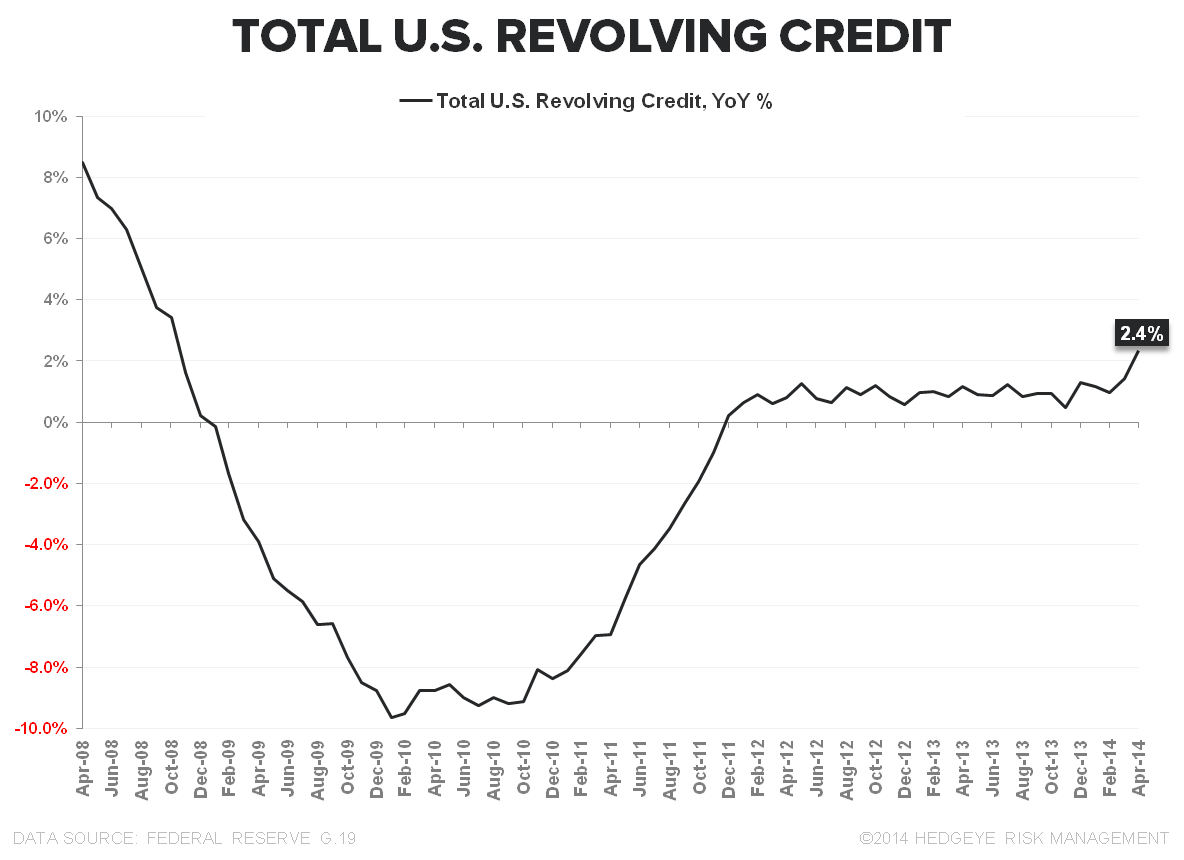

In Friday’s Early Look (Giddy Up) we highlighted the Fed G.19 Data from April which showed US revolving consumer credit balances rose at a month-over-month annualized rate of +12.3%, the fastest rate of growth since 2001.

While the (potential) inflection was certainly notable, historically, the series has been volatile and subject to significant revision, so the preliminary data is to be taken with some caution.

In short, it was interesting but, in isolation, hard to build any specific conviction around.

This morning, we received some confirmatory data from Capital One (COF) who reported domestic card loans grew 1.7% MoM in May – a continuation of the strength observed in April.

There are a few primary takeaways:

- For COF, the increase in May was well ahead of typical May changes observed over the last decade and a second consecutive month of strength.

- For consumer credit more broadly, the positive inflection in credit card loan growth is coming after more than 2.5 years of consistent, stagnant 0-1% growth.

- Consumption: Despite the acceleration in revolving credit, Household Spending in April was very soft and the collective Retail Sales data for April/May was very much middling

Whether or not rising auto and card balances is reflective of a confident, resurgent consumer or simply an attempt by households to maintain current levels of consumption in the face of rising food and commodity inflation remains open to debate.

At present, we continue to think the data sides more with the later than the former.

Christian B. Drake

@HedgeyeUSA