"For as this appalling ocean surrounds the verdant land, so in the soul of man there lies one insular Tahiti, full of peace and joy, but encompassed by all the horrors of the half-known life. God keep thee! Push not off from that isle, thou canst never return!" - Herman Melville, Moby Dick

The labor market appears to be the "insular Tahiti" Melville speaks of, surrounded by an appalling ocean of miserable data. Evidence continues to mount that the consumer is getting increasingly squeezed on the back of rising costs (commodities +11.6% YTD) and stagnant wages (personal income is +1.9% YTD). What's an investor to do?

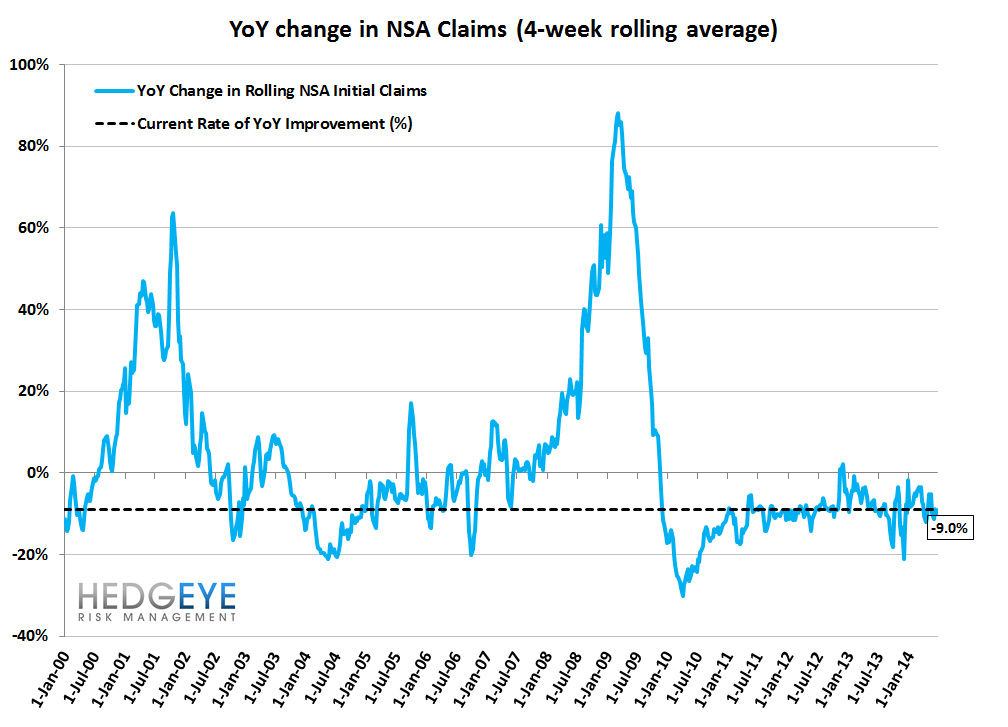

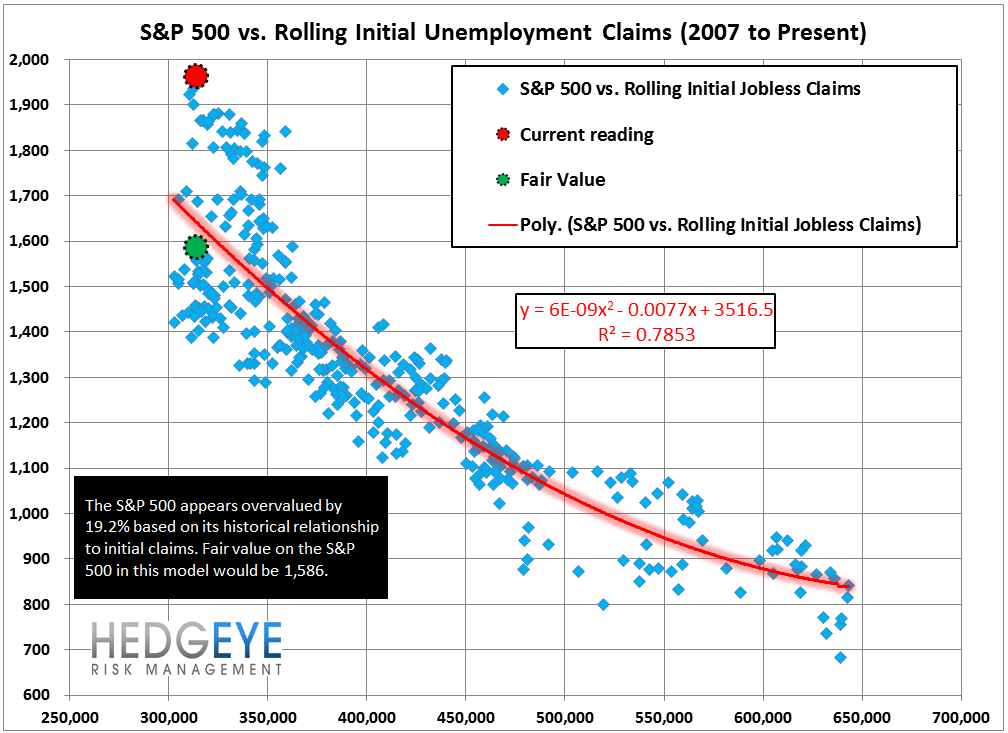

Our take is that investors should stick with claims as their weathervane. It's been a prescient indicator of turning points, marking both the top and bottom of the last cycle clearly and in a timely manner.

