As we begin Q3 it’s worth digesting the status of Big Tobacco and where we think it is heading. What’s the outlook on pricing and volume trends, is the industry ripe for consolidation, and what did PM say at its Investor Day that may impact the stock and the group? July also kicks off earnings season for the group.

INVESTMENT IDEAS

The table below lists our current investment ideas as well as a list of potential ideas we are in the process of evaluating (watch list). We intend to update this table regularly and will provide detail on any material changes.

Q2 2014 EARNINGS CALENDAR

7/18/14 PM

7/23/14 MO

7/24/14 RAI

7/25/14 LO

HEDGEYE TOBACCO INDUSTRY EVENTS

TODAY, July 2 - VMR Products – E-cig/E-vapor call with CEO Jan Verleur at 2pm EST

July 16 - Ballantyne Brands – E-cig/E-vapor call with CEO John Wiesehan Jr. at 11am EST

Sky-high Valuation. As the charts below show, the subsector is heavily overvalue on a historic basis (P/E at 16.5x versus a 5YR average of 13.1x) with all of Big Tobacco just off their max P/E’s over the period. Valuation is certainly “rich”, however we have a favorite (Long Lorillard) and believe the group will continue to rise alongside consolidation rumors (likely RAI+LO).

Cigarette Volume & Pricing. As we look to the balance of the year, Big Tobacco forecasts U.S. volumes to fall 3-4% this year, similar to 2013, and an anomaly compared to a more recent historical trend of ~ -1 to -2% declines. PM stated that it sees volume (ex-China) falling -2 to -3% this year. We expect Big Tobacco to continue to push through pricing, here again our favorite is LO.

E-Cig Volume Trends. U.S. e-cigarette sales fell -6.1%Y/Y in the four weeks ended June 15th, according to IRI. The latest figure marks the second consecutive Y/Y drop (following -2.9% for 5/18/14), and reflects a 5.2% drop in units and 1% lower prices. We view the recent performance as a reflection of a number of factors including increased product and brand offerings, price competitiveness, increased sales of lower margin rechargable kits, and a consumer shift toward e-vapor consumption.

July marks the beginning of national rollout campaigns for Altria’s e-cig brand MarkTen and Reynolds’ VUSE, which is flooding shelves already occupied by Lorillard’s blu and a handful of strong private national manufacturers (including LOGIC, NJOY, Ballantyne Brands). MO and RAI are offering deep discounts and promotion to get their products in the hands of consumers and, along with LO’s blu, are selling kits at lower price/cartomizer. Finally, we’re seeing signs of consumers shift consumption toward e-vapor products (such as tanks, pens, mods), or a form that’s unlike Big Tobacco’s more cig-alike e-cig offerings. This cohort is not included in measured channels, most often purchased in vape shops, and consumer preference seems driven on e-vapor’s better experience (drag and flavor offerings) and cheaper price versus more traditional e-cigs. We’re conducting survey work on these issues and will be interested to present our findings.

Despite an increasing competitive environment, we expect advances in Big Tobacco’s e-cig technology with the roll-out of new kits will help propel the industry in the back half and ease recent sales declines.

LONG LO. Our long positioning on Lorillard hasn’t changed since we added it as a Best Idea on 2/26/14. What has changed since then is the addition of a rumor mill that RAI may buy the company – we’re riding LO stock alongside these rumor winds. The most recent news that Imperial Tobacco may be shopping RAI’s menthol portfolio is yet another piece of news that should fill LO’s sails. (our note).

What are the main anti-trust hurdles in an RAI-LO deal getting done?

- A combined RAI + LO would own ~ 67% of U.S. menthol market.

- A combined deal would rank as the biggest-ever tobacco merger. Big tobacco is already a highly concentrated industry in the U.S. across the big three – MO has a leading ~51% of market share; a combined RAI + LO would equate to ~ 42% share.

We suspect RAI may be looking to sell its menthol brands like Kool, Winston and Salem, which equates to around ~5% total market share, however we do not think LO will be imminently purchased and are staying long of the stock until an announcement of an agreement or its long-term fair value of $80/share, whatever comes first.

