RL: Water Polo

This story is on-track to prove that $6 in EPS power on a disproportionately lower operating asset base is a reality. Mar10 numbers are still low, but for the first time in a year and a half, I can’t model a 40% blow-out in the upcoming Q.

Now that RL has printed yet another bullet-proof quarter, let’s step back and reassess the thesis as well as expectations going forward. I still think that the ultimate call here is that within 12 months, people will begin to eye $6 in earnings power on a disproportionately lower operating asset base. Translation = higher earnings without dumping capital into the model in order to get there. I can’t find many of these stories out there in retail.

But I need to keep myself intellectually honest about duration on this one. Yes, I am still getting to a number for the year that is well ahead of the Street ($4.17 for the Mar10 year vs. Street at $3.70), but for the first time in a year and a half, I’m not modeling meaningful upside to this quarter. I don’t think that RL will miss, but let’s not ignore that this company beat each of the past seven quarters by over 40% on average. I’ve got them beating this one by less than 2%.

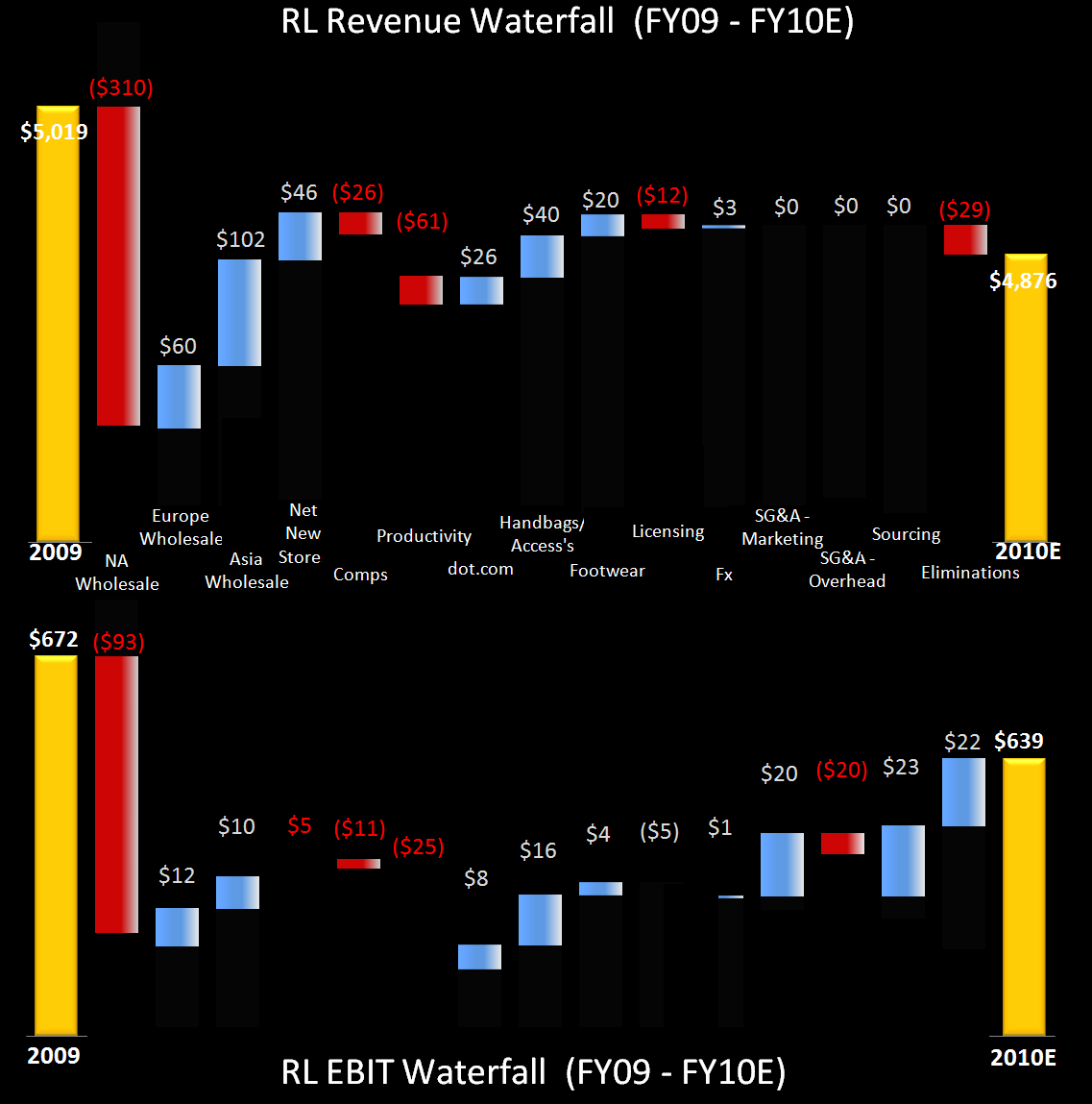

Given all the moving parts in this business and the changes in distribution, product, geography (and the overlap therein), it is increasingly important to model the puts and takes. Here’s an overview as to how we’re coming out with our numbers. Our 2Q10 (Sept) assumptions are outlined in Exhibit 2 below.