“The very substance of the ambitious is merely the shadow of a dream.”

-Shakespeare

I’m in the throes of the Nevada desert with some colleagues and friends of Hedgeye. Later today, we will be attending the 2014 NHL Awards at the Wynn Casino. For the hockey players receiving awards, this is the epitome of their success and acknowledgment of their ability to fulfill their lifelong dreams. They have reached the pinnacle of their chosen profession. In hockey speak, they are #LivingTheDream.

Incidentally, Las Vegas, as much as any city in America, also epitomizes a dream - the American dream. From 1940 to the last census in 2012, the self-proclaimed “entertainment capital of the world” grew its population from some 8,000 inhabitants to almost 2 million, for a CAGR of north of 8%. This growth rate well outpaced the overall population growth rate in the United States, which increased by only about 1.5x during the same period.

As a function of this massive growth, 18 of the world’s largest 25 hotels are now in Las Vegas, the strip is the brightest place on earth that can be seen from space, and almost 40 million people annually visit Clark County (the home of Las Vegas). Despite these staggering statistics, on many metrics Vegas actually peaked in 2007. In that year, according to the Las Vegas Visitors and Convention Bureau, total gaming revenue in Clark County was $10.9 billion versus $9.7 billion in 2013.

Admittedly, gaming revenue in Clark County has recovered a fair bit off the recent bottom when it troughed at $8.8 million in 2009. Regardless, the fact remains that Las Vegas gaming revenue is still well off the peak and hasn’t grown since 2005. So, is this Las Vegas dream dead? Is the American dream dead?

On both questions, the answer is likely no. But whether we use the term the “new normal,” or some other cutesy name to describe the prospect for American domestic economic growth, the next five plus years will likely continue to be a normalizing of the excesses of the early 2000s. In many ways, Las Vegas remains the poster child for the boom and subsequent bust of that period.

Of course, as investors, we can always dream of a rampant reacceleration of economic growth, but as Shakespeare also wrote:

“And this weak and ideal theme, no more yielding than a dream.”

Indeed.

Back to the Global Macro Grind...

In the category of “more nightmare than dream” is the under-allocation of corporate pension funds and university endowments to the U.S. equity allocation rally that began in 2009. According a report out late yesterday, the average college endowment had a 16% allocation to equities in June 2013, versus 23% in 2008 and 32% a decade ago. Meanwhile, corporate pension funds on average had 43% of their portfolios allocated to equities versus 61% in 2003. Given the outperformance of U.S. equities over that time, it is likely that many of these institutions have been notable laggards in performance.

One clear threat to the equity bears is the potential that these large institutions begin to chase performance in unison. For a broad based allocation to equities to occur, these institutions would generally have to be of the view that GDP growth is set to accelerate and likely meaningfully so. If history is any indication, this is unlikely to occur.

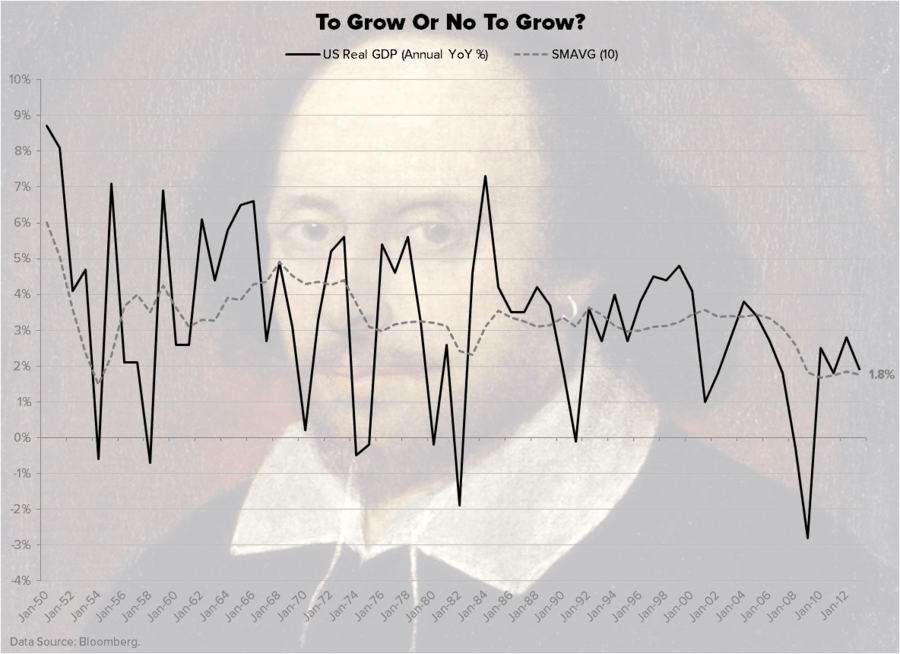

In the Chart of the Day below, we’ve looked at annual GDP growth in the United States going back to 1950 charted against the 10 year rolling average of growth. The takeaway from the chart is simply that U.S. GDP growth has been steadily coming down over time, and has had a sharp step down following the last recession. The U.S. economy seems to have now entered a phase of lower growth. Absent any evidence of acceleration of this trend, it will be difficult to compel large asset allocators to over allocate to the growth asset class of equities.

Speaking of not normal, according to Xinhua yesterday, noted Chinese economist Li Yining, “refuted the notion the Chinese economy is in decline saying that the previous high growth rates were not normal”. According to Yining’s analysis, China’s GDP should be higher than the released figure based on the fact that housing construction in rural areas is not included in the Chinese GDP calculation while it usually is in other regions.

Perhaps the Chinese government will take a page out of the U.S. government’s playbook and change the calculation as the economic statistics becomes less suitable to its needs. This is, of course, a page right out of the U.S. government’s playbook as the U.S. government has changed how the Consumer Price Index is calculated several times over the last few decades. (Ironically, this was also a period when the U.S. government had increasing obligations that were tied to inflation / CPI.)

To her credit, this ever changing methodology of changing inflation may in fact be the reason that Federal Reserve Chair Janet Yellen said last week, “recent readings on, for example, the CPI index have been a bit on the high side but the data are noisy.”

“Noisy” is an interesting characterization as the government’s own measure, CPI, actually jumped above 2.0% last month. Meanwhile, what is not noisy to those of us who eat, fuel our vehicles, or consume goods that have commodity inputs (read: most goods) is that the CRB Index is now up almost 12% year-to-date. We tend to agree with Yellein, that is noisy!

Our immediate-term Global Macro Risk Ranges are now:

UST 10yr Yield 2.47-2.64%

SPX 1

VIX 10.11-13.12

USD 80.16-80.43

Brent 113.11-116.67

Gold 1

Keep your head up and stick on the ice,

Daryl G. Jones

Director of Research