In the box directly below we break out our 5 year EPS estimates for the base business and blu. As we show, the combined business, gets a substantial lift in earnings power from blu (currently the e-cig market share leader at 39.2%), boosting overall CAGR to 20%. In the sensitivity analysis box we offer that even under a punitive scenario in which a 10% discount rate is applied on 5yr forward earnings of $7.50, the stock is north of $80. Given yesterday’s closing price of $61.11, that’s 31% upside in the stock from here.

Below we take a look at the top 10 global tobacco companies by revenue, as a reference for the industry’s biggest players as rumors of further consolidation pang the industry.

PM Investor Day Highlights:

Intermediate Term Struggles Persist; Non-Combustible Investment Significant & Bullish. We are getting constructive on PM over the longer term, especially given its recent move (-8% off its year-to-date high on 6/19). More to follow.

We’re very encouraged by PM’s longer term outlook based on its strong international brand equity, increased R&D spend towards future growth in Reduced Risk Products (RRPs), ability to take price (which it expects to remain in-line with its historical average of $1.8B per year), and easier comps after two years of excessive (above historical norm) excise tax hikes in key geographies (like Australia, Philippines, Japan, Russia, Spain, Italy, France that’s encouraging illicit trade), unique competitive challenges (Philippines and Australia), and macroeconomic weakness, all of which has led to extraordinary volume declines of -3% to -4% per year.

The company did lower its EPS target for 2014 (to $4.87-$4.97 versus previous guidance in May of $5.09-$5.19) to better reflect these intermediate term challenges, however we’re encouraged by its R&D spend (some $2 billion and hiring 300+ scientists since its spin) and focus to lead the RRP category, which we see as a natural progression to declining global cigarette trends: RRP can offset combustible cigarette declines and grow new product demand, a winning long-term strategy in our view.

The company also announced the acquisition of Nicocigs Limited (“Nicocigs”), a U.K.-based e-vapor company whose principal brand is Nicolites. The terms of the deal were not disclosed, but Nicolites has a 27% share of the U.K. e-vapor market, and the acquisition gives PM instant sales presence and a 40 person sales team on the ground (the current U.K. retail e-vapor market is estimated at approximately $350MM, the second largest behind the U.S.). We believe PM’s global inroads and partnership with MO will aid in quickly accelerating brand share and ultimately loyalty, a key component given the early stage of e-vapor product development and increased competitiveness now that all of Big Tobacco has e-cig/e-vapor products on the market.

Finally, we’re bullish over the longer-term on Marlboro 2.0, the company’s architecture to modernize the brand, and with it expand into new population and smoker segments, catering towards trends of consumers seeking smoother tastes, even within the full-flavor category. We’re positive on the company’s push to trade up consumers to the premium and above premium categories that enjoy higher margins. This we believe PM can carry out its strategy over the longer term, leveraging strong marketing and sales teams across the globe, and leverage the growth in aspirational consumers seeking the strong brand identities of the PM portfolio.

Below are key bullets from the PM Presentations last week (Thursday and Friday):

On Reduced Risk Products

- PM calls the segment the “greatest growth opportunity” to address range of adult smoker preferences

- Invested significantly in R&D behind RRPs (some $2 billion and hired 300+ scientists since its spin)

- Has portfolio of over 500 patents worldwide and 1,000 patents pending

- Platform 1 on track for launch (iQOS and Marlboro HeatSticks) in test cities in Japan and Italy in Q4 2014 with national launch schedule for 2015

- Factory being built in Bologna, Italy is expected to produce 30B units by 2016

- iQOS consists of “precisely controlled electrically-heated tobacco system” that maintains a tobacco temperate below combustion, designed to use with a custom “HeatStick” tobacco stick that is to be Marlboro branded

- iQOS expected to be rolled out across its C-store network

- Platform 2 (heat-not-burn combustible cigarette with cigarette-like look) expect to launch in 2016

- Platform 3 & 4: Nicotine containing e-cigarettes/e-vapor products scheduled to launch in 2H 2016

- According to PM the RRP are expect to negatively impact profits in 2014-2016 (hence the update to its guidance) and tip positively beginning in 2017

- Announced the acquisition of Nicocigs Limited (“Nicocigs”), a U.K.-based e-vapor company whose principal brand is Nicolites, which has a 27% share of the U.K. e-vapor market. The terms of the deal were not disclosed

Regional Commentary

EU:

- Arresting the volume decline: now forecasts volume down 5-6% in 2014 vs previous guidance of -6 to -7%. Expects volume down 5-6% in 2015 and down 4-5% thereafter.

