INVESTMENT IDEAS

The table below lists our current investment ideas as well as a list of potential ideas we are in the process of evaluating (watch list). We intend to update this table regularly and will provide detail on any material changes.

Consumer Staples fell -1.2% week-over-week versus the broader market (S&P500) down -0.7 %. XLP is up 4.0% year-to-date versus the SPX at 4.8%.

EVENTS THIS WEEK

6/17/14 Deutsche Bank Global Consumer Conference: CP; TUP; NWL; CLX

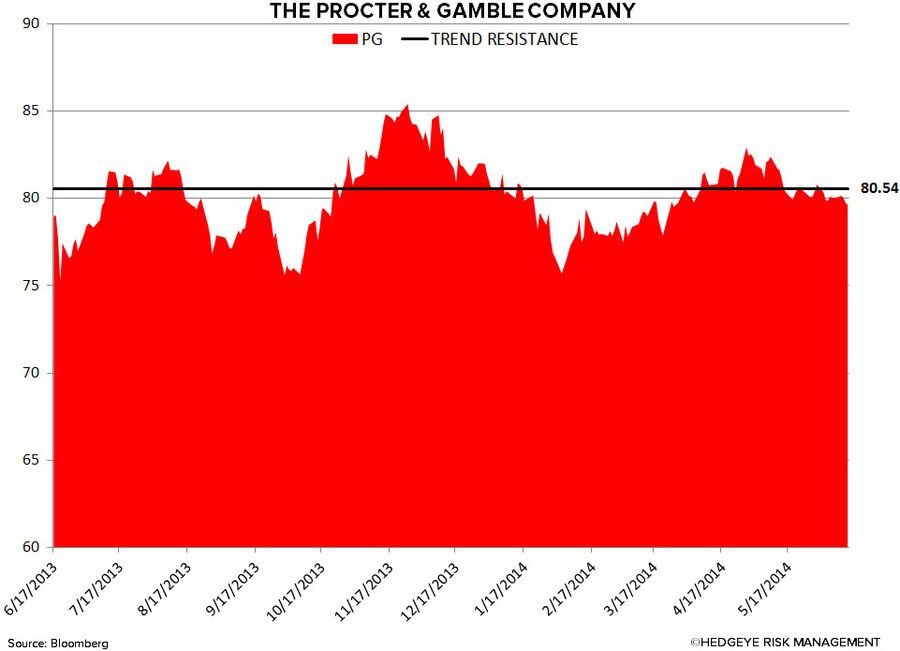

6/18/14 Deutsche Bank Global Consumer Conference: PG; CHD; IFF; CCE. Jefferies Global Consumer Conference: MJN

6/19/14 Jefferies Global Consumer Conference: JAH

XLP remains bullish on immediate term TRADE and intermediate term TREND durations from a quantitative set-up.

The Hedgeye U.S. Consumption Model has shown steady improvement over the past month, with 6 of the 12 U.S. Economic Indicators flashing green.

Despite the bullish quantitative set-up for the sector, we continue to believe that the group is facing numerous headwinds, including:

- U.S. consumption growth is slowing as inflation rises, in-line with the Macro team’s 1Q14 theme of #InflationAccelerating, and Q2 2014 theme of #ConsumerSlowing

- The economies and currencies of the emerging market – once the sector’s greatest growth engine – remain weak with the prospect of higher inflation in 2014 eroding real growth

- The sector is loaded with a premium valuation (P/E of 19.8x)

- Less sector Yield Chasing as Fed continues its tapering program

- The high frequency Bloomberg weekly U.S. Consumer Comfort Index (recently rescaled for cosmetic and not component reasons) has not seen any real improvement over the past 6 months, but rose to 35.5 versus 35.1 in the prior week

NEWS

HSH – the company confirmed this morning that its board of directors has unanimously decided to withdraw its recommendation of the pending acquisition of Pinnacle Foods (PF) in light of the $63/share proposal from TSN. Tyson expects to realize annual synergies in excess of $300M and PF would stand to receive a $163M termination fee if the deal with TSN is finalized. The deal reflects consumers’ growth in demand for high protein foods. HSH is up a monster +85% ytd.

