We added DFRG to our Best Ideas list as a SHORT on 06/05/2014 at $27.27/share.

Last week, we released a 67 page Black Book detailing why we believe DFRG is a short. The following note is a very brief summary of our presentation. If you would like more information or a copy of the deck, please email us.

Our short thesis centers on three critical themes:

- Slowing Trends, Declining Margins – Company-owned two-year same-store sales and traffic have been decelerating steadily since 3Q11. Meanwhile, restaurant level margins (LTM) and operating margins (LTM) have been declining since 2Q12.

- A Portfolio In Flux – Del Frisco’s Double Eagle Steakhouse is a robust concept, but two-year same-store sales and traffic are decelerating. The Sullivan’s concept is broken. Grille is, at this point, nothing more than an unproven growth concept.

- Materially Mispriced – At 28.22x P/E (FY14) and 13.39x EV/EBITA (FY14), we believe DFRG is materially mispriced and fails to discount slowing trends, declining margins, rising commodity costs and other issues we’ve identified. Our SOTP analysis suggests significant downside.

As always, we like to put duration into context with all our longs and shorts.

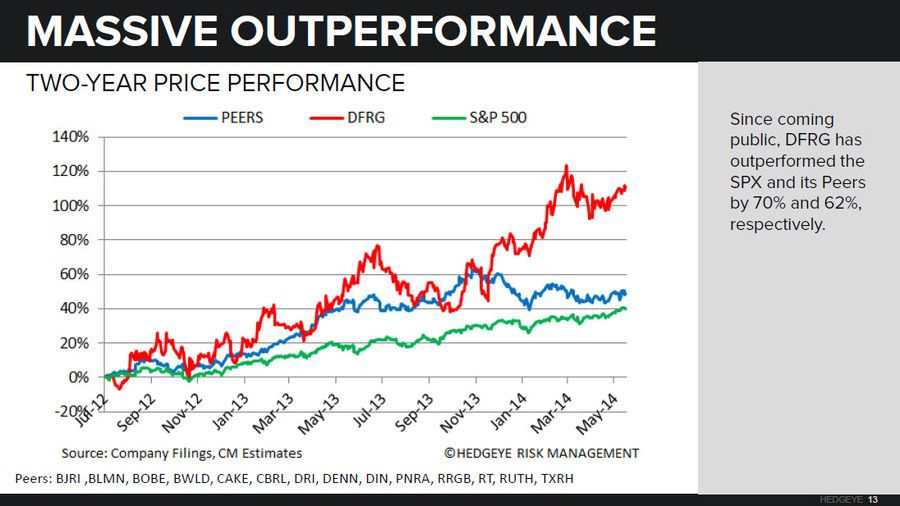

Over the past two years, DFRG has outperformed the SPX and its Peers by 70% and 62%, respectively.

The financial performance of DFRG revolves around the performance of Del Frisco’s concept, with the brand generating 48.9% and 62.3% of revenues and restaurant level EBITDA, respectively.

What are the bulls saying?

Same-store sales are decelerating and remodels are not the panacea for Sullivan’s.

DFRG’s premium valuation is driven by the potential growth of the Grille concept. With only 11 units, it is premature to call Grille a viable growth vehicle. In addition, sister concepts traditionally have a poor track record.

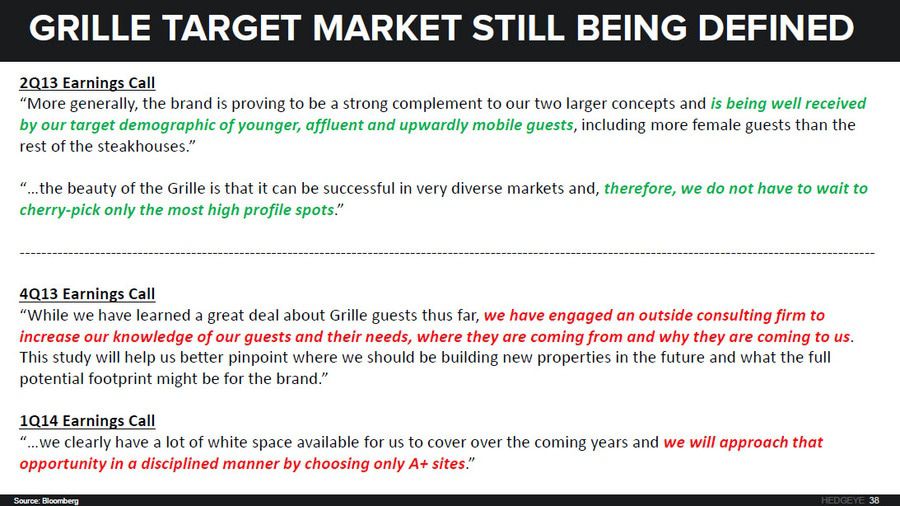

Management is still trying to understand its target market for the Grille and appears unsure of what locations to select.

