

- SunTrust agrees to pay up to $320m to end mortgage probe

- Apache said to seek buyer for Wheatstone LNG project holdings

- Aristocrat to buy Video Gaming Technologies for $1.3b

- Anglo to sell 50% in Lafarge Tarmac for minimum of GBP885m

- China auto sales rise 14% as foreign brands target small cities

- German industrial output falls as confidence in recovery wanes

- Noyer says BNP case may encourage diversification from dollar

EARNINGS:

- Alimentation Couche Tard (ATD/B CN) 8:42am, $0.25 - Preview

- Bankers Petroleum (BNK CN) 7am, $0.09

COMMODITY/GROWTH EXPECTATION (HEADLINES FROM BLOOMBERG)

- Coffee Stockpiles With Vietnam Farmers Declining to Two-Year Low

- Palm Oil Inventories in Malaysia Extend Climb as Output Expands

- Corn Avalanche Coming as Rain Trumps Planting Drop: Commodities

- Philippines to Consider More Rice Imports, Ending Subsidy

- Rubber Closes Nears 3-Week Low as Oil Price Drop Reduces Appeal

- Brent Oil Falls to Three-Week Low on Libya Supply; WTI Slips

- Gold Extends Retreat From Three-Month High as Dollar Strengthens

- Indonesia’s Presidential Candidates Trade Barbs on Graft

- Copper Drops as Stockpiles Swell Most Since March on South Korea

- Cars Beating Homes Shifts Steel Use in China: Chart of the Day

- Commodity ETP Outflows Seen by Blackrock at $392mln in June

- Philippines to Consider Ending Rice Farmers’ Subsidy: Pangilinan

- Apache Said to Seek Buyer for Wheatstone LNG Project Stake

- Russia Oil Exports Fall to Six-Year Low as Refiners Process More

CURRENCIES

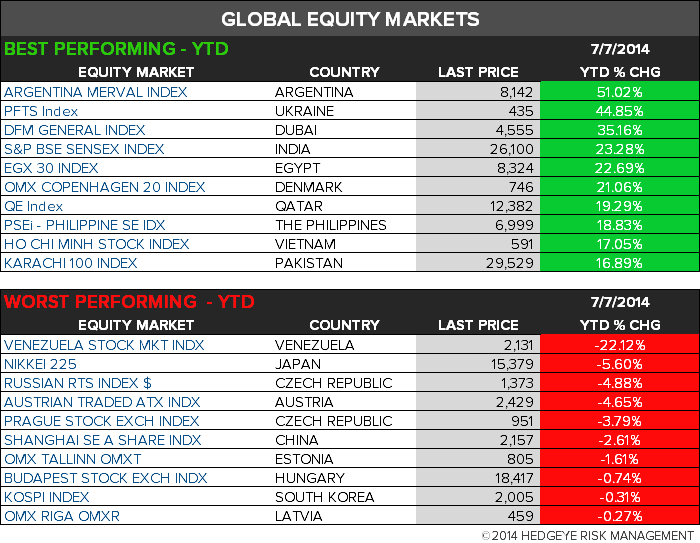

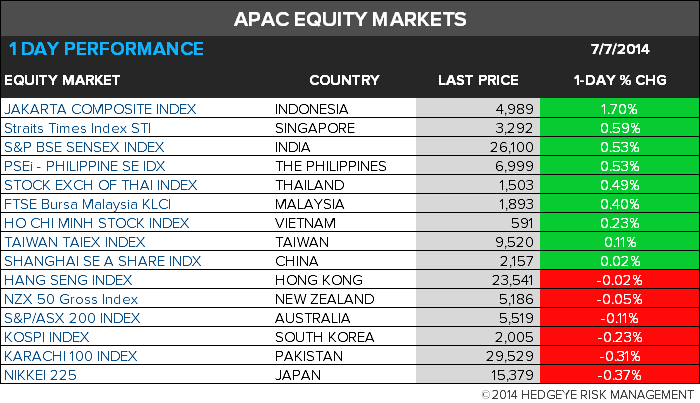

GLOBAL PERFORMANCE

EUROPEAN MARKETS

ASIAN MARKETS

MIDDLE EAST

The Hedgeye Macro Team