LO – LO was up just slightly on the week. The investment community still wonders if LO will be taken out, likely by Reynolds American (RAI). We continue to suggest that investors hold this stock into potential news of the buyout or until our long-term fair value price of the stock at $80/share is realized. We continue to assert that the company’s powerful earnings generation is anchored on its advantaged tobacco and e-cigarette portfolio. Bottom line: we do not think LO will be imminently purchased and are staying long the stock that we added as a Best Idea on 2/26/14.

TOP 5 WEEK-OVER-WEEK DIVERGENT PERFORMANCES

Positive Divergence: RDEN 18.6%; BNNY 14.3%; TAP 6.8%; HSH 4.9%; LO 2.3%

Negative Divergence: TSN -11.7%; HAIN -6.2%; SMG -4.4%; NUS -3.8%; ADM -3.0%

RECENT NOTES

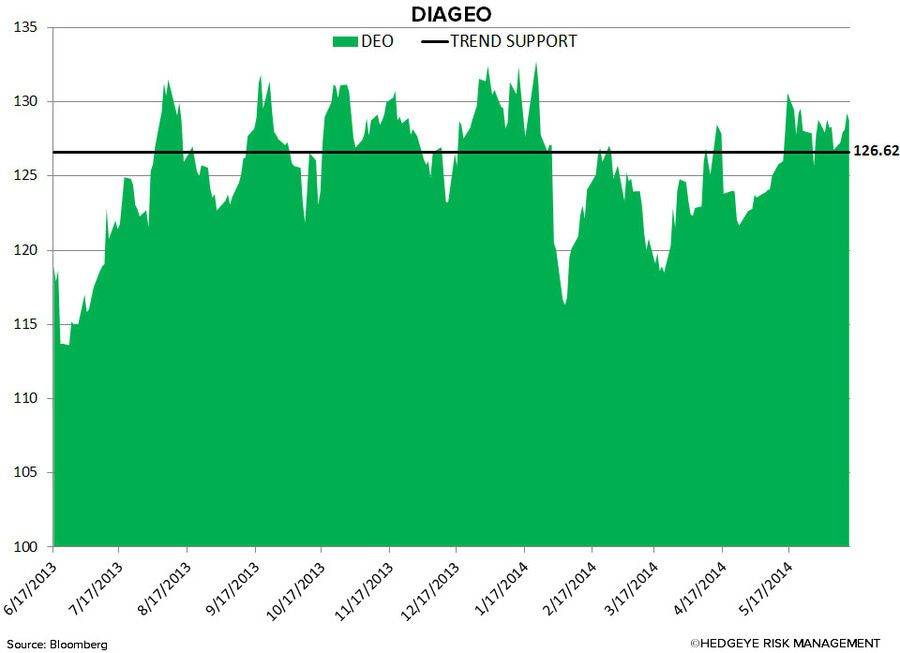

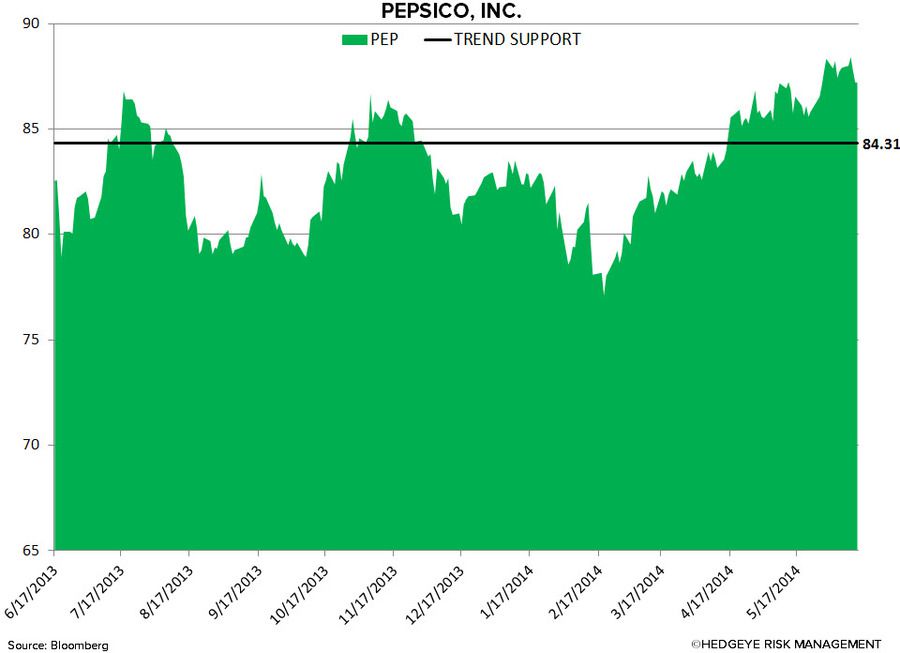

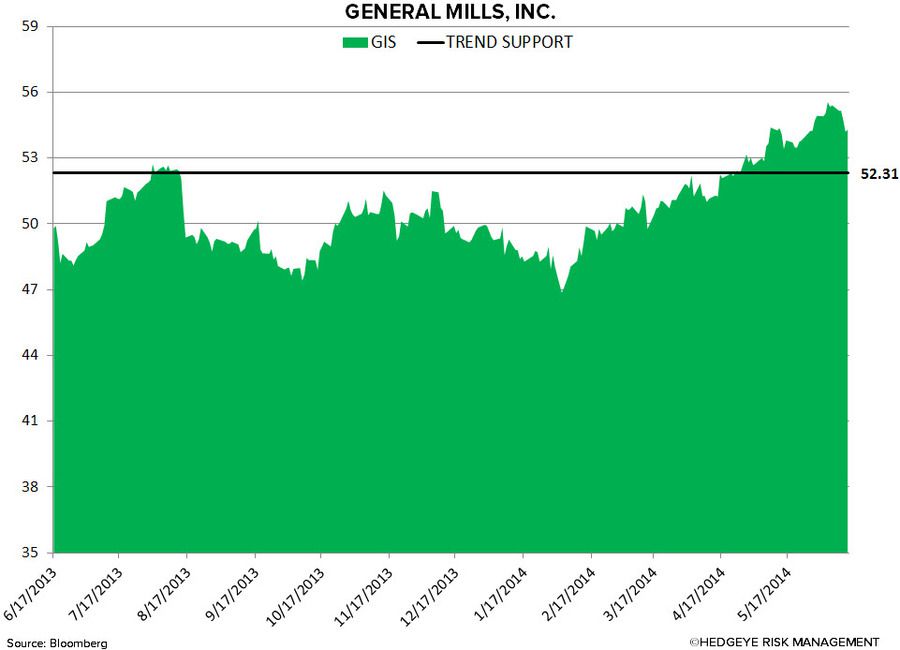

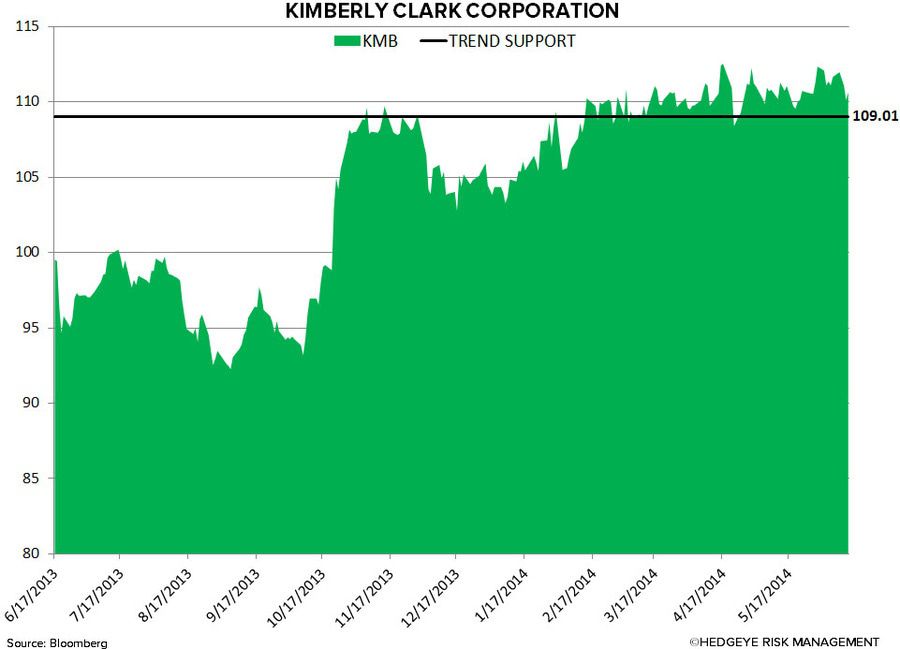

QUANTITATIVE SETUP

Howard Penney

Managing Director

Matt Hedrick

Associate

Fred Masotta

Analyst