Below are Hedgeye analysts' latest updates on our NINE current high-conviction investing ideas and CEO Keith McCullough's updated levels for each.

We also feature two institutional research notes from earlier this week, as well as a brief video presentation from two of our gaming analysts focusing on five stocks in their research universe.

Trade :: Trend :: Tail Process - These are three durations over which we analyze investment ideas and themes. Hedgeye has created a process as a way of characterizing our investment ideas and their risk profiles, to fit the investing strategies and preferences of our subscribers.

- "Trade" is a duration of 3 weeks or less

- "Trend" is a duration of 3 months or more

- "Tail" is a duration of 3 years or less

HEDGEYE CARTOON OF THE WEEK

IDEAS UPDATES

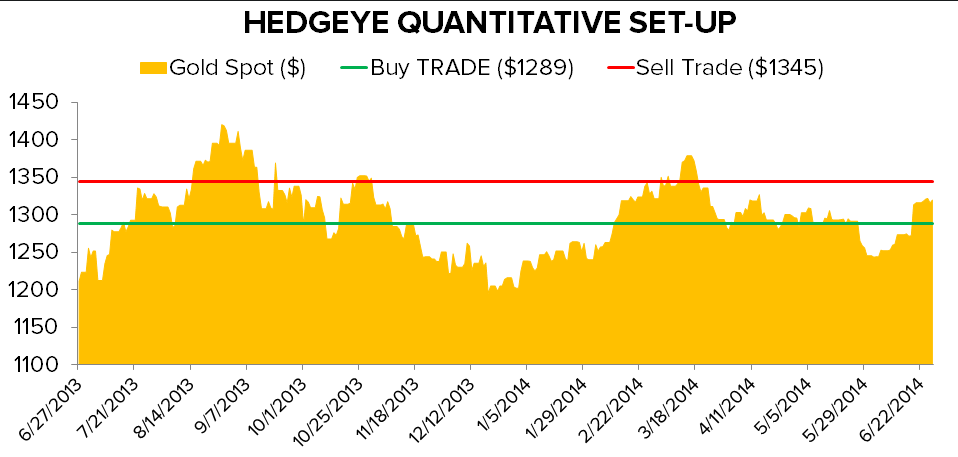

GLD – Despite a slight correction in the CRB Index, Gold still grinded higher (again) on the week.

From our perspective on how high-frequency data points curbing growth and inflation have changed from last week, the revised -2.9% Q1 GDP report likely contributed to divergence against the CRB Index. The Economic Times had a report yesterday about the symmetry between Gold and Brent coming apart, and financial media has published no shortage of arguments on weather, disease, and geopolitical tension attributing to the run-up across the commodity complex.

- Gold: +9.3% YTD

- Brent Crude Oil: +2.3% YTD

- CRB: +11.4% YTD

- CRB Food Index: +23.5% YTD

All weather-related and geopolitical arguments aside, the article from the Economic Times confirms our views on Gold’s footprint. When growth surprises to the downside and a run-up in everyday necessities that people actually consume increases, individuals have less money to spend. Therefore Gold’s breakaway from the broader commodity complex and stronger linkage to the dollar and forward looking monetary policy makes intuitive sense.

- Core CPI (Fed’s preferred measure): +0.3% (+0.2% expected)

- Headline CPI: +0.4% for May (+0.2% expected)

- Fed’s full-year GDP forecast: +2.1-2.3% (revised downward from 3.0%)à pre-revision

Factoring in a -2.9% revision this week (and a likely second downward revision in 2H comps) makes for a more dovish outlook (relative to expectations). In this environment, we continue to like Gold in the intermediate-term on the long-side.

