Below are Hedgeye analysts' latest updates on our NINE current high-conviction investing ideas and CEO Keith McCullough's updated levels for each.

*Please note that we added OZM to Investing Ideas earlier this week. We will send out a full report next week.

We also feature two institutional research notes from earlier this week, as well as Keith McCullough's Friday morning macro call, all of which offer valuable insight into the markets and economy.

Trade :: Trend :: Tail Process - These are three durations over which we analyze investment ideas and themes. Hedgeye has created a process as a way of characterizing our investment ideas and their risk profiles, to fit the investing strategies and preferences of our subscribers.

- "Trade" is a duration of 3 weeks or less

- "Trend" is a duration of 3 months or more

- "Tail" is a duration of 3 years or less

HEDGEYE CARTOON OF THE WEEK

IDEAS UPDATES

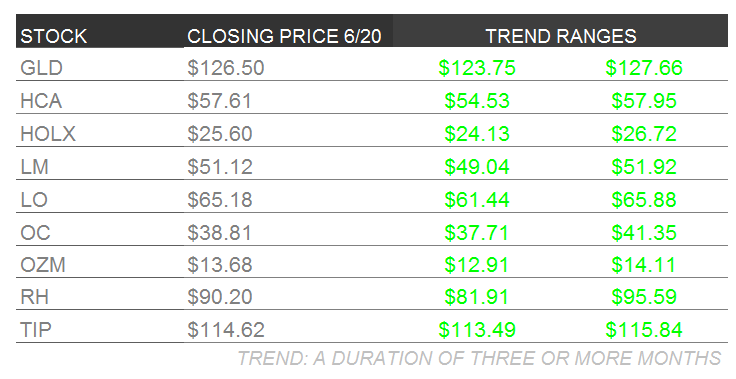

GLD – This past Thursday Gold broke out of Hedgeye's immediate-term TRADE resistance of $1285 with the new risk range at $1285-$1336/oz. and intermediate-term upside from to TREND resistance of $1381.

The repetitive call to front-run the Fed’s response to worse-than expected economic data finally manifest this week:

- Headline CPI prints +0.4% vs +0.2% expected (inflation accelerates)

- Full-year GDP forecast from the Fed lowered to 2.1-2.3% from 3% (growth misses and warrants a response)

As inflation accelerates, and growth expectations decrease, the likelihood of an easier Fed increases:

- GLD Surges 3.5% on Thursday

- Spot Volumes: 62%, 52%, and 49% above 1, 3, and 6-Month averages respectively

- The 1-Week negative correlation tightens significantly to -0.91

Meanwhile, divergence in the equity markets between consumer-based growth and inflationary sectors continues to take hold:

- Energy (XLE) (+13.5% YTD); Utilities (XLU) (+14.9%)

- Consumer Discretionary (XLY) (-1.00%)

HCA – Healthcare sector head Tom Tobin has no update on HCA whose shares were up almost 5% this week. He reiterates his high-conviction call on the stock.

HOLX – (Editor's note: The following update was sent in from Healthcare sector head Tom Tobin earlier today.)

I was running around San Francisco yesterday meeting with clients and again got a fresh round of questions about the upcoming 3D reimbursement announcement from CMS. Apparently my questioners had seen a note from “my guy in DC” regarding Hologic. This DC consultant’s business is to know what is coming out of DC regulators before news is officially announced, which is dubious for obvious reasons, but it doesn’t mean it isn’t true.

The call is that when the reimbursement is announced at the beginning of July, 3D Tomography will not receive any additional dollar amount over 2D. This is a problem for how long it takes HOLX and GE to penetrate the market where even an extra $25 per scan across 4 scans per hour and 8 hours a day, tallies up to a big number which can easily offset equipment cost.

If “my-guy-in-DC” is right, and has the inside view of what CMS will say, there will be a few sequential outcomes.

- HOLX trades down to $21-$22, or returns to the multiple it was at before HOLX announced they were finally receiving a code this year.

- Sellside makes no change to their estimates, since numbers have only moved higher to incorporate the March quarter upside and company guidance

- Breast cancer advocacy groups, facilities, and GE/HOLX pressure politicians and ultimately CMS to increase 3D reimbursement by the time the final rule is announced in November, or GE/HOLX launch a legislative initiative as they did to gain incremental reimbursement for 2D. Either way, 3D will ultimately get a reimbursement increase over 2D

Even if I adjust my 3D facility adoption curve to a slower penetration pace to reflect $0 incremental reimbursement increase, HOLX should trade in the $30-$38 range over the coming 12-18 months. Street estimates for the June quarter are too low regardless. Regardless of the reimbursement outcome, I’ll be able to see how many facilities are buying a 3D system, so if there is an impact, I’ll see it.

