TODAY’S S&P 500 SET-UP – July 1, 2014

As we look at today's setup for the S&P 500, the range is 29 points or 1.13% downside to 1938 and 0.35% upside to 1967.

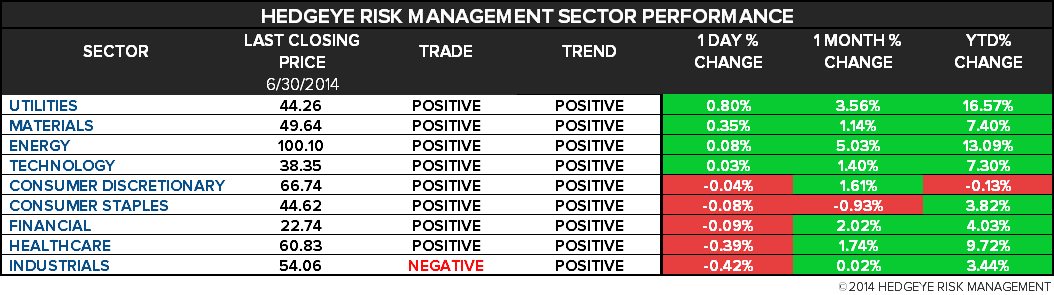

SECTOR PERFORMANCE

EQUITY SENTIMENT:

CREDIT/ECONOMIC MARKET LOOK:

- YIELD CURVE: 2.09 from 2.07

- VIX closed at 11.57 1 day percent change of 2.75%

MACRO DATA POINTS (Bloomberg Estimates)

- 7:45am: ICSC weekly sales

- 8:55am: Redbook weekly sales

- 9:45am: Markit US Manufacturing PMI, June final, est. 57.5 (prior 57.5)

- 10am: ISM Manufacturing, June., est. 55.9 (prior 55.4)

- 10am: Construction Spending m/m, May, est. 0.5% (prior 0.2%)

- 10am: IBD/TIPP Economic Optimism, July, est. 48.0 (prior 47.7)

- 4:30pm: API weekly oil inventories

GOVERNMENT:

- House, Senate on recess until July 8

- President Obama holds cabinet meeting, speaks on economy

- 8:30am: Treasury Sec. Jack Lew speaks at U.S.-China Business Council event ahead of his trip

- *U.S. ELECTION WRAP: McAllister to Seek Re-Election; Obamacare

WHAT TO WATCH:

- U.S. June vehicle sales starting ~8:30am - Preview

- Iraqi lawmakers meet amid rifts on Maliki’s political future

- China June Purchasing Mgrs at 51.0, matching estimates

- BNP agrees to pay $8.97b to End U.S. sanctions probe

- BNP Paribas seen rerouting dollar clearing to retain customers

- Macau casino revenue falls 3.7%, first drop in 5yrs

- Job gains fail to lower U.S. office-vacancy rate stuck at 16.8%

- Global equities may rise 8-9% in 12 months, UBS’s Haefele says

- Russell offers final member lists for Russell 1000, Russell 2000

- U.K. manufacturing unexpectedly strengthens on demand surge

- German joblessness unexpectedly increases for second month

- Poroshenko says Ukraine ends cease fire in Eastern regions

- U.S. foreign account tax compliance act takes effect

EARNINGS:

- A Schulman (SHLM) 4:30pm, $0.66

- Acuity Brands (AYI) 9:15am, $1.12

- Paychex (PAYX) 4:01pm, $0.40

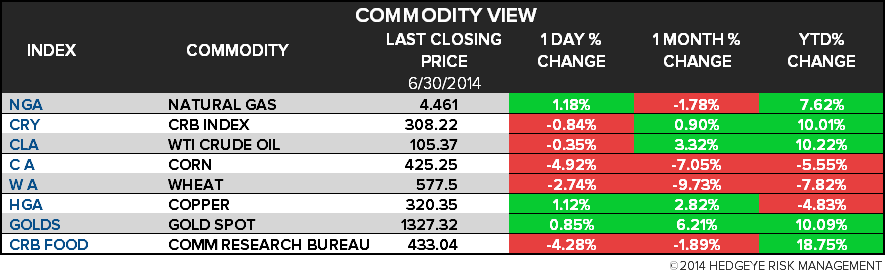

COMMODITY/GROWTH EXPECTATION (HEADLINES FROM BLOOMBERG)

- Iraq’s Kurds Vow to Keep Kirkuk Oil Fields Until Referendum

- Gold Rally Obscures Fund Outflow as Investors Target Shares

- Raw Materials’ Resurgence Follows Record Fund Exit: Commodities

- Zinc Drops From 16-Month High as Rally Is Judged to Be Excessive

- Soybeans Extend Slump on USDA Data as Corn Drops to 5-Month Low

- Cocoa Drops as Supplies From Ivory Coast Increase; Sugar Falls

- Gold Investor Index Falls to 4-Year Low as Rally Spurs Selling

- Steel Rebar Extends Quarterly Slump as China Steel Output Climbs

- Europe’s Seven Months of Warm Weather Set to Finish in July

- South Africa Close to Starting Yellow-Corn Exports to China

- Fuel Oil Shipments to Asia for July Arrival Increase to 3.3M Mt

- Uganda Seen Boosting Sugar Production 32% With New Factories

- Shutdown Threatening to Cost U.S. Ports $2 Billion Spurs Talks

- Gold Trades Near Three-Month High as Holdings to Economy Weighed

CURRENCIES

GLOBAL PERFORMANCE

EUROPEAN MARKETS

ASIAN MARKETS

MIDDLE EAST

The Hedgeye Macro Team