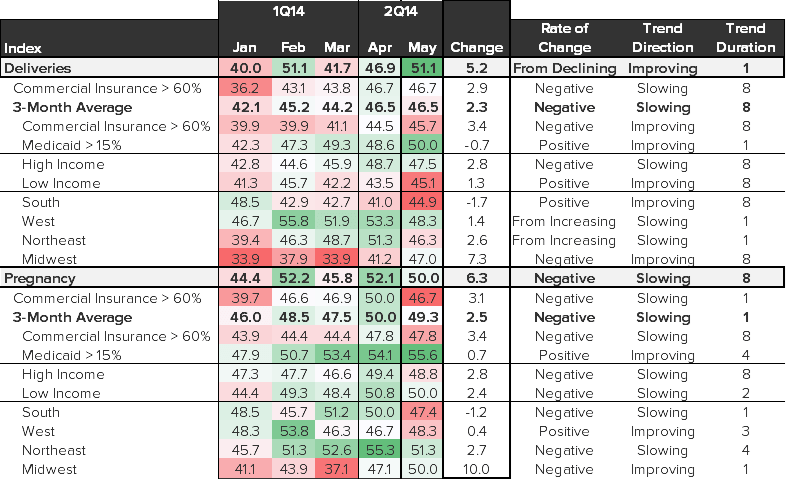

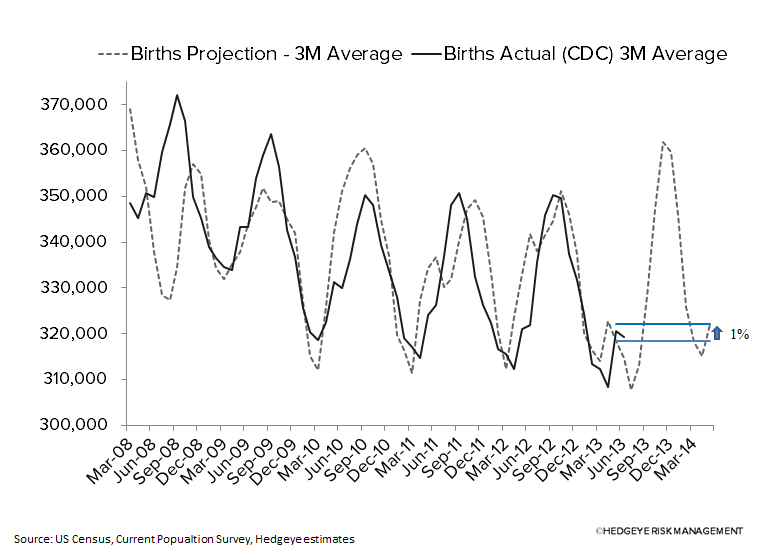

HCA – Our update of our birth model continues to show a decent increase in births through the May 2014 update. The key here (as we have said before) is the link between births and 25% of inpatient admissions. Note: A value over 50 is positive; under 50 is negative.

There are glimmers of hope in our OB/GYN monthly survey as well. Deliveries and Pregnancy trends are picking up in some pockets, particularly in the West and among Medicaid focused practices.

HOLX – A study was released showing the benefits of 3D Tomosynthesis over conventional 2D Digital Mammography this week. Both the New York Times (see NYT story here) and Bloomberg carried stories about the results. The key chart is below and for us, the reason we believe 3D Tomo will receive a higher payment per scan than facilities currently get for a digital mammography.

In the JAMA study, the authors compared results with conventional 2D Digital mammography (open circle) in terms of cancers detected and the number of patients called back for more detailed analysis, to patient exam results when facilities switched to 3D tomosynthesis (blue circle). 3D found more cancer while recalling fewer women for a second more thorough and anxiety producing diagnostic exam.

Our view is that even if CMS posts a preliminary reimbursement rate equivalent to 2D, the reimbursement for tomosynthesis is unlikely to remain at that level. The evidence and the experience of radiologists (who we have spoken to so far) is strong at this point that 3D tomosynthesis is indeed better. By keeping 3D payments low, CMS will create a political problem for themselves where they will be demonized for denying women access to lifesaving technology.

