Editor's note: This is a complimentary research insight from Hedgeye macro analyst Christian Drake. Click here for more information on our products and services.

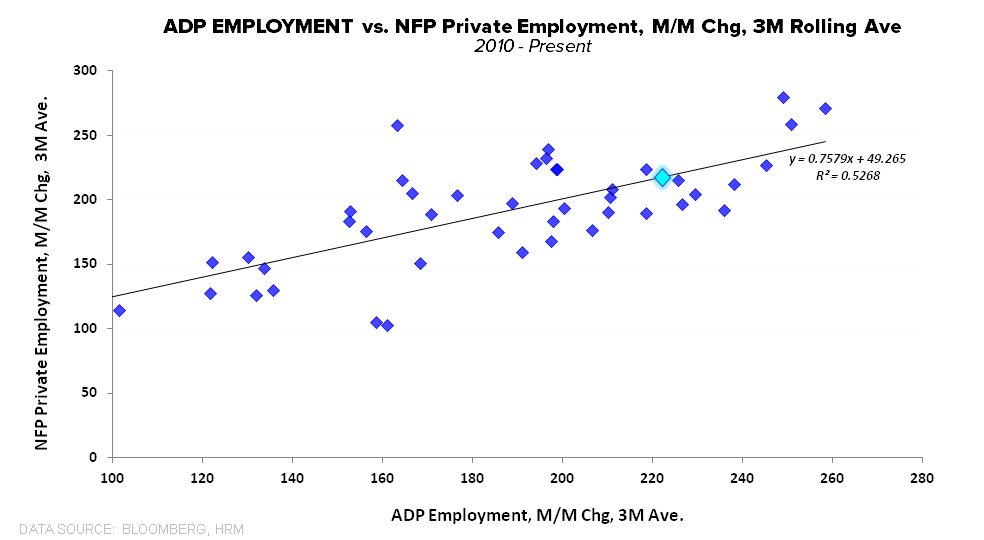

On a month-to-month basis, the payroll estimates from ADP and the Bureau of Labor Statistics can differ substantially. However, on a multi-month, moving average basis, the relationship between the ADP & Non-farm private payroll (NFP) figures is pretty decent.

This is more analytic musing than convicted forecasting, but for the co-integration tea leafers…..the regression using the 3M rolling average in the ADP series (updated for this morning’s data) suggests +217,000 on the June NFP Private payroll print (current estimate = 213,000)

Historically, it appears the tendency is for NFP to re-couple to ADP after outlier moves (counting actual payrolls may be more accurate than calling up some smaller cross-section and asking questions….whoulda thunk).

More to be revealed tomorrow morning...