“I still eat a burger at a counter with ketchup dripping down my face.”

-Scarlett Johansson

Like being long #InflationAccelerating and slow-growth #YieldChasing in 2014, that sounds #tasty.

My Mom makes yummy burgers on the barbee too. Today we’ll be pounding those back (amongst other things) as we celebrate Canada Day out here on the Big Lake they call Gitchee Gumee in Thunder Bay, Ontario.

Back in Connecticut, it’s going to be Berger Time as well. The Craig Berger, that is – our long-awaited head of Technology Research @HedgeyeBerger who will be launching his Best Semiconductor Ideas today at 11AM EST (Dial-in: ; Conference Code: 859426#).

Back to the Global Macro Grind…

We surprised some of our Institutional Subscribers when we added Semiconductors (SMH = +16.6% YTD) to the long side of our Global Macro Themes deck in Q2. With Berger on board, we’ll really be able to augment our top-down macro call. It goes something like this:

- As US growth slows (and European + Emerging Market + Asian demand stabilizes/strengthens), we like global instead of local demand

- With the US Federal Reserve fear-mongering disinvestment (0% rates), US capex and inventory growth will continue to disappoint

- With tight inventory and low-capex, obvious ways for companies to grow faster are through A) pricing and B) M&A

Yep, just one more way you can be long a slowing US domestic consumption cycle.

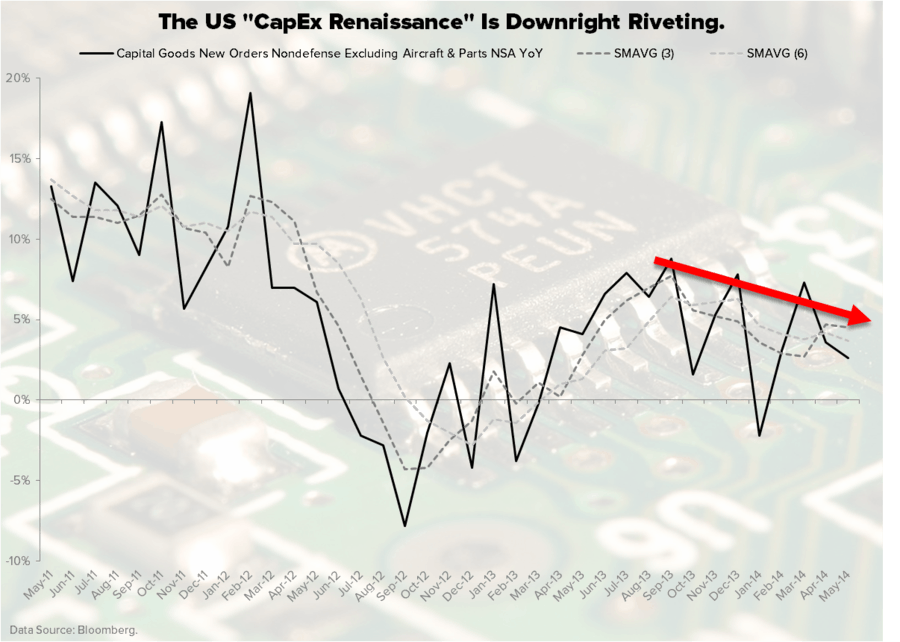

There’s a solid article in the FT today reminding you that those who were bullish on the “US capex cycle” have been direly disappointed in 2014 YTD. Newsflash: you aren’t going to get a real mid-1990s capex cycle until you let interest rates rise.

Ideological central-planners don’t get the career-risk adjusted decision making process of execs inasmuch as their Keynesian textbooks don’t get how a country like the UK can see manufacturing demand accelerate (PMI for June 57.5) as the value of the UK currency does (Pound $1.71 vs USD today).

Why on earth would a public CFO sign off on his or her CEO ramping capex (and hurting peak margins, because that’s what happens in the short-term when you invest) when he or she can just fire people (cut costs), take price, and/or buy someone and do the same all over again?

Back to Berger time…

He and I are going to have some fun together creatively destructing some of the old ways of #OldWall research. You see, our edge isn’t what some of NYC and CT’s finest hedgies went to jail for. It’s working as a team, using a differentiated top-down and bottom-up research process.

If you’re still reading my rants, you probably have a feel for what I do. What Berger does is born partly out of his industry experience (worked at Intel, INTC) and partly from doing his time working for firms that also loved doing banking and brokering (we don’t plan on doing either).

We do un-conflicted, un-compromised, independent research. If we don’t have Research Edge that helps investors generate alpha, we don’t get paid. We’re really looking forward to marrying the top-down signaling process of Global Macro with Craig’s detailed financial models and industry analysis.

Here’s a looksy at slide 10 of Berger’s 52 slide Global Semis deck:

1. Chip Sector now a Dividend + Cash Return Story: Div yield leaders include STM (4.2%), INTC (3.0%), MXIM (3.0%), MCHP (2.9%), ADI (2.7%)

2. Large Dividend Hikes (and/or share buybacks) Possible: from SNDK, QCOM, BRCM, NVDA, MRVL, ALTR, AVGO, POWI, VSH, SWKS

3. Acquisitions in Chip Sector Heating Up: Consolidation trends should continue with CAVM, ISIL, SLAB, POWI, MLNX, AMCC, IPHI, EZCH our top acquisition targets

In other words, if you’re into slow-growth #YieldChasing + M&A, you should still be into semis.

If you’d like to throw some more inflation ketchup on that tasty Hedgeye-Style factored burger, stay with long inflation via my homeland too. Largely a play on commodity #InflationAccelerating, Canadian Stocks (TSX) are +12.9% YTD. Beats banging your head against that Old Wall Dow, doesn’t it?

Our immediate-term Global Macro Risk Ranges are now:

UST 10yr Yield 2.49-2.59%

SPX 1

VIX 10.61-12.79

Pound 1.69-1.71

WTIC Oil 104.76-106.94

Gold 1

Copper 3.13-3.21

Best of luck out there today,

KM

Keith R. McCullough

Chief Executive Officer