With the interest in protein in the food space (TSN-HSH) heating up, we thought a recent note from the Hedgeye Macro team on livestock and poultry prices is particularly applicable to the Consumer Staples sector. A copy of the work is included directly below.

---

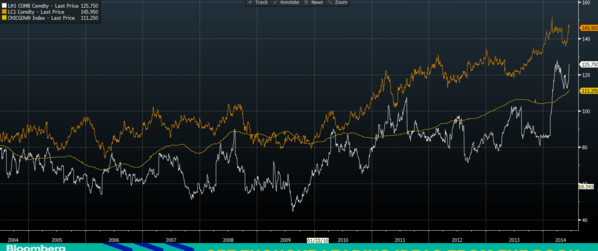

We continue to field arguments against the inflationary read-through on the commodity squeeze. Sharp increases in livestock and poultry prices over the last ten years in the face of stagnant wage growth, a decline in savings rates, and a declining U.S. dollar illustrate this reality in staggering fashion.

If Janet Yellen’s commentary yesterday is any indication, the fed will continue to promote yield-chasing from financial intermediaries and those lucky enough to hold equities and fixed assets. The PCE survey from the BLS reports the top quintile of income earners takes 66% of the aggregate income in the basket from interest, dividends, and investment related income. Needless to say, a majority of Americans consume meat.

2013 Meat Consumption Per Capita (KG/Person):

- United States: 106.9

- China: 53.5

- World Average: 34.9

The average consumer we have continuously highlighted is reaching insolvency. Median net income margins have consistently compressed over the last five years to about 1.38% with savings rates decreasing over the same period.

Last Ten Years:

- USD Index: -9.8%

- Trailing 1-year U.S. Personal Savings Rate: -9%

- S&P GSCI Livestock Index: +69%

- U.S. Private Sector Avg. Hourly Earnings (Real): -43%

survey from both the USDA and the University of Oklahoma’s Department of Agricultural Economics this week provide evidence that people are eating the higher price tags (adding to the pain, they drove to the store --> WTI and Brent hovering at 9-month highs).

- “This month’s survey shows consumers are willing to pay 11-35% more for steak, pork chops, and chicken wings"

- Food Demand Survey from the University of Oklahoma’s Department of Agricultural Economics

- The USDA’s Weekly Retail Beef Feature Activity Report highlighted a sharp decline in the number of food retail outlets featuring beef

Last Ten Years:

- Live Cattle: +71%

- Lean Hogs: +65%

- Chicken Breast: +40%

Disease or not contributing to the advances YTD, this kind of headline inflation is tangibly relevant on the wallet. Unfortunately most people were not granted the opportunity to add to their inflation hedges out of the FOMC statement yesterday where the Fed provided a downward revision to its 2014 GDP estimate for the SEVENTH year in a row:

- Headline CPI printed at +0.4% Tuesday vs. +0.2% expected (Inflation surprises)

- Full-year growth estimates cut to 2.1-2.3% from 3% at the Fed (coincident response as growth misses)

- 16 of 19 commodities in the CRB in positive territory on the year (prospect for future dollar devaluation increases; dollar down, cost of living up)

Ben Ryan

Analyst