This note was originally published at 8am on June 16, 2014 for Hedgeye subscribers.

“Something deep in my character allows me to take the hits and get on with trying to win.”

-Lionel Messi

First and foremost, happy belated Father’s Day to all the Dads out there who do what they do when no one is looking. As most of the young men playing in the 2014 World Cup will attest, doing the best that you can do out there, every day, is a grind.

For those of you who didn’t know who Messi was until your Dad’s Day dinner last night, what a gem this guy is in the arena that is soccer. Selfless, hard working, and talented, he is everything that the largesse of Argentina’s government is not.

At 26 years old, Messi is the Captain of Argentina’s hopes in Brazil. Like many athletes who represent their country, his maturity and leadership are beyond his years. On money, he said it “doesn’t thrill me or make me a better player… I’m just happy with the ball at my feet.”

Back to the Global Macro Grind…

With both the NHL and NBA seasons officially over (congrats Kings and Spurs!), it’s time for some World Cup Soccer while you attempt to risk manage what are becoming very thinly traded all-time-bubble-highs in US Equities.

In order to look forward, let’s take a step back. Unless you were long #InflationAccelerating last week, it was messy:

- SP500 and Dow were down -0.7% and -0.9%, respectively, last week (Dow barely up YTD at +1.2%)

- Russell 2000 resumed its bearish intermediate-term TREND at -0.1% YTD and -3.8% since March

- Industrials (XLI) led losers at -1.5% on the week as energy prices (producer costs) ripped

US Consumer Discretionary stocks (XLY) are still -1.6% YTD and continue to eat #InflationAccelerating:

- CRB Commodities Index (19 Commodities) was up another +1.5% last week to +10.6% YTD

- WTI Crude Oil led inflation melt-up at +4.2% on the week to +10.8% YTD

- Natural Gas and Coffee prices were up another +1% last wk to +14.8% and +50.6% YTD, respectively

While Total US Equity Market Volume was down -34% (vs. the 3 month average) on Friday’s +0.3% SPX negative breadth up-day, we finally got some real equity and commodity market volatility last week:

- Oil volatility (Oil VIX) was +34.3% last week to 19.47

- US Equity volatility (VIX) was +11.8% last week to 12.18

From a risk management perspective, rate of change in our model always matters – but it really matters when that directional rate of change (2nd derivative) signal occurs off its most asymmetric long-term TAIL risk point.

That’s where US Equity Volatility (VIX) was when it closed at 10.73 on June 6, 2014. While the perma-bulls on US GDP growth may think “it’s different this time”, it’s not. The VIX has never stayed below 10 – ever. And, as you know, never-ever is a very long time.

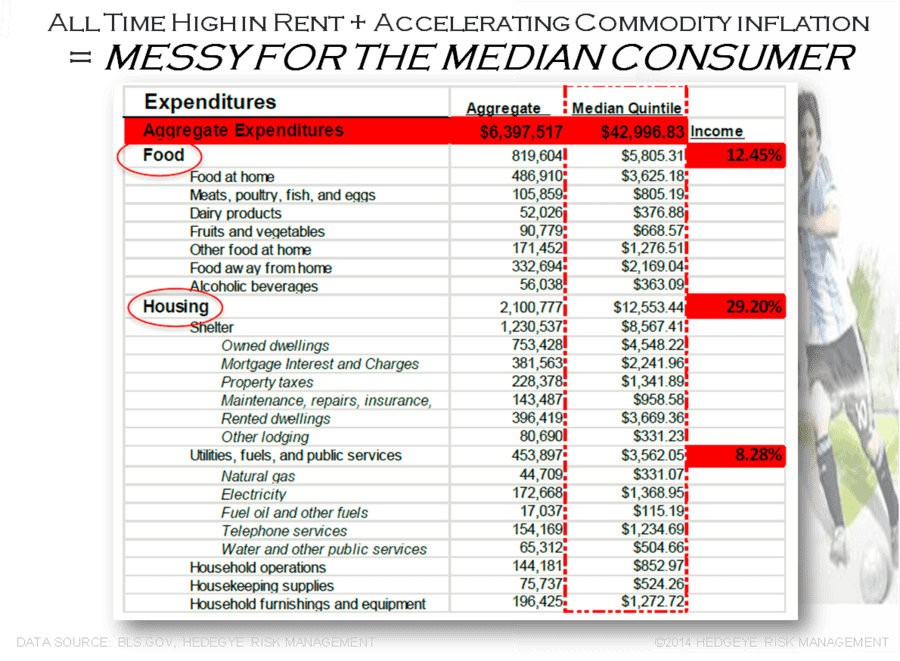

As gas prices rage higher alongside an all-time high in US rents (34% of the country rents and shelter is their #1 cost of living), prepare for another messy week of Consensus Macro expectations meeting their maker (bond market signaling growth is slowing):

- TUESDAY: US Consumer Prices (unlegislated taxes) for May should continue to accelerate

- WEDNESDAY: The Fed should talk down its US Housing and GDP forecasts now that they’re wrong on growth (again)

- THURSDAY: Uruguay plays England at 3PM EST #WorldCup

If England plays like they did against Italy, that could get messy too. As Spain learned against the Dutch, at first risk happens slowly – then all at once.

UST 10yr Yield 2.45-2.64%

SPX 1914-1951

RUT 1124-1175

VIX 10.73-13.21

Brent Oil 109.87-113.11

Natural Gas 4.65-4.83

Gold 1257-1286

Best of luck out there this week,

KM

Keith R. McCullough

Chief Executive Officer