- Marlboro continues to take share, up 38.9% in 1Q 2014 vs 38.5% in 2013, with 84% of the company EU volume concentrated in four brands: Marlboro, L&M, Chesterfield, and Philip Morris

- Strategy to drive growth in premium and above premium segment and take price to offset volume declines

- Expects excise tax should remain rational, and within bounds of recent years range of 3% - 6%

- Reduced Risk Products: great opportunity with test launch of Platform 1 in Q4 2014 in Italy and national expansion in 2015

- Tailwinds: UK untapped market. PM has market share of 38.5% in the EU, but only 7.3% in the UK.

- Headwinds: Losing share in Spain, Italy and France on hike in excise tax and uptick in illicit trade

- says 1 in 10 cigs sold in the EU was illicit last year... working to tackle this problem

Asia:

- Continues to be a growth engine for the company with 7 of the top 10 smoking countries across the globe located in Asia

Near term headwinds

Japan, Philippines, Australia, Indonesia, and Russia offer particular challenges, citing the existing unfavorable excise tax and illicit trade headwinds

- Japan – excise hike from 5% to 8% in April 2014, and another VAT hike expected in October 2015 in the 8-10% range (final word expected near year-end)

- Philippines – the co. struggles with a major competitor in the Mighty Corporation. In 2013, the company only declared half of revenues for tax purposes, and continues to create an uneven playing field

- Australia – after a 12.5% excise tax hike in December 2013, there’s another 12.5% hike scheduled for September 2014. Seeing sharp growth of illicit trade (up to 13.9% after years of decline) alongside hit from plain packaging and competitive price discounting

- Indonesia – PM is the largest player in hand rolled cigarettes, how consumer trends against hand rolled is working against them

- Russia – challenged volumes on higher excise (most recently in January 2014 of 8 Rubles/pack) and smoking ban in bars and restaurants effective June 2014

Longer term Tailwinds

- Philippines – government likely to side with PM with tax stamps expect in July 2014 to better even the playing field (vs Mighty) and drive share gains.

- Indonesia – significant growth opportunity with increased purchasing power and middle class expansion.

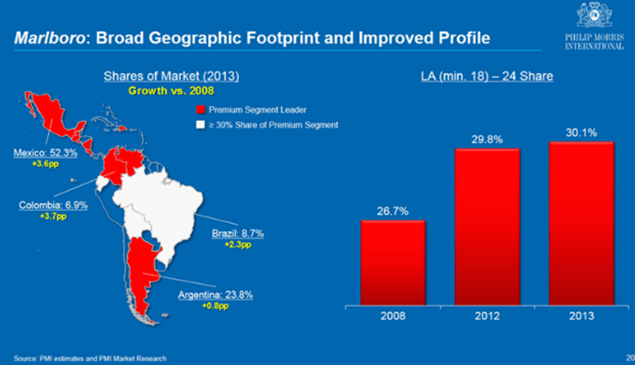

LatinAm & Canada

- In LatAm the compnay has a huge opportunity through its strong brand equity to gain share of more people moving into the middle class, GDP picking up, and by addressing illicit trade with governments throughout the region

- Highlights include better price management in Brazil and Argentina; the co.has a great opportunity to growth the Brazilian market (as the chart below shows, Marlboro has only a 8.7% share in the country), and must work to limit downtrading in Mexico

Happy 4th of July!

Howard Penney

Managing Director

Matt Hedrick

Associate

Fred Masotta

Analyst