If we’re wrong on reimbursement, we still see several tailwinds for 3D

- Mammography is competitive and facilities need to upgrade to maintain market share

- A replacement cycle will accelerate as 2D systems from the last replacement cycle reach the end of their useful lives of 7-10 years

- Mammography capital market is expanding

- ACA is accretive to mammography demand

- Dense Breast legislation drives conversion

- A lower callback rate for 3D is accretive to the practice profits

LM – Deal activity in the asset management sector has taken a noticeable leg up during the course of the second quarter with several recognizable AUM transactions occurring in this week alone. Second quarter 2014 deal tallies have aggregated to $44 billion globally on 282 transactions amongst global asset management firms, the highest level since the $45 billion that transacted in the 4th quarter of 2007.

Generally, we estimate that nascent deal flow facilitates incremental transactions as empirical comps are created which can accelerate the deal process of pending negotiations in the pipeline.

We remind investors that part of our rationale for recommending Legg Mason as a long on our Best Ideas list is the company has been a successful roll up of various asset management properties over the past 20 years with the accretive integration of investment managers employing everything from quantitative strategies to domestic small cap equities to European hedge funds.

Historically, LM stock has reacted quite favorably to its roll-up strategy with substantial outperformance against the market after employing M&A. In analyzing the acquisitions of the main affiliates that still surivive under the LM umbrella (Batterymarch, Brandywine, Royce, etc), Legg stock has outperformed the S&P 500 by 900 basis points on average in the 6 and 12 month time periods after deal announcements. Thus if the recent amend and extend within Legg's long term capital structure does allow the company more financial flexibility coincides with what we believe is management's threshold to only do an immediately accretive deal, LM may soon finally pull a new affiliate under its umbrella which has been historically positive.

LO – Lorillard enjoyed a nice 6.5% pop this week, finishing Friday up 1.5%. There was little news on the week concerning the stock, yet the "animal spirits" surrounding a potential take-out from Reynolds American (RAI) continue to boost shares. We suggest staying on for the ride higher.

In related news, there was a Senate hearing on e-cigarettes earlier in the week. One key takeaway from it is that should the FDA finalize its proposed regulations for e-cigs – which did not ban the marketing of e-cigs – big Tobacco companies like LO stand to benefit over smaller independents given their deep pockets.

We continue to outline the long-term fair value price of the stock at $80/share. We do not think LO will be imminently purchased and are staying long the stock that we added to Investing Ideas on 3/7/14. It is up over 24% since then.

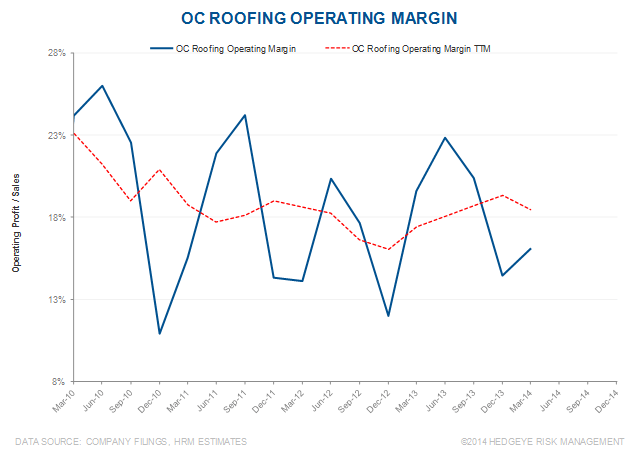

OC – Owens Corning lowered its operating profit outlook Friday morning from $500 million to above $416 million, a move it hinted to in first quarter results. The roofing market is facing excess production, depressed demand from this past winter and a large competitor behaving aggressively in the market. Even in this environment OC’s roofing segment is still earning a respectable 18.4% TTM operating margin. OC’s roofing segment makes up ~30% of sales. OC’s other segments insulation and composites are still showing strong signs, which management noted in the same press release.

As of right now we reaffirm our long term outlook. We will want to get a better sense of the roofing market dynamics if we need to adjust our view. We continue to expect the shares to perform well longer-term if the company can come anywhere near consensus expectations.

RH – (Editor's note: Shares of Restoration Hardware were up over 18% last week, followed by an 11% gain this week, bringing its total gain to 32% over the last two weeks. Hedgeye retail sector head Brian McGough still thinks RH is the best idea in retail and has major upside potential from here.)