LM – Legg Mason was out in the debt markets this week amending and extending its current credit facilities. The company was able to place various categories of 5, 10, and 30 year funding, replacing some shorter term bank facilities and also a convertible bond issue. The ability to secure longer term funding and replace these lower quality sources of capital (the convert and shorter term bank lines) is a great benefit for shareholders as LM's capital base is now secured for a much longer period of time with higher quality capital.

We continue to estimate, Legg may be shoring up capital to make acquisitions which historically has resulted in a positive reaction for the stock as asset management deals can be accretive to earnings within a short period of time.

LO – Lorillard gave up its 6.5% pop last week, reflecting the roller coaster ride of a stock that is being driven on sentiment (a possible acquisition target of Reynolds American) and a lack of news. We, however, suggest remaining long of the stock.

Our thesis has not changed. While its competitors like Philip Morris are dealing with international headwinds, we remain bullish on LO’s U.S.-based portfolio of premium menthol.

We continue to outline the long-term fair value price of the stock at $80/share. We do not think LO will be imminently purchased and are staying long the stock that we added to Investing Ideas on 3/7/14.

OC – Last week, management guided earnings down on the back of a weak roofing segment. While the announcement was disappointing, we still continue to expect shares to perform well in the longer-term as Owens Corning improves margins in its two other segments that combine for 70% of its sales. News this week is quiet out of the Owens Corning camp as we approach the end of 2Q. We will highlight a couple of quick notes:

- APOG, an architectural glass product company, posted a 47% year-over-year in its 1Q FY2015 profit. The company also expected its revenues to grow between 15% and 20% year-over-year.

- Saint-Gobain, a European building products company that competes with OC in roofing and insulation, reports results for first half of 2014 on July 30.

- McGraw Hill non-residential buildings construction starts fell 5% in May after a 15% increase in April. However, when looking further into the numbers commercial buildings by office and hotels increased by 31% year-over-year an encouraging sign for Owens Corning.

- The Architecture Billings Index (ABI), in the chart below, posted its largest month-over-month increase in 8 months. The ABI index typically leads industry non-residential construction activity by 11 months – another positive for Owens Corning.

OZM – We published a note on Och-Ziff on Friday. Click here to read.

RH – This week Restoration Hardware unveiled its latest Design Gallery, in the Flatiron district in New York City. We would actually call the 22,000 square foot store ‘the mother of all renovations’ more than a completely new store. RH took the existing 9,000 square foot store and added 13,000 feet to make it a temporary flagship. We say ‘temporary’ because RH is in the process of securing the location for its true NYC flagship, which we think will rival the Ralph Lauren mansion in allure.

The lease on the Flatiron store only takes RH out another two years. But given that this is the most profitable location in the entire fleet, the economics made sense to build the extension for just another 24 months. One notable point, when a store gets remodeled, it gets pulled out of the ‘comp’ equation until it is open for 14 months. This could have a slight negative impact on the RH reported comp (maybe a point or two), but will be accretive to earnings immediately. That’s what we care about most.

TIP – Hedgeye's macro team added the iShares TIPS Bond ETF TIP to Investing Ideas list on June 6th. It has outpaced the S&P 500 by over 100 basis points since then.

Macro analyst Darius Dale penned a particularly powerful institutional research note on the economy and Fed (see below) earlier this week which has obvious ramifications for our bullish TIP thesis.

* * * * * * *

Click on each title below to unlock the content.

Hedgeye macro analyst Darius Dale channels iconic rock superstar Prince and observes that while our GDP estimates are coming down, consensus macro remains out to lunch with theirs. In other words, stick with our year-to-date game plan.

ICI Fund Flow Survey: Significant U.S. Equity Outflows

The combined equity mutual fund complex shed almost $1 billion in outflows with significant domestic equity outflows offset by a slight international equity fund inflow. The broad take away is that the U.S. retail investor has been retrenching for most of the first half of the year.

What's Happening In Macau (and What It Means for Five Gaming Stocks)

In this video, Todd Jordan, Managing Director of Hedgeye's Gaming, Lodging and Leisure team, talks with fellow analyst David Benz about business conditions in Macau and the impact on these five stocks.