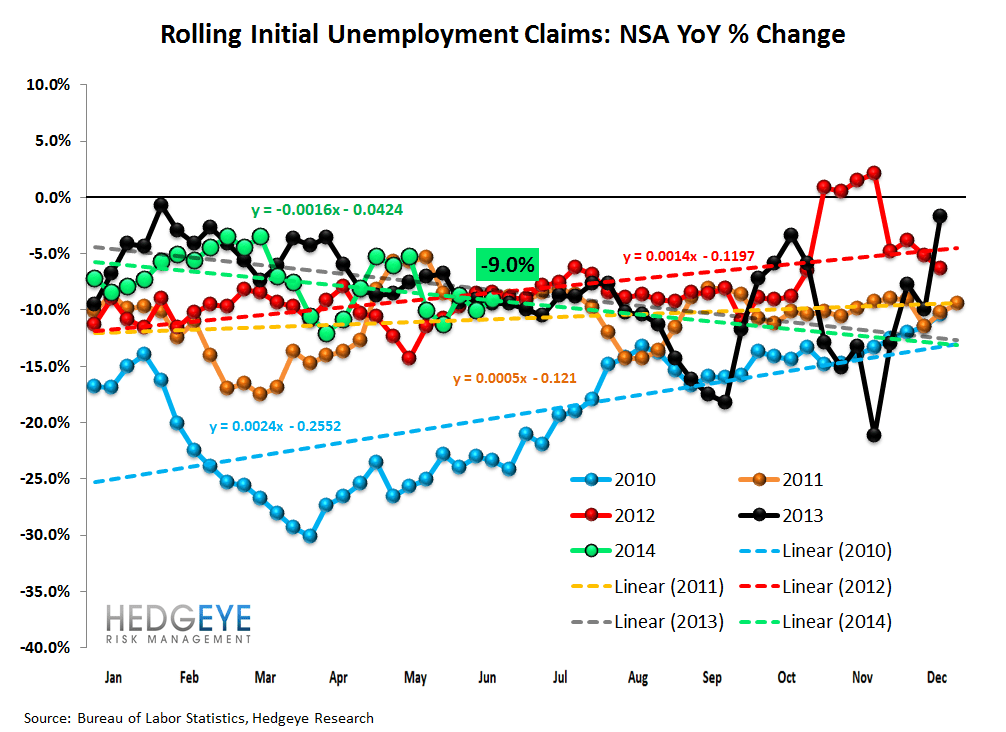

Along those lines, rolling initial jobless claims (NSA) were 9.0% lower than at the same point last year, which was in-line with the trend over the past 5 weeks (-9.8%, on average). The 9.0% improvement marks a slight deterioration vs the prior week's 10.1% improvement but isn't anything we'd get overly excited about.

One of our best long ideas remains Capital One (COF). The new new on Capital One is that credit card industry loan growth is showing early signs of accelerating (April and May data were much stronger than expectations). So long as credit quality is not degrading investors should increase the multiple they'll pay for Capital One's earnings in recognition of the accelerating loan growth. This morning's initial claims data shows there is no reason to worry about credit data for now so we're sticking with the idea.