At 17.6%, Grille’s restaurant level margins are 1100 bps below that of Del Frisco’s. This will continue to pressure the margin structure of the company, particularly with management’s current growth plans.

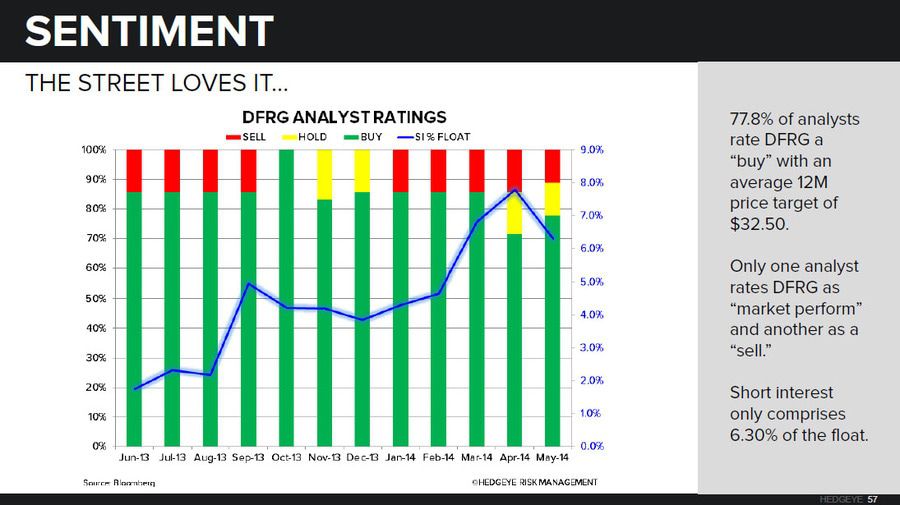

The Street loves the company.

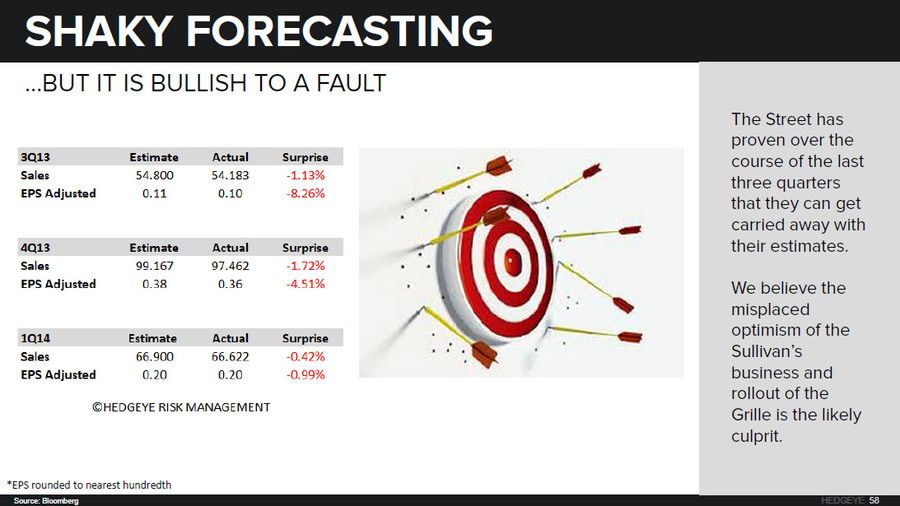

But management has struggled to deliver on sales and earnings expectations.

DFRG is trading near its all-time peak on several valuation fronts.

Using a generous sum-of-the-parts valuation analysis, we find that the stock is grossly overvalued.

Call with questions.

Howard Penney

Managing Director

Fred Masotta

Analyst