This note was originally published at 8am on June 17, 2014 for Hedgeye subscribers.

“The Fundamental Force for Divergence: r > g”

-Thomas Piketty

I’m about a third of the way through Piketty’s 685 page NYT “Best Seller,” Capital In The 21st Century, and I have to admit that I don’t think I’m going to make it to the end. Like most Keynesian and/or Marxist economic diatribes written from a loft in Europe, there’s a lot more text than teeth.

That said, if Piketty had any experience risk managing markets, he’d have been able to hammer home why one of his core arguments is accurate. The aforementioned quote points to a simple relationship between growth (g) and returns (r). It explains the widening divergence between rich and poor.

True or False? “When the rate of return on capital significantly exceeds the growth rate of the economy, then it logically follows that inherited wealth grows faster than output and income” (Piketty, pg 26). True; especially when real growth is 0%. That’s when only those long inflation and/or #YieldChasing get paid.

Back to the Global Macro Grind…

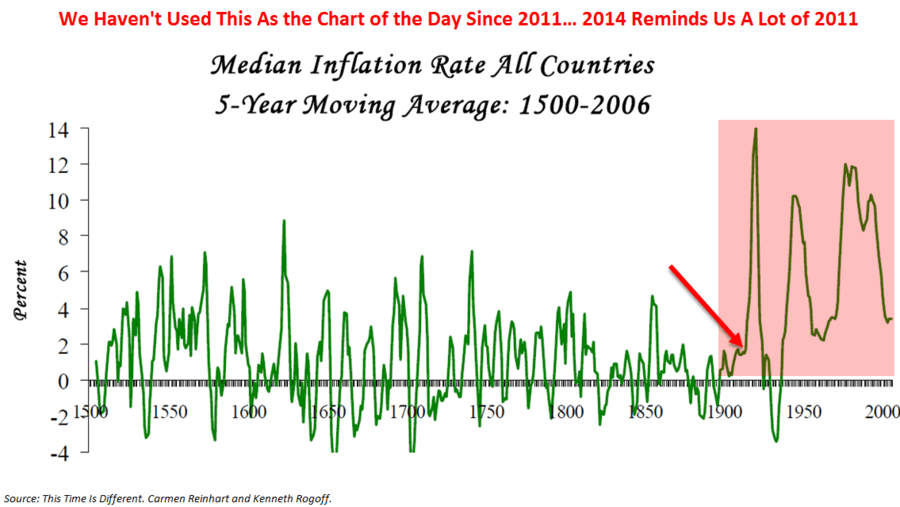

The main issue most mainstream “economists” educated in the West tend to have is taking the government’s word for it on inflation. If you don’t know what real world inflation is, there’s absolutely no way you can have a real forecast for real (inflation adjusted) consumption g (growth).

It took Piketty to page 102 to address “The Question of Inflation”, but using multi-century government data sets he was still able to discern a very basic trend in made-up government inflation data: “the first crucial fact to bear in mind is that inflation is largely a twentieth-century phenomenon.”

“More precisely, if we look at average price increases over the periods 1700-1820 and 1820-1913, we find that inflation was insignificant in France, Britain, the United States, and Germany: at most 0.2-0.3% per year. We even find periods of slightly negative price movements.” (Piketty, pg 103)

Negative price movements?

Oh the horror. Commonly fear mongered in 3-card Keynesian Monte as the great threat of “deflation”, most humans have got along just fine when the prices of primitive things like food and shelter have fallen in price.

Forget getting lost in the weeds on why there’s no way the 0.2-0.3% inflation reading is precise. It’s the forest (i.e. long-term and secular slope of the line in general prices and/or cost of living) that has been straight up into the right since 1913.

What happened in 1913?

Oh, right. That was the Federal Reserve Act of 1913 – when the US allowed an un-elected body of central planners begin with their Policies to Inflate via destruction of the purchasing power of The People (i.e. the value of their hard earned currency and savings).

Back to the relationship between real growth (g) and returns (r):

- If real-growth is +3-4% (1983-1989, or 1993-1999), lots of people are getting paid (savers too!)

- If real growth is 1.7% (Bush and Obama decade), less people are getting paid (not the savers though)

- If real growth is -1% (US GDP growth in Q1 of 2014), people who are long inflation and/or #YieldChasing get paid

If you have nothing, you can’t make a return on nothing. That’s a simple concept. What’s less obvious is that if you have something, and save it (during this Federal Reserve Regime) you still get nothing, minus inflation.

“So”, when growth slows, you’re forced to buy asset price inflation (commodities, REITS, etc.) so that you can earn what you need (something greater than 0%) just to keep up with the cost of living.

When growth accelerates and the central planning agency RAISES rates, you get paid to both save and invest. (hint: you can’t grow unless you have savings to invest, unless you start levering yourself up).

Two real-time examples of countries going opposite way on this right now are the USA and the UK:

- The British Pound is +4.2% in the last 6 months vs the US Dollar

- As the Pound strengthens, UK inflation has weakened to its lowest level since 2009 (+1.5%)

- As US inflation accelerates (vs. decelerating at this time last year when the USD was strengthening), real-growth is slowing

What the US and UK bond markets are expecting are two different policy paths:

- US rates are falling again as the world anticipates Yellen gets less hawkish (less tapering, more dovish)

- UK rates are rising as the world expects the Bank of England to get more hawkish and get off 0%

I could ground myself in an academic hole and write a doctoral thesis on how the divergence between rich and poor is being perpetuated by Fed Policies to Inflate. But I won’t. Too expensive. The inflation of a Western Economics Education is hitting all-time highs too.

Our immediate-term Global Macro Risk Ranges are now:

SPX 1916-1951

RUT 1136-1175

VIX 10.73-13.29

Pound 1.68-1.70

Brent Oil 110.13-113.78

Gold 1259-1286

Best of luck out there today,

KM

Keith R. McCullough

Chief Executive Officer