TODAY’S S&P 500 SET-UP – June 20, 2014

As we look at today's setup for the S&P 500, the range is 37 points or 1.66% downside to 1927 and 0.23% upside to 1964.

SECTOR PERFORMANCE

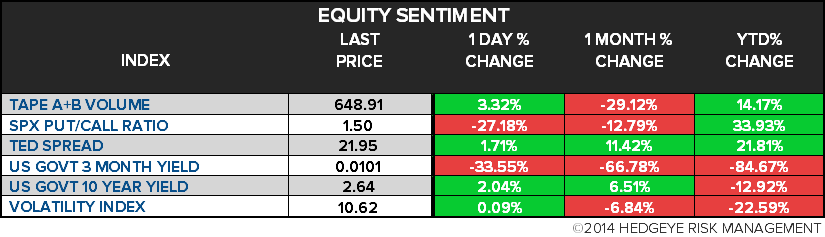

EQUITY SENTIMENT:

CREDIT/ECONOMIC MARKET LOOK:

- YIELD CURVE: 2.19 from 2.17

- VIX closed at 10.62 1 day percent change of 0.09%

MACRO DATA POINTS (Bloomberg Estimates):

• No major economic reports scheduled

• 1pm: Baker Hughes rig count

GOVERNMENT:

- House in session; Senate schedule TBA

- President Obama meets with New Zealand PM John Key

- SEC Chairman Mary Jo White speaks at Economic Club of N.Y.

- 9am: House Judiciary hearing on net neutrality/antitrust law, w/FTC Commissioner Joshua Wright

- 9am: House Ways/Means Cmte hearing on IRS treatment of tax-exempt orgs.

- 9am: House Maj. Whip Kevin McCarthy, Rep. Paul Ryan, N.J. Gov. Chris Christie speak at Faith and Freedom Coalition

- 9:30am: House Nat. Resources panel Nat. Gas Gathering Enhancement Act (H.R. 4293), Energy Infra. Improvement Act (H.R. 1587)

- 9:30am: House Veterans’ Affairs Cmte hearing on Sr. Exec. Service performance subpoena

WHAT TO WATCH:

- Shire rejects AbbVie’s $46.5b takeover bid as too low

- Siemens lifts Alstom Energy bid to $19.9b, defying GE

- Obama sending advisers to give Iraq time to form govt.

- Energy Transfer “high level” talks to acquire Targa terminated

- BofA must face U.S. suit claiming mortgage-securities fraud

- Oracle sales, profit miss estimates amid transition to cloud

- Icahn urges Family Dollar CEO to seek sale “immediately"

- Revel casino files for bankruptcy, seeking savior at auction

- U.K. May budget deficit little changed after 1-time 2013 boost

- NYC Fifth Avenue tower sells to Thor-led group for $595m

- Verizon said meeting with Dish on possible spectrum sale: NYPost

- U.S. GDP, Housing Data, Nike, Wimbledon: Week Ahead June 21-28

EARNINGS:

- CarMax (KMX) 7am, $0.67

- Darden Restaurants (DRI) 7am, $0.94

COMMODITY/GROWTH EXPECTATION (HEADLINES FROM BLOOMBERG)

- Gold Options Signal Sustained Rally as Yellen Shakes Out Boredom

- Brent Heads for Second Weekly Gain on Iraq Violence; WTI Steady

- China Miners’ Loss Is BHP Gain as Iron Slumps 44%: Commodities

- LNG Rally Fading on New Supply as Nukes Set to Restart: Energy

- Copper Gains Most in Three Weeks as Zinc Trades at 16-Month High

- Gold Falls With Rally Seen Overdone as Investors Close Positions

- Soybeans Slide on Expectation U.S. Farmers Expanded Planting

- Asia’s WAF Purchases for July Stable; Nigerian Imports to Rise

- Digital Shipping Platforms Cutting $684 Million Errors: Freight

- Rising German Coal Use Imperils Emissions Deal: Carbon & Climate

- Kansai Electric Said to Agree With Cheniere to Purchase U.S. LNG

- RBI, Finance Ministry Said to Work on Iran Oil Payment Process

- Energy Traders Pay More Than 100 Million Euros to Meet New Rules

- China Metal Probe to Push Copper to LME Depots: Chart of the Day

CURRENCIES

GLOBAL PERFORMANCE

EUROPEAN MARKETS

ASIAN MARKETS

MIDDLE EAST

The Hedgeye Macro Team