The Data

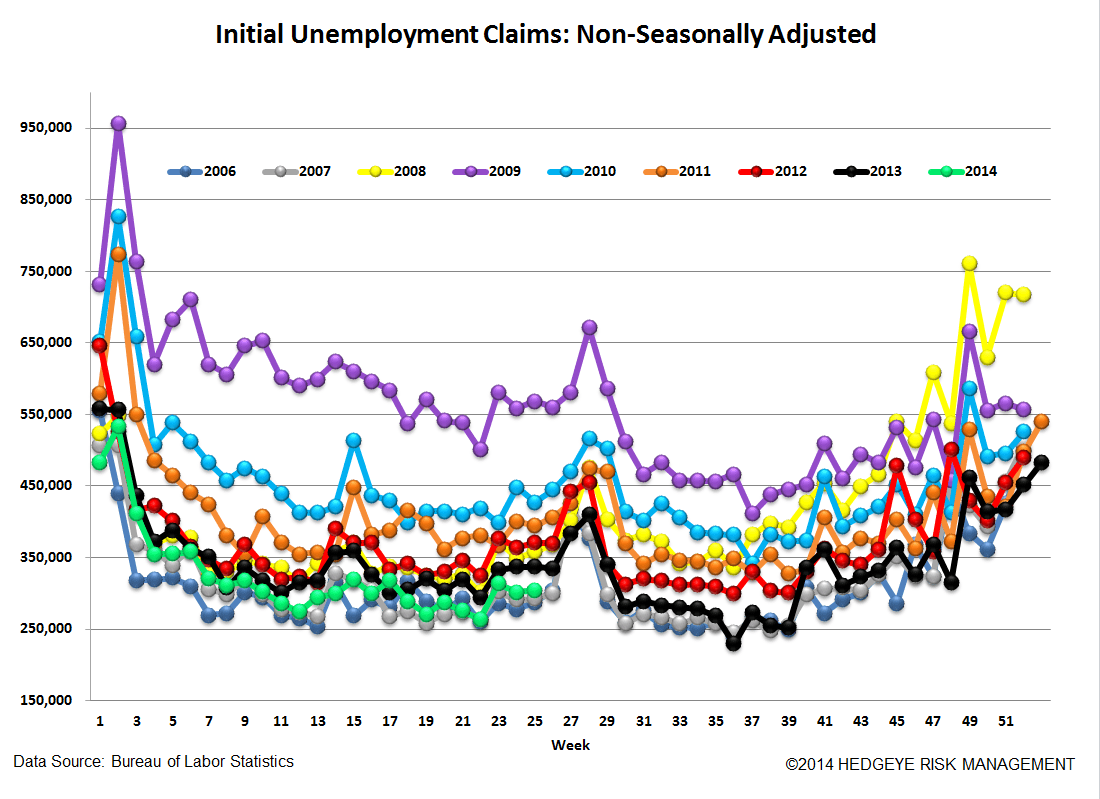

Prior to revision, initial jobless claims fell 0k to 312k from 312k WoW, as the prior week's number was revised up by 2k to 314k.

The headline (unrevised) number shows claims were lower by 2k WoW. Meanwhile, the 4-week rolling average of seasonally-adjusted claims rose 2k WoW to 314.25k.

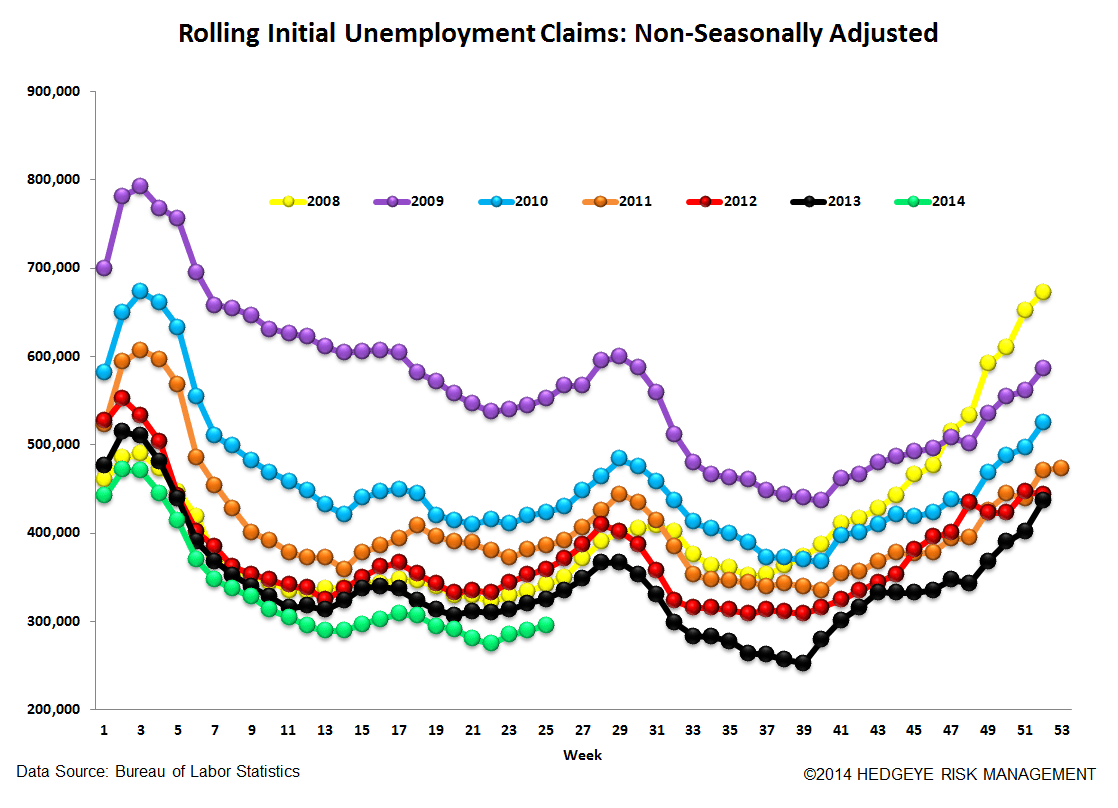

The 4-week rolling average of NSA claims, which we consider a more accurate representation of the underlying labor market trend, was -9.0% lower YoY, which is a sequential deterioration versus the previous week's YoY change of -10.1%

Yield Spreads

The 2-10 spread fell -6 basis points WoW to 208 bps. 2Q14TD, the 2-10 spread is averaging 221 bps, which is lower by -18 bps relative to 1Q14.

Joshua Steiner, CFA

Jonathan Casteleyn, CFA, CMT