We were initially caught off guard in seeing the announcement from Restoration Hardware that it would sell up to $350mm in convertible notes. But after going through the numbers and the logic, we think it makes all the sense in the world. Here’s what we’re thinking…

- The company is, in effect, creating $350mm of low-cost liquidity through a convertible note offering. It currently has only $149mm outstanding on a $417.5mm credit facility. So why would it need to do this deal?

- First off, because it can. We’d like to see the company tap the capital markets for lower cost financing from a position of strength rather than from a defensive position if the long-term growth plan is thrown a curve ball.

- The cost of the debt is not the issue at hand. Yes, it’s nice that the structure of this deal suggests that there is no dilution until the stock is $172 – about 95% above Thursday's closing price. And even then, we’re only talking about 1-2% dilution.

- No, the KEY ISSUE here is duration matching. The company just started what will be a 5+ year store growth plan where it will take square footage from 825k to about 2.3mm. It is signing leases today for 2H16. Its current credit facility expires in August 2016. One of the bear cases we hear is that the company would be locked into expensive leases in 2017/18 without having liquidity protection. Then we go into a recession, which would hurt cash flow and close the window for the company to find liquidity to finance its growth. That argument is officially shot in the foot.

The punch line on this financing deal is that it de-risked the growth strategy, and took out one of the key bear arguments on this stock. If there’s any bad news, it’s that that there will be dilution at some point over the next few years – because we think that RH trades through $172.

TIP – The Federal Reserve targeted rates lower again this week, adding to our #InflationAccelerating theme and burnishing our high-conviction, inflation-protection TIP idea. We see cyclical and structural inflationary pressures, with commodity inflation accelerating to fresh YTD highs.

- CRB (19 component) Commodities Index = +11.4% YTD

- CRB Food Index up another +2.1% this week = +22.8% YTD

- Nickel +2.9% this week = +33.1 % YTD, and

- Gold +3.5% this week = +9.5% YTD

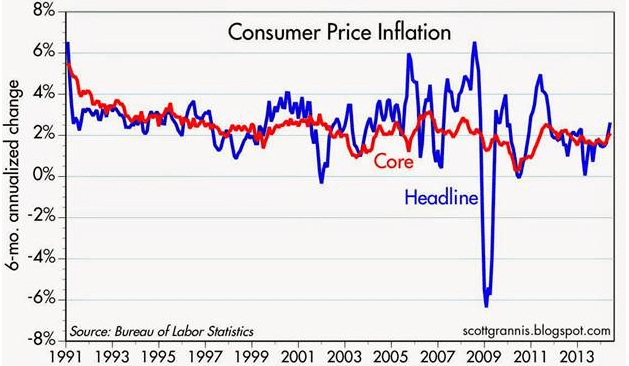

If we’re right and the inflation-accelerating-slows US growth setup is similar to 2011, Gold can go a lot higher, and yesterday it broke out above Hedgeye’s immediate-term TRADE resistance of $1285/oz. Tuesday’s data reported CPI MoM up to 0.1% to 0.4%, CPI YoY up 0.1% to 2.1%, and CPI Core Index up 0.2% to 2.0%, all of which were higher than estimates.

The chart above (courtesy of Scott Grannis) shows inflation accelerating from 1.5% in February to 2.6% in May and core inflation accelerating from 1.6% to 2.1% in the same time frame. Additionally, with the dollar quite weak, and gold and commodity prices elevated, the economy is symptomatic of rising inflation. All of the aforementioned data points confirm our stance on iShares TIPS Bond ETF TIP being a high-conviction investment idea.

* * * * * * *

Click on each title below to unlock the content.

All-Time Highs: Can Livestock and Poultry Prices Go Higher?

We continue to field arguments against the inflationary read-through on the commodity squeeze. Sharp increases in livestock and poultry prices over the last ten years in the face of stagnant wage growth, a decline in savings rates, and a declining U.S. dollar illustrate this reality in staggering fashion.

ICI Fund Flow Survey: Bonds Are Running, Stocks Are Choppy

Taxable bonds just put up their 18th consecutive week of inflow assisted by tax-free inflows at 22 consecutive weeks. Conversely, equity funds had another choppy week with domestic stock fund outflows, the 7th consecutive week, offset by international stock fund inflows.

Keith McCullough's Morning Macro Call 7.20.14

Hedgeye CEO Keith McCullough takes a deep dive into what's going on in the markets and economy with a close look at commodities, gold and utilities.